|

市場調查報告書

商品編碼

1998656

工業燃燒器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Industrial Burner on Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

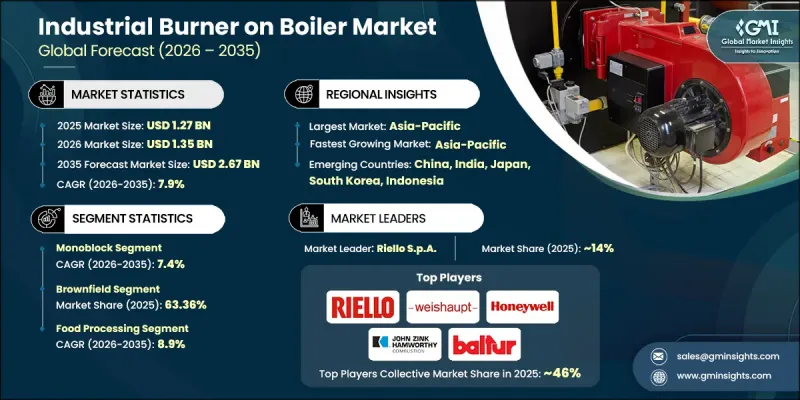

預計到 2025 年,全球鍋爐工業燃燒器市場價值將達到 12.7 億美元,到 2035 年將以 7.9% 的複合年成長率成長至 26.7 億美元。

工業生產的成長和製造設施的持續擴張推動了對可靠鍋爐燃燒系統的需求。工業燃燒器在確保穩定且有效率的供熱方面發揮著至關重要的作用,從而保證了大規模生產環境中鍋爐性能的穩定性。可靠的燃燒技術有助於工廠最佳化能源消耗,同時最大限度地減少中斷,維持製程的連續運作。提高能源效率和降低營運成本的壓力日益增大,推動了工業領域採用能夠實現精確燃燒控制的先進燃燒器技術。此外,現有鍋爐基礎設施的現代化改造也持續催生了對燃燒器系統及相關設備升級的需求。工廠越來越傾向於尋求能夠支援精確溫度控制並符合不斷變化的環境法規的解決方案。燃燒器設計的持續技術進步也有助於提高燃料利用效率並降低維護需求。由於工業流程仍然高度依賴蒸氣和熱能,因此對鍋爐系統中先進工業燃燒器的需求將繼續成為推動全球鍋爐工業燃燒器市場長期成長的主要動力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 12.7億美元 |

| 預計金額 | 26.7億美元 |

| 複合年成長率 | 7.9% |

預計到2025年,整體式燃燒器市場規模將達到7.235億美元,並在2026年至2035年間以7.4%的複合年成長率成長。這種設計因其將燃燒器、風機和控制單元等關鍵燃燒部件整合到一個緊湊的系統中而廣受業界認可。這種整合式配置可實現穩定的空燃比,從而帶來穩定的燃燒性能和更高的熱效率。此外,其緊湊的結構簡化了安裝流程,降低了維護的複雜性,使其成為各種工業加熱環境的理想選擇。隨著市場對兼具可靠性能和高能源效率的節省空間燃燒技術的需求不斷成長,整體式燃燒器的應用正在加速發展。其易於操作、可靠性高以及維護簡單等優勢,使整體式燃燒器成為全球鍋爐工業燃燒器產業的領先設計類別。

預計到2025年,棕地市場將佔據63.36%的市場佔有率,並在2026年至2035年間以7.1%的複合年成長率成長。棕地改造引領市場的主要驅動力在於,人們日益成長的需求是在不更換整個系統的情況下,對現有鍋爐基礎設施進行升級和現代化改造。透過將先進的燃燒器技術整合到現有設施中,工業領域可以提高燃燒效率並減少排放。這種方法使企業能夠在避免長時間生產中斷和過度資本投資的同時,提高營運績效。對能源最佳化、法規遵循以及延長現有工業設備使用壽命的日益關注,持續推動棕地改造計劃的發展。這種安裝模式的經濟可行性和營運優勢使其成為工業鍋爐燃燒器市場的主導模式。

預計到2025年,中國鍋爐工業燃燒器市場規模將達到1.79億美元,並在2026年至2035年間以8.1%的複合年成長率成長。蓬勃發展的工業活動和能源密集產業的持續擴張是推動中國市場領先地位的主要動力。隨著大規模工業活動能源需求的不斷成長,對能夠提供可靠熱輸出的高效燃燒技術的需求也日益增加。工業設施優先考慮火焰穩定、運作控制精確、熱性能高的燃燒器系統,以支援不間斷的生產週期。政府針對空氣品質和排放氣體的法規也推動了先進燃燒器技術的應用,這些技術旨在減少排放排放並提高燃料效率。此外,對工業基礎設施的持續投資和鍋爐系統的現代化改造也持續刺激著國內產能的成長。自動化燃燒管理系統和靈活燃料運作等技術進步進一步鞏固了中國在亞太地區鍋爐工業燃燒器市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 流程工業對蒸氣和熱能的需求不斷成長

- 擴建發電和熱電汽電共生設施

- 食品加工、化工以及紙漿和造紙業的成長

- 陷阱與挑戰

- 先進低氮氧化物燃燒器系統的高初始投資成本

- 與現有鍋爐和控制系統的複雜整合

- 機會

- 擴大雙燃料和多燃料燃燒器技術的應用。

- 將數位控制和自動化整合到燃燒器管理系統中

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依燃燒器設計分類,2022-2035年

- 單體塊

- 雙區塊

第6章 市場估算與預測:依部署類型分類,2022-2035年

- 棕地

- 待開發區

第7章 市場估計與預測:依輸出範圍,2022-2035年

- 小於300千瓦

- 300 kW~1 MW

- 1~5 MW

- 5~20MW

- 20~50 MW

- 超過50兆瓦

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 發電

- 化工/石油化工

- 金屬加工

- 食品加工

- 纖維

- 紙漿和造紙

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Alzeta Corporation

- Andritz AG

- Baltur

- Bentone

- Ebico

- Fives Group

- Honeywell International

- John Zink Hamworthy Combustion

- NIBE Group

- Oilon Group Oy

- Oxilon Pvt. Ltd.

- Riello SpA

- Selas Heat Technology Company

- Weishaupt GmbH

- Zeeco, Inc.

The Global Industrial Burner on Boiler Market was valued at USD 1.27 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 2.67 billion by 2035.

Rising industrial production and the ongoing expansion of manufacturing facilities are creating strong demand for dependable boiler combustion systems. Industrial burners play a critical role in ensuring stable and efficient heat generation, enabling consistent boiler performance across large-scale production environments. Reliable combustion technology helps facilities optimize energy consumption while maintaining continuous process operations with minimal disruptions. Growing pressure to improve energy efficiency and reduce operational costs is encouraging industries to adopt advanced burner technologies capable of delivering precise combustion control. In addition, the modernization of existing boiler infrastructure is driving recurring demand for upgraded burner systems and related equipment. Facilities are increasingly seeking solutions that support accurate temperature regulation while aligning with evolving environmental compliance standards. Continuous technological improvements in burner design also enhance fuel utilization efficiency and reduce maintenance needs. As industrial processes continue to depend heavily on steam and heat generation, the need for advanced industrial burners in boiler systems will remain a major driver supporting the long-term growth of the global industrial burner on boiler market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.27 Billion |

| Forecast Value | $2.67 Billion |

| CAGR | 7.9% |

The monoblock segment reached USD 723.5 million in 2025 and is expected to grow at a CAGR of 7.4% from 2026 through 2035. This design has gained widespread industry acceptance because it integrates key combustion components, including the burner, fan, and control unit, into a single compact system. The unified configuration enables consistent air-fuel mixing, resulting in stable combustion performance and improved thermal efficiency. The compact structure also simplifies installation procedures and reduces servicing complexity, which makes the system attractive for a broad range of industrial heating environments. Demand for space-efficient combustion technologies that offer dependable performance and high energy efficiency continues to accelerate the adoption of monoblock burners. Their ease of operation, reliability, and streamlined maintenance requirements position them as a leading design category within the global industrial burner on boiler industry.

The brownfield segment accounted for 63.36% share in 2025 and is projected to grow at a CAGR of 7.1% from 2026 to 2035. Market leadership of brownfield installations is largely attributed to the rising need to upgrade and modernize existing boiler infrastructure without replacing entire systems. Integrating advanced burner technologies into existing facilities enables industries to enhance combustion efficiency while reducing emissions. This approach enables companies to enhance operational performance while avoiding extended production interruptions and excessive capital investment. Growing attention toward energy optimization, regulatory compliance, and extending the service life of existing industrial equipment continues to drive interest in brownfield projects. The economic practicality and operational advantages of this installation model make it the dominant approach within the industrial burner on boiler market.

China Industrial Burner on Boiler Market reached USD 179 million in 2025 and is expected to grow at a CAGR of 8.1% between 2026 and 2035. Strong industrial activity and continuous expansion of energy-intensive sectors are major contributors to the country's market leadership. Increasing energy requirements across large-scale industrial operations are generating higher demand for efficient combustion technologies capable of delivering reliable heat output. Industrial facilities prioritize burner systems that offer consistent flame stability, precise operational control, and high thermal performance to support uninterrupted production cycles. Government regulations focused on air quality and emission reduction are also encouraging the adoption of advanced burner technologies designed to limit pollutant output and improve fuel efficiency. Additionally, ongoing investments in industrial infrastructure and the modernization of boiler systems continue to stimulate domestic production capabilities. Technological advancements such as automated combustion management systems and flexible fuel operation are further strengthening China's leading position in the Asia Pacific industrial burner on boiler market.

Key companies participating in the Global Industrial Burner on Boiler Market include Alzeta Corporation, Andritz AG, Baltur, Bentone, Ebico, Fives Group, Honeywell International, John Zink Hamworthy Combustion, NIBE Group, Oilon Group Oy, Oxilon Pvt. Ltd., Riello S.p.A., Selas Heat Technology Company, Weishaupt GmbH, and Zeeco, Inc. Companies competing in the Global Industrial Burner on Boiler Market are focusing on multiple strategic initiatives to reinforce their competitive position and expand market reach. Manufacturers are prioritizing research and development activities to introduce advanced combustion technologies that improve efficiency, reduce emissions, and enhance operational reliability. Many companies are also strengthening their manufacturing capabilities and optimizing supply chains to address growing industrial demand. Strategic collaborations with industrial equipment providers and engineering firms help organizations develop tailored burner solutions that meet evolving operational requirements. In addition, businesses are expanding global distribution networks and strengthening after-sales service capabilities to improve customer engagement and long-term client retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for steam and heat in process industries

- 3.2.1.2 Expansion of power generation and cogeneration facilities

- 3.2.1.3 Growth of food processing, chemicals, and pulp and paper industries

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital cost of advanced low-NOx burner systems

- 3.2.2.2 Complex integration with existing boiler and control systems

- 3.2.3 Opportunities

- 3.2.3.1 Rising adoption of dual-fuel and multi-fuel burner technologies

- 3.2.3.2 Integration of digital controls and automation in burner management systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Burner Design, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Monoblock

- 5.3 Duoblock

Chapter 6 Market Estimates & Forecast, By Installation, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Brownfield

- 6.3 Greenfield

Chapter 7 Market Estimates & Forecast, By Power Range, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 < 300 kW

- 7.3 300 kW - 1 MW

- 7.4 1 - 5 MW

- 7.5 5 - 20MW

- 7.6 20 - 50 MW

- 7.7 > 50 MW

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Chemical and petrochemical

- 8.4 Metalworking

- 8.5 Food processing

- 8.6 Textile

- 8.7 Pulp and paper

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alzeta Corporation

- 10.2 Andritz AG

- 10.3 Baltur

- 10.4 Bentone

- 10.5 Ebico

- 10.6 Fives Group

- 10.7 Honeywell International

- 10.8 John Zink Hamworthy Combustion

- 10.9 NIBE Group

- 10.10 Oilon Group Oy

- 10.11 Oxilon Pvt. Ltd.

- 10.12 Riello S.p.A.

- 10.13 Selas Heat Technology Company

- 10.14 Weishaupt GmbH

- 10.15 Zeeco, Inc.

工業燃燒器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

工業燃燒器市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 全球氫氣燃燒器市場

全球氫氣燃燒器市場 工業燃燒器市場:依燃料類型、自動化程度、燃燒器類型、動作溫度、應用、終端用戶產業和地區分類

工業燃燒器市場:依燃料類型、自動化程度、燃燒器類型、動作溫度、應用、終端用戶產業和地區分類 工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測

工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測 2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年

2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年 工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年)

工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年)