|

市場調查報告書

商品編碼

2061418

2026 年至 2035 年法布瑞氏症治療的市場機會、成長要素、產業趨勢分析與預測。Fabry Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

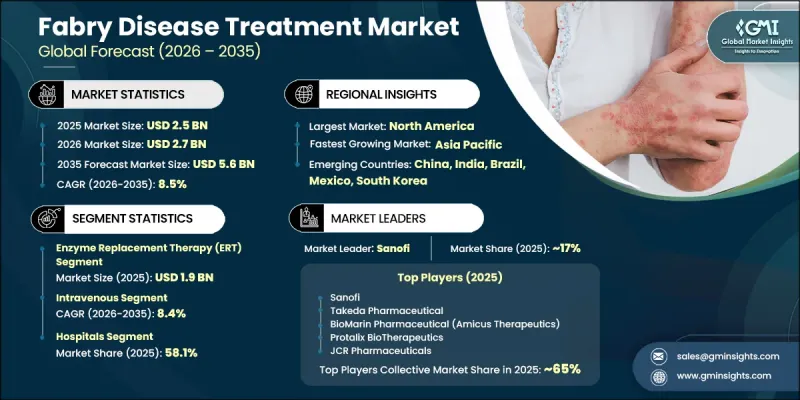

預計到 2025 年,全球法布瑞氏症治療市場價值將達到 25 億美元,並有望以 8.5% 的複合年成長率成長,到 2035 年達到 56 億美元。

未來幾年,對法布瑞氏症先進標靶治療方案的需求不斷成長,預計將顯著推動市場成長。人們對罕見遺傳疾病的認知不斷提高,加上診斷和治療途徑的改善,進一步加速了全球法布瑞氏症治療產業的成長。製藥公司正加大研發投入,致力於推出能改善臨床療效的創新治療方法。醫療基礎設施的完善、對罕見疾病治療的監管支持以及精準醫療解決方案的普及,也促進了市場發展。法布瑞氏症併發症負擔的加重,促使醫療服務提供者採用先進的治療方法,以改善患者的長期管理和生活品質。此外,生物技術和罕見疾病藥物研發的持續進步,正在加速新治療方法的商業化進程,從而提高患者的治療可及性,並增強法布瑞氏症治療產業在整個預測期內的整體成長前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預測金額 | 56億美元 |

| 複合年成長率 | 8.5% |

法布瑞氏症是一種罕見的遺傳性疾病,會影響身體多個器官,包括腎臟、心血管系統、神經系統、皮膚和眼睛。此病由α-半乳糖苷酶A缺乏引起,導致Globotriaosylceramide在體內組織中積聚。法布瑞氏症患者常出現慢性神經痛、皮膚異常、出汗減少和視力相關併發症。目前,酵素替代療法和Chaperone療法是延緩疾病進展和改善患者預後的最常用治療方法。隨著臨床上對早期診斷和長期疾病管理的日益重視,全球對有效治療方法的需求不斷成長。

預計到2025年,酵素替代療法(ERT)市場規模將達到19億美元。此市場成長的主要驅動力是法布瑞氏症診斷率的提高以及酵素替代療法作為治療酵素缺乏症的標準治療方法的廣泛應用。診斷能力的提升和醫護人員對該疾病認知的提高,使得疾病的早期發現成為可能,從而擴大了符合ERT治療條件的患者群體。基因和臨床檢測技術的持續進步也促進了ERT療法在醫療機構中的更廣泛應用。

預計到2025年,醫院將佔據58.1%的市場。醫院作為法布瑞氏症的主要治療場所,繼續發揮主導作用,擁有先進的診斷基礎設施和專業的醫學知識,能夠進行精準的疾病監測和治療。酵素替代療法在醫院環境中的日益普及,進一步推動了該領域的成長,因為這些療法通常需要監督下的靜脈輸液和長期的患者觀察。醫療基礎設施的擴建以及罕見疾病專科治療中心的改善,也進一步強化了醫院在法布瑞氏症治療中的作用。

到2025年,北美法布瑞氏症治療市場將佔據44.8%的佔有率。該地區持續引領市場,這主要得益於眾多成熟生物製藥公司的強大實力、先進罕見疾病治療方法的快速發展,以及高度發展的醫療保健生態系統,該系統支持早期診斷和治療。對研發投入的增加、有利的報銷機制以及罕見疾病治療領域的持續創新,進一步推動了該地區的市場成長。賽諾菲和Amicus Therapeutics等領先企業的存在,也為創新法布瑞氏症治療方案在北美的持續商業化和推廣提供了支持。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 全球範圍內,法布瑞氏症病例正在增加。

- 專家和醫生們的意識日益增強

- 法布瑞氏症治療方法進展

- 健康意識的提高和對早期診斷的需求增加

- 產業潛在風險與挑戰

- 高昂的治療費用

- 治療選擇有限

- 市場機遇

- 下一代基因療法平台的擴展

- 增加對罕見疾病研究和開發的投入,以及推出監管獎勵

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 價格分析

- 產品平臺分析

- 人工智慧和生成式人工智慧對市場的影響

- 監理情勢

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療方法分類,2022-2035年

- 酵素替代療法(ERT)

- Chaperone療法

- 其他治療類型

第6章 市場估計與預測:依給藥途徑分類,2022-2035年

- 靜脈

- 口服

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 居家照護環境

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- BioMarin Pharmaceutical(Amicus Therapeutics)

- Avrobio

- Freeline Therapeutics

- Idorsia Pharmaceuticals

- ISU Abxis

- JCR Pharmaceuticals

- Novartis

- Pfizer

- Protalix BioTherapeutics

- Sanofi

- Takeda Pharmaceuticals

- Viatris

The Global Fabry Disease Treatment Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 5.6 billion by 2035.

Increasing demand for advanced and targeted therapeutic solutions for Fabry disease is expected to significantly support market expansion over the coming years. Rising awareness regarding rare genetic disorders, along with improvements in disease diagnosis and treatment accessibility, continues to strengthen industry growth worldwide. Pharmaceutical companies are increasing investments in research and development activities focused on introducing innovative treatment options with improved clinical outcomes. Expanding healthcare infrastructure, favorable regulatory support for rare disease therapies, and growing availability of precision medicine solutions are also contributing to market development. The increasing burden of Fabry disease-related complications is encouraging healthcare providers to adopt advanced therapeutic approaches that improve long-term patient management and quality of life. In addition, ongoing advancements in biotechnology and rare disease treatment development are accelerating the commercialization of novel therapies, supporting wider patient access and enhancing the overall growth outlook for the Fabry disease treatment industry throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 8.5% |

Fabry disease is a rare hereditary disorder that impacts several organs throughout the body, including the kidneys, cardiovascular system, nervous system, skin, and eyes. The condition develops due to inadequate levels of the alpha-galactosidase A enzyme, leading to the buildup of globotriaosylceramide within body tissues. Patients affected by Fabry disease often experience chronic nerve pain, skin-related abnormalities, reduced sweating, and vision-related complications. Currently, enzyme replacement therapy and chaperone therapy remain the most commonly utilized treatment approaches for managing disease progression and improving patient outcomes. Growing clinical focus on early diagnosis and long-term disease management is further increasing demand for effective treatment solutions worldwide.

The Enzyme Replacement Therapy (ERT) segment reached USD 1.9 billion in 2025. Segment growth is primarily supported by the increasing diagnosis rate of Fabry disease and the widespread adoption of enzyme replacement therapy as a standard treatment approach for addressing enzyme deficiency in affected individuals. Improvements in diagnostic capabilities and expanding awareness among healthcare professionals are enabling earlier identification of the disease, resulting in a larger eligible patient population for ERT-based therapies. Ongoing advancements in genetic testing technologies and laboratory diagnostics are also contributing to increased treatment adoption across healthcare settings.

The hospitals segment accounted for 58.1% share in 2025. Hospitals continue to serve as the primary treatment environment for Fabry disease management due to the availability of advanced diagnostic infrastructure and specialized medical expertise required for accurate disease monitoring and therapy administration. The growing use of enzyme replacement therapy within hospital settings is further supporting segment growth, as these treatments often require supervised infusion procedures and long-term patient observation. Expanding healthcare capabilities and increasing access to specialized rare disease treatment centers are also strengthening the role of hospitals in Fabry disease care.

North America Fabry Disease Treatment Market held a share of 44.8% in 2025. The region continues to maintain a leading market position due to the strong presence of established biopharmaceutical companies, rapid adoption of advanced rare disease therapies, and a highly developed healthcare ecosystem that supports early diagnosis and treatment accessibility. Increasing investments in research activities, favorable reimbursement frameworks, and continuous innovation in rare disease therapeutics are further contributing to regional market growth. The presence of major industry participants such as Sanofi and Amicus Therapeutics is also supporting ongoing commercialization and expansion of innovative Fabry disease treatment solutions across North America.

Leading companies operating in the Global Fabry Disease Treatment Market include Avrobio, BioMarin Pharmaceutical (Amicus Therapeutics), Freeline Therapeutics, Idorsia Pharmaceuticals, ISU Abxis, JCR Pharmaceuticals, Novartis, Pfizer, Protalix BioTherapeutics, Sanofi SA, Takeda Pharmaceuticals, and Viatris. Companies operating in the Fabry disease treatment market are implementing multiple strategic initiatives to strengthen their market position and expand their global presence. Industry participants are heavily investing in research and development activities to introduce advanced therapies with improved efficacy and long-term treatment outcomes. Strategic collaborations, licensing agreements, and partnerships with biotechnology firms are helping companies accelerate drug development and expand product pipelines. Market players are also focusing on expanding clinical trial programs and obtaining regulatory approvals for novel treatment options across multiple regions. Increasing investments in gene therapy research, precision medicine technologies, and rare disease diagnostics are further supporting competitive growth strategies. In addition, companies are strengthening patient support programs, improving treatment accessibility, and expanding manufacturing capabilities to enhance market penetration and reinforce their foothold within the global Fabry disease treatment industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment trends

- 2.2.3 Route of administration trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cases of Fabry disease across the globe

- 3.2.1.2 Growing awareness among specialists and physicians

- 3.2.1.3 Advancements in Fabry disease treatment therapies

- 3.2.1.4 Rising health awareness and demand for early-stage diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Limited treatment options

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of next generation gene therapy platforms

- 3.2.3.2 Growing investment in rare disease R&D and regulatory incentives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Pricing analysis

- 3.6 Product pipeline analysis

- 3.7 Impact of AI and Generation AI on the market

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 MEA

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Enzyme replacement therapy (ERT)

- 5.3 Chaperone treatment

- 5.4 Other treatment types

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Intravenous

- 6.3 Oral

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Homecare settings

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BioMarin Pharmaceutical (Amicus Therapeutics)

- 9.2 Avrobio

- 9.3 Freeline Therapeutics

- 9.4 Idorsia Pharmaceuticals

- 9.5 ISU Abxis

- 9.6 JCR Pharmaceuticals

- 9.7 Novartis

- 9.8 Pfizer

- 9.9 Protalix BioTherapeutics

- 9.10 Sanofi

- 9.11 Takeda Pharmaceuticals

- 9.12 Viatris

法布瑞氏症市場規模、佔有率和成長分析:按療法、給藥途徑、最終用戶、分銷管道、發病時間和地區分類-2026-2033年產業預測

法布瑞氏症市場規模、佔有率和成長分析:按療法、給藥途徑、最終用戶、分銷管道、發病時間和地區分類-2026-2033年產業預測 法布瑞氏症治療市場:依治療類型、給藥途徑、病患人口統計特徵、治療方法、最終使用者和通路分類-2026-2032年全球市場預測

法布瑞氏症治療市場:依治療類型、給藥途徑、病患人口統計特徵、治療方法、最終使用者和通路分類-2026-2032年全球市場預測 法布瑞氏症治療市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物、治療方法、給藥途徑、分銷管道、地區和競爭格局分類,2021-2031年

法布瑞氏症治療市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物、治療方法、給藥途徑、分銷管道、地區和競爭格局分類,2021-2031年 法布瑞氏症:全球市場展望、流行病學、競爭格局與市場預測報告(32個主要市場),2025-2035年法布瑞氏症:新型療法、未滿足的需求與TPP洞察報告,2026年法布瑞氏症:市場展望、流行病學、競爭格局、市場預測報告(2025-2035年)

法布瑞氏症:全球市場展望、流行病學、競爭格局與市場預測報告(32個主要市場),2025-2035年法布瑞氏症:新型療法、未滿足的需求與TPP洞察報告,2026年法布瑞氏症:市場展望、流行病學、競爭格局、市場預測報告(2025-2035年) 法布瑞氏症市場報告:按類型、診斷和治療、最終用戶和地區分類(2026-2034 年)

法布瑞氏症市場報告:按類型、診斷和治療、最終用戶和地區分類(2026-2034 年) 全球法布瑞氏症治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球法布瑞氏症治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 法布瑞氏症治療市場規模、佔有率及產業分析報告:依給藥途徑、治療方法、通路、地區,預測至2025-2034年

法布瑞氏症治療市場規模、佔有率及產業分析報告:依給藥途徑、治療方法、通路、地區,預測至2025-2034年 法布瑞氏症治療市場規模、佔有率和趨勢分析報告:按解決方案、治療方法、給藥途徑、分銷管道、地區和細分市場預測,2024-2030年

法布瑞氏症治療市場規模、佔有率和趨勢分析報告:按解決方案、治療方法、給藥途徑、分銷管道、地區和細分市場預測,2024-2030年