|

市場調查報告書

商品編碼

2061386

獸醫服務市場機會、成長要素、產業趨勢分析及2026-2035年預測。Veterinary Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

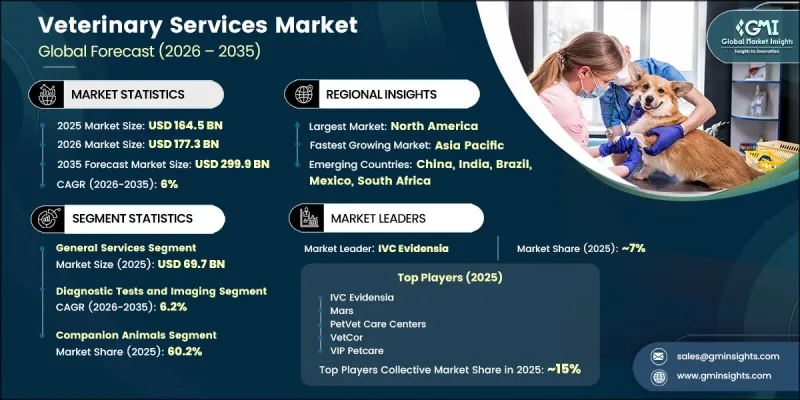

2025年全球獸醫服務市場價值為1,645億美元,預計到2035年將以6%的複合年成長率成長至2,999億美元。

全球動物數量的持續成長、寵物擁有率的上升、消費者在動物保健方面的支出增加,以及開發中國家和已開發國家獸醫服務可及性的提高,共同推動了市場成長。人們對伴侶偏好的日益青睞和動物福利意識的增強,正在促進獸醫和預防保健解決方案的支出。獸醫服務涵蓋一系列旨在維護伴侶動物和牲畜健康福祉的醫療保健活動。這些服務包括預防醫學、常規健康監測、疫苗接種計劃、外科手術、生殖醫學、診斷評估、牙科護理、動物諮詢和疾病管理解決方案。獸醫機構持續推進的數位轉型正在提高營運效率,並實現對醫療記錄和患者管理系統的無縫存取。寵物保險的日益普及,加上可支配收入的增加以及寵物「擬人化」觀念的日益增強,進一步鼓勵消費者投資於先進的獸醫服務和優質的寵物醫療保健解決方案。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1645億美元 |

| 預計金額 | 2999億美元 |

| 複合年成長率 | 6% |

預計到2025年,綜合獸醫服務市場規模將達到697億美元。該市場涵蓋旨在維護動物健康和提供長期預防保健的基礎醫療服務。人們對預防性獸醫護理和定期健康監測的日益重視是推動該市場成長的主要因素。消費者對改善動物生活品質的日益關注以及對綜合健康服務需求的不斷成長,持續推動全球市場對綜合獸醫解決方案的採用。

預計2026年至2035年間,診斷檢測和影像領域將以6.2%的複合年成長率成長。動物感染疾病和慢性病的日益普及推動了對先進獸醫診斷技術和影像解決方案的需求。對疾病早期發現、精準監測和有效治療方案的日益重視,正在加速獸醫診所和動物保健機構對診斷服務的應用。獸醫影像和臨床實驗室技術的進步也為市場擴張提供了支持。

預計到2025年,美國獸醫服務市場規模將達到641億美元。該地區強勁的市場成長主要得益於寵物飼養量的增加、先進的獸醫基礎設施以及專業動物醫療保健服務的廣泛普及。消費者在伴侶動物照護方面的支出不斷成長、預防性獸醫保健意識的提高以及對專業醫療保健服務需求的持續成長,都將繼續推動北美地區的市場擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 動物疾病增加

- 寵物飼養量增加

- 寵物保險滲透率提高

- 獸醫學進展

- 產業潛在風險與挑戰

- 獸醫服務成本不斷上漲

- 熟練人員短缺

- 市場機遇

- 遠端醫療和虛擬護理生態系統的擴展

- 將再生醫學與先進醫療技術整合到臨床實務中

- 促進因素

- 成長潛力分析

- 技術展望

- 最新科技趨勢

- 新興技術

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 救贖方案

- 各國寵物數量

- 未來市場趨勢

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 總務

- 專業服務

- 緊急服務

第6章 市場估計與預測:依服務業分類,2022-2035年

- 診斷測試和影像

- 身體健康監測

- 外科手術

- 疫苗接種

- 美容

- 寵物住宿和日托

- 寵物健身

- 其他服務

第7章 市場估計與預測:依動物類型分類,2022-2035年

- 伴侶動物

- 狗

- 貓

- 馬

- 其他伴侶動物

- 家畜

- 牛

- 豬

- 家禽

- 綿羊和山羊

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- CVS Group

- Ethos Veterinary Health

- Greencross Limited

- Heartland Veterinary Partners

- IDEXX Laboratories

- IVC Evidensia

- VCA Animal Hospitals Inc.

- Kremer Veterinary Services

- Mars Incorporated

- VIP Petcare

- PetVet Care Centers

- PetIQ

- VetCor

- VetPartners

The Global Veterinary Services Market was valued at USD 164.5 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 299.9 billion by 2035.

Market growth is fueled by the steadily increasing global animal population, rising pet ownership rates, growing consumer spending on animal healthcare, and broader access to veterinary care services across developing and developed economies. Increasing preference for companion animals and higher awareness regarding animal wellbeing are encouraging greater expenditure on veterinary treatments and preventive healthcare solutions. Veterinary services encompass a broad range of healthcare activities focused on maintaining the health and wellness of companion and livestock animals. These services include preventive care, routine health monitoring, vaccination programs, surgical procedures, reproductive healthcare, diagnostic evaluations, dental treatments, animal consulting, and disease management solutions. Ongoing digital transformation across veterinary facilities is improving operational efficiency and enabling seamless access to medical records and patient management systems. The growing popularity of pet insurance coverage, combined with rising disposable income levels and increased humanization of pets, is further encouraging consumers to invest in advanced veterinary care services and premium healthcare solutions for animals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $164.5 Billion |

| Forecast Value | $299.9 Billion |

| CAGR | 6% |

The general veterinary services segment reached USD 69.7 billion in 2025. This segment includes essential healthcare services aimed at maintaining animal wellness and supporting long-term preventive care. Rising awareness regarding preventive veterinary care and regular health monitoring is significantly contributing to segment growth. Increasing consumer focus on improving animal quality of life and expanding demand for comprehensive wellness services continue to support the adoption of general veterinary healthcare solutions across global markets.

The diagnostic tests and imaging segment is projected to grow at a CAGR of 6.2% during 2026-2035. The increasing prevalence of infectious and chronic diseases among animals is driving the demand for advanced veterinary diagnostic technologies and imaging solutions. Growing emphasis on early disease identification, accurate monitoring, and effective treatment planning is accelerating the adoption of diagnostic services across veterinary clinics and animal healthcare facilities. Technological advancements in veterinary imaging and laboratory testing capabilities are also strengthening market expansion.

U.S. Veterinary Services Market was valued at USD 64.1 billion in 2025. Strong market growth across the region is primarily supported by increasing pet ownership, advanced veterinary infrastructure, and widespread availability of specialized animal healthcare services. Growing consumer spending on companion animal care, rising awareness regarding preventive veterinary treatments, and increasing demand for specialized healthcare services continue to drive market expansion throughout North America.

Key companies operating in the Global Veterinary Services Market include CVS Group, Ethos Veterinary Health, Greencross Limited, Heartland Veterinary Partners, IDEXX Laboratories, IVC Evidensia, VCA Animal Hospitals Inc., Kremer Veterinary Services, Mars Incorporated, VIP Petcare, PetVet Care Centers, PetIQ, VetCor, and VetPartners. Companies operating in the veterinary services market are increasingly adopting strategic initiatives to strengthen their market presence and improve competitive positioning. Industry participants are focusing on expanding veterinary clinic networks, investing in advanced diagnostic technologies, and enhancing digital healthcare capabilities to improve operational efficiency and patient care. Strategic partnerships, mergers, and acquisitions are helping organizations broaden their service portfolios and increase geographic reach. Companies are also emphasizing telehealth solutions, electronic medical record systems, and AI-driven diagnostic tools to streamline veterinary operations and improve customer experience. In addition, rising investments in specialized animal healthcare services, workforce training programs, and preventive care solutions are supporting long-term business growth. Many market players are further prioritizing customer retention through premium wellness programs, subscription-based healthcare models, and integrated pet care services to strengthen brand loyalty and market share.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Service type trends

- 2.2.4 Animal type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of animal diseases

- 3.2.1.2 Rising pet adoption

- 3.2.1.3 Increasing penetration of pet insurance

- 3.2.1.4 Advancements in veterinary medicine

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Increasing cost of veterinary services

- 3.2.2.2 Lack of skilled personnel

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of telemedicine and virtual care ecosystems

- 3.2.3.2 Integration of regenerative and advanced therapies in clinical practice

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Reimbursement scenario

- 3.7 Pet population, by country

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 General services

- 5.3 Specialty services

- 5.4 Emergency services

Chapter 6 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic tests and imaging

- 6.3 Physical health monitoring

- 6.4 Surgery

- 6.5 Vaccination

- 6.6 Grooming

- 6.7 Pet boarding and daycare

- 6.8 Pet fitness

- 6.9 Other services

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Sheep and goats

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 CVS Group

- 9.2 Ethos Veterinary Health

- 9.3 Greencross Limited

- 9.4 Heartland Veterinary Partners

- 9.5 IDEXX Laboratories

- 9.6 IVC Evidensia

- 9.7 VCA Animal Hospitals Inc.

- 9.8 Kremer Veterinary Services

- 9.9 Mars Incorporated

- 9.10 VIP Petcare

- 9.11 PetVet Care Centers

- 9.12 PetIQ

- 9.13 VetCor

- 9.14 VetPartners

獸醫服務市場-全球產業規模、佔有率、趨勢、機會和預測:按動物類型、服務類型、地區和競爭對手分類,2021-2031年

獸醫服務市場-全球產業規模、佔有率、趨勢、機會和預測:按動物類型、服務類型、地區和競爭對手分類,2021-2031年 獸醫保健服務市場規模、佔有率和趨勢分析報告:按動物、服務、地區和細分市場分類(2026-2033 年)

獸醫保健服務市場規模、佔有率和趨勢分析報告:按動物、服務、地區和細分市場分類(2026-2033 年) 獸醫保健服務市場:依動物種類、服務類型、診所類型和客戶類型分類-2026-2032年全球市場預測

獸醫保健服務市場:依動物種類、服務類型、診所類型和客戶類型分類-2026-2032年全球市場預測 獸醫服務市場報告:按服務、動物類型、最終用途和地區分類,2026-2034 年

獸醫服務市場報告:按服務、動物類型、最終用途和地區分類,2026-2034 年 獸醫服務市場規模、佔有率和成長分析(按動物類型、服務類型和地區分類)-2026-2033年產業預測美國獸醫服務市場規模、佔有率和趨勢分析報告:按動物、服務、消費行為、主要企業、競爭分析和細分預測,2025-2033 年

獸醫服務市場規模、佔有率和成長分析(按動物類型、服務類型和地區分類)-2026-2033年產業預測美國獸醫服務市場規模、佔有率和趨勢分析報告:按動物、服務、消費行為、主要企業、競爭分析和細分預測,2025-2033 年 美國的獸醫學服務(第5版) - 寵物照護客戶獲得競爭

美國的獸醫學服務(第5版) - 寵物照護客戶獲得競爭 獸醫服務市場:依服務類型、動物類型、地區

獸醫服務市場:依服務類型、動物類型、地區 按動物類型、服務類型、交付管道、地區、範圍和預測劃分的獸醫服務市場規模

按動物類型、服務類型、交付管道、地區、範圍和預測劃分的獸醫服務市場規模