|

市場調查報告書

商品編碼

2061320

自動自吸式排水幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測Auto Prime Dewatering Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

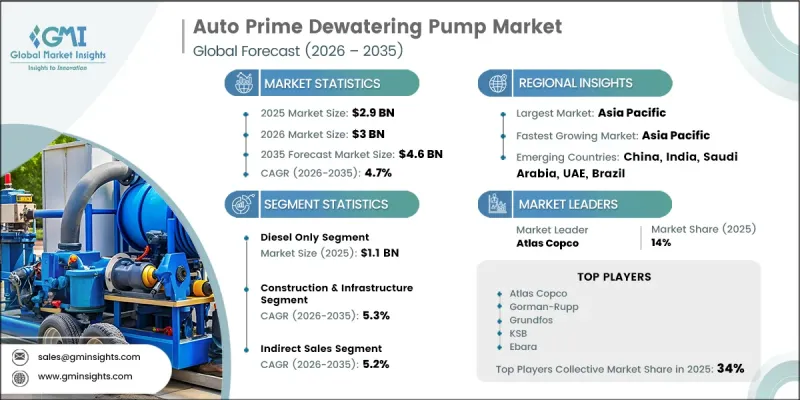

2025 年全球自吸式排水幫浦市場價值 29 億美元,預計到 2035 年將以 4.7% 的複合年成長率成長至 46 億美元。

全球自吸式排水泵產業正經歷穩定成長,這主要得益於多個工業領域對先進水資源管理系統需求的不斷成長。日益頻繁的淹水、緊急排水需求以及對高效流體處理解決方案日益成長的需求,共同為自吸式排水泵創造了有利的市場環境。此外,工業活動的增加和資源開採投資的增加也顯著促進了市場成長,因為高效的排水系統對於持續運作至關重要。泵浦工程、自動化系統和運作效率的技術進步進一步推動了這些產品在全球的應用。現代自吸式排水泵無需持續人工操作即可自主運作,因此在整體工業應用中都獲得了廣泛認可。此外,減少水資源浪費、提高營運效率和降低維護需求的日益成長的關注也支持長期市場需求。更高的能源效率、更耐用的泵體結構和更先進的自動化功能也推動了自吸式排水系統在全球基礎設施、工業和市政項目中的應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 29億美元 |

| 預測金額 | 46億美元 |

| 複合年成長率 | 4.7% |

受高效水資源管理和廢水管理日益成長的需求推動,全球自吸式排水泵市場正經歷強勁成長。先進的泵浦技術在提高整體能源效率的同時,簡化了維護程序,這對於致力於最佳化營運和實踐永續水資源管理的產業而言至關重要。在全球範圍內,節水和提高排水效率的努力顯著加速了自吸式排水泵的普及應用。基礎設施建設項目、工業項目和市政排水工程的需求不斷成長,也促進了市場擴張,因為這些系統在維持工作流程的連續性以及最大限度地減少因積水造成的中斷方面發揮著至關重要的作用。

到2025年,純柴油動力市場規模將達到11億美元。由於柴油驅動系統性能可靠,即使在電力供應有限的地區也能高效運作,因此市場對其需求仍然強勁。此外,柴油運作系統能夠承受高負載運行,使其成為大規模工業和基礎設施應用的理想選擇。

預計到2025年,建築與基礎設施產業將佔全球市場佔有率的33.7%,並在2026年至2035年間維持5.3%的複合年成長率。該行業的成長主要得益於全球範圍內快速的城市擴張和日益成長的基礎設施建設活動。對自吸式排水泵的需求持續上升。這些系統能夠有效防止建築工地積水,避免施工中斷,並提高施工效率。

預計到2025年,美國自吸式排水幫浦市場將佔據81%的市場佔有率,市場規模將達到5.969億美元。全國範圍內的市場成長主要得益於基礎建設活動的活性化和對排水管理系統投資的擴展。建築項目的擴張以及人們對災害管理解決方案日益成長的興趣,都促使市場對高效排水技術的需求不斷成長。此外,極端天氣事件的頻繁發生和降雨量的增加,也進一步推動了對能夠支持緊急排水應變和業務連續性的先進排水泵系統的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 價格趨勢

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理框架

- 北美:EPA排放法規、OSHA 現場安全標準和 ANSI/HI 泵浦標準。

- 歐洲:歐盟機械指令、ATEX 指令和 CE 標誌要求

- 亞太地區:區域環境排放標準與礦山安全法規

- 中東和非洲:石油和天然氣 (O&G) 產業的 ATEX/IECEx 合規性和 GCC GSO/SASO 標準

- 全球永續發展要求:排放目標和噪音法規對柴油汽車起步的影響

- 波特五力分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依動力來源,2022-2035年

- 僅限柴油

- 僅電力

- 柴油-電力雙碟

- 液壓驅動

第6章 市場估價與預測:依卸貨港規模分類,2022-2035年

- 4吋/100毫米

- 6吋/150毫米

- 8吋/200毫米

- 10吋/250毫米

- 12吋或更大/300毫米或更大

第7章 市場估算與預測:依流量與容量分類,2022-2035年

- 200立方米/小時或更少

- 201~400 m3/h

- 401~600 m3/h

- 超過 600 立方米/小時

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 建築和基礎設施

- 採礦和採石

- 石油、天然氣和煉油廠

- 供水/污水處理

- 工業製造

- 其他(國防/軍事、農業/灌溉等)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- 全球主要公司

- Atlas Copco

- Ebara

- Flowserve Corporation

- Gorman-Rupp

- Grundfos Holding

- KSB

- Sulzer

- 當地公司

- Cosmos Pumps

- Esdhar Dewatering Solution

- Logic Dewatering KSA

- Rover Industry

- Sky Dewatering

- SPP Pumps

- Thompson Pump

- 新興企業和專業公司

- DEFU Pumps

- HCP Pump

- MBH Pumps

- Remko Pumps

- SB Pumps India

- Solidpump

- Truflo Pumping Systems

The Global Auto Prime Dewatering Pump Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 4.6 billion by 2035.

The global auto prime dewatering pump industry is witnessing steady expansion due to the growing requirement for advanced water management systems across multiple industrial sectors. Increasing incidents of water accumulation, emergency drainage requirements, and rising demand for efficient fluid handling solutions are creating favorable market conditions for auto-prime dewatering pumps. Expanding industrial operations and rising investments in resource extraction activities are also contributing significantly to market growth, as efficient water removal systems remain essential for uninterrupted operations. Technological progress in pump engineering, automation systems, and operational efficiency is further strengthening product adoption worldwide. Modern auto-prime dewatering pumps are designed to operate independently without requiring continuous manual intervention, making them highly preferred across industrial applications. In addition, increasing focus on reducing water wastage, improving operational productivity, and lowering maintenance requirements is supporting long-term demand. Enhanced energy efficiency, durable pump configurations, and advanced automation capabilities are also driving broader acceptance of auto-prime dewatering systems across infrastructure, industrial, and municipal operations globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 4.7% |

The global auto prime dewatering pump market is experiencing strong momentum due to increasing emphasis on efficient water control and drainage management. Advanced pump technologies are improving overall energy efficiency while simplifying maintenance procedures, which is becoming increasingly important for industries focused on operational optimization and sustainable water management practices. Growing efforts to improve water conservation and drainage efficiency have significantly accelerated the adoption of auto-prime dewatering pumps across worldwide markets. Rising demand from infrastructure development activities, industrial projects, and municipal drainage operations is also contributing to market expansion, as these systems play an essential role in maintaining continuous operational workflows and minimizing disruptions caused by water accumulation.

In 2025, the diesel-only segment accounted for USD 1.1 billion. Demand for diesel-powered systems remains strong due to their dependable performance and ability to operate effectively in locations with limited power availability. Their capability to handle intensive operational workloads also makes them highly suitable for large-scale industrial and infrastructure-related applications.

The construction and infrastructure segment held a 33.7% share in 2025 and is expected to register a CAGR of 5.3% between 2026 and 2035. Growth within this segment is being driven by rapid urban expansion and the increasing number of infrastructure development activities taking place globally. Demand for auto-prime dewatering pumps continues to rise because these systems effectively prevent water buildup at project locations, ensuring uninterrupted operations and improved construction efficiency.

United States Auto Prime Dewatering Pump Market accounted for 81% share and generated USD 596.9 million in 2025. Market growth across the country is being supported by rising infrastructure development activities and increasing investments in drainage management systems. Expanding construction operations and growing focus on disaster management solutions are contributing to higher demand for efficient dewatering technologies. In addition, recurring extreme weather conditions and rising precipitation levels are further strengthening the requirement for advanced dewatering pump systems capable of supporting emergency water removal and operational continuity.

Key companies operating in the Auto Prime Dewatering Pump Market include Atlas Copco, Ebara, Flowserve Corporation, Gorman-Rupp, Grundfos Holding, KSB, Sulzer, Cosmos Pumps, Esdhar Dewatering Solution, Logic Dewatering KSA, Rover Industry, Sky Dewatering, SPP Pumps, Thompson Pump, DEFU Pumps, HCP Pump, MBH Pumps, Remko Pumps, SB Pumps India, Solidpump, and Truflo Pumping Systems. Companies active in the auto prime dewatering pump industry are focusing on product innovation, expansion of distribution networks, and technological advancements to strengthen their market presence. Manufacturers are investing in energy-efficient pump technologies, automated monitoring systems, and durable product designs to improve operational performance and reduce maintenance costs. Strategic collaborations, regional expansion initiatives, and partnerships with infrastructure and industrial contractors are helping companies broaden their customer base and enhance market reach. Many players are also prioritizing research and development activities to introduce advanced pumping solutions with improved efficiency, higher reliability, and greater automation capabilities.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power source

- 2.2.3 Discharge port diameter

- 2.2.4 Flow rate capacity

- 2.2.5 End use industry

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 North America: EPA Discharge Regulations, OSHA Site Safety & ANSI/HI Pump Standards

- 3.5.2 Europe: EU Machinery Directive, ATEX Directive & CE Marking Requirements

- 3.5.3 Asia Pacific: Regional Environmental Discharge Standards & Mining Safety Regulations

- 3.5.4 Middle East & Africa: ATEX / IECEx Compliance for O&G Sector & GCC GSO/SASO Standards

- 3.5.5 Global Sustainability Mandates: Emissions Targets & Noise Ordinance Impact on Diesel Auto-Prime

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade Data Analysis (Based on Paid Database) (HS Code: 8413)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Diesel only

- 5.3 Electric only

- 5.4 Diesel-electric dual drive

- 5.5 Hydraulic drive

Chapter 6 Market Estimates & Forecast, By Discharge Port Diameter, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 4-Inch / 100mm

- 6.3 6-Inch / 150mm

- 6.4 8-Inch / 200mm

- 6.5 10-Inch / 250mm

- 6.6 12-Inch & above / 300mm+

Chapter 7 Market Estimates & Forecast, By Flow Rate Capacity, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 200 m3/hr

- 7.3 201-400 m3/hr

- 7.4 401-600 m3/hr

- 7.5 Above 600 m3/hr

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Construction & infrastructure

- 8.3 Mining & quarrying

- 8.4 Oil, gas & refineries

- 8.5 Municipal & wastewater

- 8.6 Industrial manufacturing

- 8.7 Others (defense & military, agriculture & irrigation etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global key players

- 11.1.1 Atlas Copco

- 11.1.2 Ebara

- 11.1.3 Flowserve Corporation

- 11.1.4 Gorman-Rupp

- 11.1.5 Grundfos Holding

- 11.1.6 KSB

- 11.1.7 Sulzer

- 11.2 Regional Players

- 11.2.1 Cosmos Pumps

- 11.2.2 Esdhar Dewatering Solution

- 11.2.3 Logic Dewatering KSA

- 11.2.4 Rover Industry

- 11.2.5 Sky Dewatering

- 11.2.6 SPP Pumps

- 11.2.7 Thompson Pump

- 11.3 Emerging/Niche Specialists

- 11.3.1 DEFU Pumps

- 11.3.2 HCP Pump

- 11.3.3 MBH Pumps

- 11.3.4 Remko Pumps

- 11.3.5 SB Pumps India

- 11.3.6 Solidpump

- 11.3.7 Truflo Pumping Systems

礦用泵浦市場規模、佔有率和成長分析:按泵浦類型、驅動系統、應用、最終用戶、安裝類型和地區分類-2026-2033年產業預測

礦用泵浦市場規模、佔有率和成長分析:按泵浦類型、驅動系統、應用、最終用戶、安裝類型和地區分類-2026-2033年產業預測 脫水泵浦市場規模、佔有率、趨勢和預測:按類型、容量、應用和地區分類,2026-2034年

脫水泵浦市場規模、佔有率、趨勢和預測:按類型、容量、應用和地區分類,2026-2034年 礦用排水泵市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測全球排水泵市場機會、成長要素、產業趨勢分析及2026-2035年預測。

礦用排水泵市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測全球排水泵市場機會、成長要素、產業趨勢分析及2026-2035年預測。 脫水泵浦市場:按泵浦類型、技術、驅動系統、設計、額定功率、材質和最終用途產業分類-2026-2032年全球預測

脫水泵浦市場:按泵浦類型、技術、驅動系統、設計、額定功率、材質和最終用途產業分類-2026-2032年全球預測 排水泵市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、最終用途產業、泵浦類型、地區和競爭格局分類,2021-2031年)全球建築幫浦市場(按泵浦類型、動力來源、運作方式、最終用途產業和銷售管道分類)預測(2026-2032年)

排水泵市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、最終用途產業、泵浦類型、地區和競爭格局分類,2021-2031年)全球建築幫浦市場(按泵浦類型、動力來源、運作方式、最終用途產業和銷售管道分類)預測(2026-2032年) 建築幫浦市場規模、佔有率和成長分析(按產品類型、功率、容量、分銷管道和地區分類)-2026-2033年產業預測

建築幫浦市場規模、佔有率和成長分析(按產品類型、功率、容量、分銷管道和地區分類)-2026-2033年產業預測 全球排水泵市場全球採礦幫浦市場

全球排水泵市場全球採礦幫浦市場