|

市場調查報告書

商品編碼

2027598

全球排水泵市場機會、成長要素、產業趨勢分析及2026-2035年預測。Global Dewatering Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

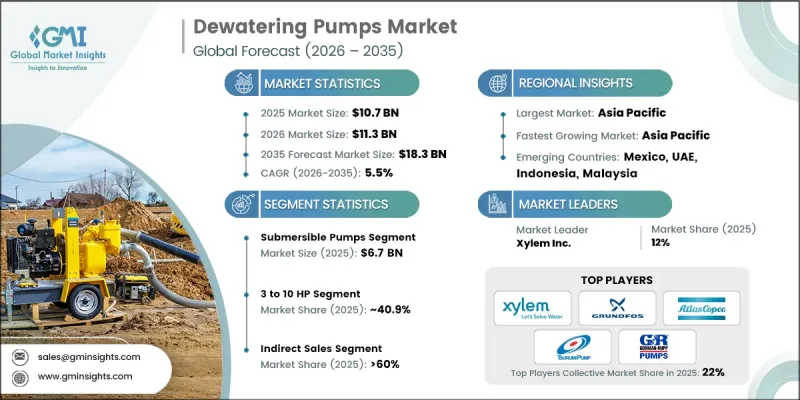

預計到 2025 年,全球排水幫浦市場價值將達到 107 億美元,並預計以 5.5% 的複合年成長率成長,到 2035 年達到 183 億美元。

採礦和金屬產業是市場成長的主要驅動力,無論在地上或地下作業中,持續排水都至關重要,以維持營運穩定性、保障工人安全並最佳化設備性能。工業化和電氣化,以及全球對銅、鋰、鎳等金屬需求的成長,正推動採礦作業向更深、更複雜的區域擴展,加劇水資源管理的挑戰。這促使市場對先進的排水解決方案產生需求,這些解決方案需要配備高容量、耐磨損且即使在惡劣環境下也能連續運作的水泵。遵守包括美國環保署 (EPA) 等機構制定的環境標準在內的各項法規,進一步加速了高效、永續水泵系統的應用,從而最大限度地減少停機時間,提高生產效率,並符合環境法規的要求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 107億美元 |

| 預測金額 | 183億美元 |

| 複合年成長率 | 5.5% |

預計到2025年,潛水泵浦市場規模將達到67億美元。其優點在於運作效率高、用途廣泛,無需引水,即使浸沒在水中也能直接運作。這使得潛水泵能夠快速部署,並在極少監控的情況下持續運行,因此非常適合建築、城市排水、採礦和地下作業等應用。其緊湊的設計使其能夠適應空間限制和水位波動,從而促進了其在眾多工業領域的應用。

預計到2025年,3-10馬力功率段的泵浦將佔據40.9%的市場佔有率,並繼續保持最具商業性前景的功率範圍。此功率段的泵浦在動力、效率和柔軟性實現了理想的平衡,適用於中型建築專案、城市排水和礦山輔助作業。它們能夠在保持能源效率的同時處理大量水,易於安裝、便於攜帶,並且高度適用於租賃和短期部署模式。持續的產品創新進一步鞏固了其市場主導地位,提高了可靠性和耐用性,並降低了維護需求。

預計到2025年,亞太地區排水幫浦市場佔有率將達到38%,並在2026年至2035年間以5.9%的複合年成長率成長。中國是推動區域市場成長的主要力量,這得益於大規模基礎設施項目、城市擴張和工業發展對持續排水解決方案的需求。採礦和地下設施(例如地鐵建設和公共產業開發)也進一步刺激了市場需求。強大的國內製造業基礎使得泵浦的生產更具成本效益,並能快速部署到各種規模的專案中。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 快速的都市化和建設活動的擴張

- 採礦和金屬產業的擴張

- 擴大石油和天然氣探勘和生產

- 產業潛在風險與挑戰

- 大筆初始投資

- 設備因磨損和堵塞而故障

- 機會

- 新興市場的基礎建設

- 智慧泵系統與物聯網整合

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 各地區價格波動

- 監理情勢

- 波特的分析

- PESTEL 分析

- 貿易數據分析(基於付費資料庫)

- 進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易走廊及關稅影響(基於付費資料庫)

- 區域貿易平衡

- 貿易協定的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 預測性維護的應用

- 設計最佳化與仿真

- 供應鏈情報

- 風險、限制和監管考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業市佔率分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 潛水泵

- 非潛水泵/地面泵

第6章 市場估計與預測:依產能分類,2022-2035年

- 3馬力或以下

- 3~10 HP

- 10~50 HP

- 超過 50 匹馬力

第7章 市場估計與預測:依最終用途產業分類,2022-2035年

- 建造

- 採礦和金屬

- 地方政府

- 石油和天然氣

- 發電

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Atlas Copco AB

- Cornell Pump Company

- Ebara Corporation

- Flowserve Corporation

- Franklin Electric Co. Inc.

- Gorman-Rupp Company

- Grundfos

- Homa Pumpen GmbH

- KSB SE &Co. KGaA

- Parker Hannifin Corporation

- Sulzer Ltd.

- Thompson Pump

- Tsurumi Manufacturing

- Wacker Neuson SE

- Weir Group PLC

- WILO SE

- Xylem Inc.

The Global Dewatering Pumps Market was valued at USD 10.7 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 18.3 billion by 2035.

The market's growth is driven by the mining and metals sector, where both surface and underground operations require continuous water removal to maintain operational stability, protect worker safety, and optimize equipment performance. Rising industrialization, electrification, and global demand for metals like copper, lithium, and nickel have pushed mining operations into deeper and more complex geographies, increasing water management challenges. These conditions have fueled demand for advanced dewatering solutions with high-capacity, abrasion-resistant pumps capable of operating continuously under harsh environments. Regulatory compliance, including environmental standards from agencies like the U.S. EPA, has further accelerated the adoption of efficient, sustainable pumping systems, ensuring minimal downtime, improved productivity, and adherence to environmental mandates.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.7 Billion |

| Forecast Value | $18.3 Billion |

| CAGR | 5.5% |

In 2025, the submersible pumps segment generated USD 6.7 billion. Their dominance stems from operational efficiency and versatility, allowing them to function directly in flooded conditions without priming. This enables faster deployment and continuous operation with minimal supervision, making submersible pumps ideal for construction, municipal drainage, mining, and underground applications. Their compact design accommodates space constraints and variable water levels, driving widespread adoption across industries.

The 3 to 10 HP capacity segment held 40.9% share in 2025 and is projected to remain the most commercially viable range. Pumps within this horsepower category strike an ideal balance between power, efficiency, and flexibility, catering to medium-scale construction projects, municipal drainage, and mining support operations. They handle significant water volumes while maintaining energy efficiency, offering easy installation, portability, and compatibility with rental or short-term deployment models. Continuous product innovation has enhanced reliability, durability, and reduced maintenance requirements, reinforcing their leading market position.

Asia Pacific Dewatering Pumps Market held a 38% share in 2025 and is expected to grow at a CAGR of 5.9% from 2026 to 2035. China leads the regional market, supported by extensive infrastructure projects, urban expansion, and industrial developments requiring consistent dewatering solutions. Mining operations and underground facilities, such as metro construction and utility development, further drive demand. A strong domestic manufacturing base enables cost-efficient production and rapid deployment of pumps across diverse project scales.

Key players in the Global Dewatering Pumps Market include Atlas Copco AB, Cornell Pump Company, Ebara Corporation, Flowserve Corporation, Franklin Electric Co. Inc., Gorman-Rupp Company, Grundfos, Homa Pumpen GmbH, KSB SE & Co. KGaA, Parker Hannifin Corporation, Sulzer Ltd., Thompson Pump, Tsurumi Manufacturing, Wacker Neuson SE, Weir Group PLC, WILO SE, and Xylem Inc. Companies in the dewatering pumps industry strengthen their market position through continuous innovation in high-capacity, abrasion-resistant, and energy-efficient pump technologies. Strategic alliances with mining, construction, and municipal infrastructure firms enhance market reach. R&D investments enable improved durability, wear resistance, and adaptability to extreme conditions. Expanding service networks and providing maintenance, remote diagnostics, and rapid deployment capabilities build customer trust. Manufacturers also focus on regional production facilities for cost-effective delivery, targeted marketing campaigns, and participation in trade exhibitions to boost visibility and strengthen global brand presence, ensuring competitiveness in a rapidly growing market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Capacity

- 2.2.4 End use industry

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & growing construction activities

- 3.2.1.2 Expansion of mining & metals sector

- 3.2.1.3 Growing oil & gas exploration & production

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Equipment failure due to abrasive wear & clogging

- 3.2.3 Opportunities

- 3.2.3.1 Emerging markets infrastructure development

- 3.2.3.2 Smart pumping systems & IoT integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Regional price variations

- 3.7 Regulatory landscape

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Paid Data Base)

- 3.10.1 Import/export volume & value trends (Driven by Paid Data Base)

- 3.10.2 Key trade corridors & tariff impact (Driven by Paid Data Base)

- 3.10.3 Regional trade balance

- 3.10.4 Impact of trade agreements

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Predictive maintenance applications

- 3.11.4 Design optimization & simulation

- 3.11.5 Supply chain intelligence

- 3.11.6 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Latin America

- 4.3.1.5 Middle East and Africa

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Submersible pumps

- 5.3 Non-submersible/surface pumps

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Up to 3 HP

- 6.3 3 to 10 HP

- 6.4 10 to 50 HP

- 6.5 Above 50 HP

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Mining & metals

- 7.4 Municipal

- 7.5 Oil & gas

- 7.6 Power generation

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Atlas Copco AB

- 10.2 Cornell Pump Company

- 10.3 Ebara Corporation

- 10.4 Flowserve Corporation

- 10.5 Franklin Electric Co. Inc.

- 10.6 Gorman-Rupp Company

- 10.7 Grundfos

- 10.8 Homa Pumpen GmbH

- 10.9 KSB SE & Co. KGaA

- 10.10 Parker Hannifin Corporation

- 10.11 Sulzer Ltd.

- 10.12 Thompson Pump

- 10.13 Tsurumi Manufacturing

- 10.14 Wacker Neuson SE

- 10.15 Weir Group PLC

- 10.16 WILO SE

- 10.17 Xylem Inc.

礦用泵浦市場規模、佔有率和成長分析:按泵浦類型、驅動系統、應用、最終用戶、安裝類型和地區分類-2026-2033年產業預測

礦用泵浦市場規模、佔有率和成長分析:按泵浦類型、驅動系統、應用、最終用戶、安裝類型和地區分類-2026-2033年產業預測 脫水泵浦市場規模、佔有率、趨勢和預測:按類型、容量、應用和地區分類,2026-2034年

脫水泵浦市場規模、佔有率、趨勢和預測:按類型、容量、應用和地區分類,2026-2034年 自動自吸式排水幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測礦用排水泵市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測

自動自吸式排水幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測礦用排水泵市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測 脫水泵浦市場:按泵浦類型、技術、驅動系統、設計、額定功率、材質和最終用途產業分類-2026-2032年全球預測

脫水泵浦市場:按泵浦類型、技術、驅動系統、設計、額定功率、材質和最終用途產業分類-2026-2032年全球預測 排水泵市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、最終用途產業、泵浦類型、地區和競爭格局分類,2021-2031年)全球建築幫浦市場(按泵浦類型、動力來源、運作方式、最終用途產業和銷售管道分類)預測(2026-2032年)

排水泵市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、最終用途產業、泵浦類型、地區和競爭格局分類,2021-2031年)全球建築幫浦市場(按泵浦類型、動力來源、運作方式、最終用途產業和銷售管道分類)預測(2026-2032年) 建築幫浦市場規模、佔有率和成長分析(按產品類型、功率、容量、分銷管道和地區分類)-2026-2033年產業預測

建築幫浦市場規模、佔有率和成長分析(按產品類型、功率、容量、分銷管道和地區分類)-2026-2033年產業預測 全球排水泵市場全球採礦幫浦市場

全球排水泵市場全球採礦幫浦市場