|

市場調查報告書

商品編碼

2045826

工業氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測Industrial Hydrogen Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

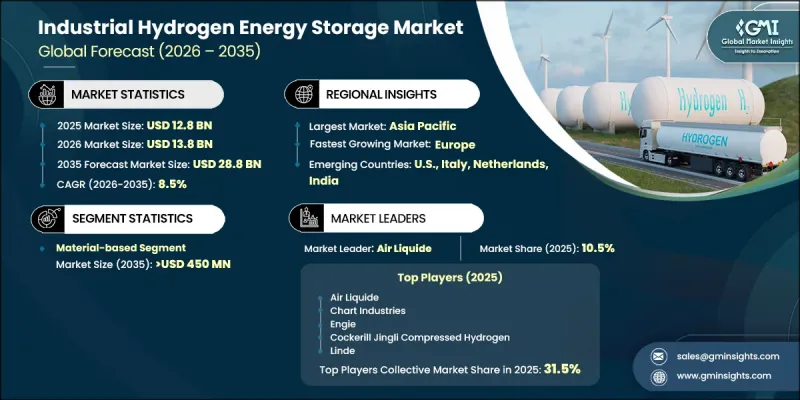

預計到 2025 年,全球工業氫能儲存市場規模將達到 128 億美元,並預計以 8.5% 的複合年成長率成長,到 2035 年達到 288 億美元。

工業氫能儲存產業的成長得益於全球加速向脫碳轉型以及對高效可再生能源併網解決方案日益成長的需求。氫能作為一種清潔、柔軟性的能源載體,正日益受到認可,有助於在發電、製造、交通和重工業等領域排放減排。可再生能源的廣泛應用也推動了對能夠適應間歇性電力供應的長期儲能系統的需求。包括高壓儲能系統、低溫技術和固體技術在內的儲能技術不斷進步,提高了儲能系統的效率、安全性和可擴展性。對氫氣生產設施、儲能獎勵和分銷網路的投資增加,進一步促進了市場發展。各國政府和相關人員正透過資金舉措、政策激勵和大規模基礎設施項目積極支持氫能經濟框架。此外,將儲能與太陽能和風能系統結合,能夠增強電網穩定性和能源可靠性,使氫能成為未來全球工業領域清潔能源系統的關鍵驅動力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 128億美元 |

| 預測市場規模 | 288億美元 |

| 複合年成長率 | 8.5% |

預計2035年,材料基氫儲存領域市場規模將達4.5億美元。氫儲存材料的持續創新是該領域成長的主要驅動力,例如金屬氫化物、化學氫化物和複雜氫化物體係等先進化合物的開發。這些材料因其能夠提高儲存密度、穩定性和整體系統效率而備受關注。材料科學的進步正在提升氫的吸附和釋放能力,使儲存系統更加可靠,並使其在大規模工業應用中更具商業性可行性。持續的研發工作正在進一步提高氫儲存技術的成本效益和運作安全性。

預計到2035年,美國工業氫能儲存市場規模將達42億美元。美國市場的擴張得益於強大的聯邦政策框架、對清潔能源投資的增加以及對永續工業能源解決方案日益成長的需求。美國《清潔能源法案》下的獎勵計畫正在加速氫氣生產和儲存基礎設施的建設。煉油、化學和冶金等大型工業部門的存在進一步推動了對高效氫氣儲存系統的需求。此外,可再生能源裝置容量的快速成長也增加了對長期儲能技術的需求,以確保電網穩定。公私合營以及大規模氫能樞紐計畫正在進一步促進氫能技術在全國範圍內的普及,使美國成為一個重要的成長市場。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 生產能力和生產情況

- 主要製造商的生產能力

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場(核心解決方案)的影響

- 人工智慧驅動的生產最佳化(核心解決方案)

- 預測性維護和故障檢測(核心解決方案)

- 新機會與趨勢

- 投資分析及未來展望

- 永續發展措施與工業4.0的融合

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 重要夥伴關係和聯盟

- 主要併購活動

- 產品創新和新產品發布

- 市場擴大策略

- 競爭定位矩陣

第5章 市場規模及預測:依方法論分類,2022-2035年

- 壓縮

- 液化

- 基於材料的

第6章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 其他

第7章:公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Chart Industries

- Cockerill Jingli Compressed hydrogen

- ENGIE

- Everfuel A/S

- FuelCell Energy, Inc.

- GKN Compressed Hydrogen

- Gravitricity Ltd

- Hexagon Purus ASA

- ITM Power PLC

- Linde plc

- McPhy Energy SA

- Nel ASA

- NPROXX BV

- Plug Power Inc.

- SSE

- Worthington Industries

The Global Industrial Hydrogen Energy Storage Market was valued at USD 12.8 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 28.8 billion by 2035.

Growth in the industrial hydrogen energy storage industry is driven by the accelerating global shift toward decarbonization and the rising need for efficient renewable energy integration solutions. Hydrogen is increasingly being recognized as a clean and flexible energy carrier that supports emissions reduction across power generation, manufacturing, transportation, and heavy industry applications. Expanding renewable energy penetration is also increasing demand for long-duration storage systems capable of balancing intermittent power supply. Technological advancements in hydrogen storage, including high-pressure containment systems, cryogenic technologies, and solid-state storage innovations, are improving efficiency, safety, and scalability. Rising investments in hydrogen production facilities, storage infrastructure, and distribution networks are further strengthening market development. Governments and private stakeholders are actively supporting hydrogen economy frameworks through funding initiatives, policy incentives, and large-scale infrastructure projects. Integration of hydrogen storage with solar and wind energy systems is also enhancing grid stability and energy reliability, positioning hydrogen as a key enabler of future clean energy systems across global industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.8 Billion |

| Forecast Value | $28.8 Billion |

| CAGR | 8.5% |

The material-based segment is expected to reach USD 450 million by 2035. Continuous innovation in hydrogen storage materials is significantly contributing to this segment's expansion, with growing development of advanced compounds such as metal hydrides, chemical hydrides, and complex hydride systems. These materials are gaining attention due to their high storage density, stability, and ability to improve overall system efficiency. Advancements in material science are enhancing hydrogen absorption and release performance, making storage systems more reliable and commercially viable for large-scale industrial applications. Ongoing research and development efforts are further improving cost efficiency and operational safety in hydrogen storage technologies.

U.S. Industrial Hydrogen Energy Storage Market is projected to reach USD 4.2 billion by 2035. Market expansion in the United States is supported by strong federal policy frameworks, rising clean energy investments, and growing demand for sustainable industrial energy solutions. Incentive programs under national clean energy legislation are accelerating the development of hydrogen production and storage infrastructure. The presence of large-scale industrial sectors such as refining, chemicals, and metallurgy is further driving demand for efficient hydrogen storage systems. In addition, the rapid expansion of renewable energy capacity is increasing the need for long-duration storage technologies to ensure grid stability. Public-private collaborations and large-scale hydrogen hub initiatives are further strengthening deployment across the country, positioning the U.S. as a leading growth market.

Key companies operating in the Global Industrial Hydrogen Energy Storage Market include Air Liquide, Linde plc, Air Products and Chemicals, Inc., ENGIE, Plug Power Inc., Nel ASA, ITM Power PLC, McPhy Energy S.A., Chart Industries, Worthington Industries, Hexagon Purus ASA, FuelCell Energy, Inc., Everfuel A/S, NPROXX B.V., Cockerill Jingli Compressed Hydrogen, GKN Compressed Hydrogen, SSE, and Gravitricity Ltd. Companies operating in the industrial hydrogen energy storage market are adopting multiple strategies to strengthen their competitive position and expand global reach. Leading players are heavily investing in research and development to improve hydrogen storage efficiency, safety, and scalability across industrial applications. Strategic partnerships with energy utilities, industrial manufacturers, and renewable energy developers are enabling companies to accelerate project deployment and expand infrastructure networks. Firms are also focusing on large-scale hydrogen hub developments and integrated storage solutions linked with wind and solar energy systems. Expansion of manufacturing capacity and localization of supply chains are helping reduce production costs and improve accessibility. In addition, companies are actively engaging in government-backed clean energy programs and policy-driven initiatives to secure long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Method trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Capacity & production landscape (Driven by Primary Research)

- 3.7.1 Capacity by key producer (Driven by Primary Research)

- 3.7.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.8 Impact of AI & Generative AI on the market (Core Solution)

- 3.8.1 AI-Driven production optimization (Core Solution)

- 3.8.2 Predictive maintenance & fault detection (Core Solution)

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future prospects

- 3.11 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Method, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Compression

- 5.3 Liquefaction

- 5.4 Material based

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products and Chemicals, Inc.

- 7.3 Chart Industries

- 7.4 Cockerill Jingli Compressed hydrogen

- 7.5 ENGIE

- 7.6 Everfuel A/S

- 7.7 FuelCell Energy, Inc.

- 7.8 GKN Compressed Hydrogen

- 7.9 Gravitricity Ltd

- 7.10 Hexagon Purus ASA

- 7.11 ITM Power PLC

- 7.12 Linde plc

- 7.13 McPhy Energy S.A.

- 7.14 Nel ASA

- 7.15 NPROXX B.V.

- 7.16 Plug Power Inc.

- 7.17 SSE

- 7.18 Worthington Industries

氫能儲存市場:2026-2032年全球市場預測(按儲存技術、物理狀態、壓力等級、儲存週期、儲存基礎設施類型和最終用途分類)

氫能儲存市場:2026-2032年全球市場預測(按儲存技術、物理狀態、壓力等級、儲存週期、儲存基礎設施類型和最終用途分類) 氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測。

氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測。 氫能儲存市場:市場規模、佔有率和趨勢分析(按技術、物理狀態、應用和地區分類),細分市場預測(2026-2033 年)固定式氫能儲存市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

氫能儲存市場:市場規模、佔有率和趨勢分析(按技術、物理狀態、應用和地區分類),細分市場預測(2026-2033 年)固定式氫能儲存市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 氫能儲存市場規模、佔有率、趨勢和預測:按產品類型、技術、應用、最終用戶和地區分類,2026-2034年

氫能儲存市場規模、佔有率、趨勢和預測:按產品類型、技術、應用、最終用戶和地區分類,2026-2034年 氫能儲存市場:按技術、應用和地區分類

氫能儲存市場:按技術、應用和地區分類 固定式氫燃料電池:全球市場展望、詳細分析及至2032年預測

固定式氫燃料電池:全球市場展望、詳細分析及至2032年預測 全球能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)車載氨分解系統市場:依車輛類型、推進方式、功率、催化劑、整合方式、應用領域、最終用戶分類,全球預測,2026-2032年分散式氨裂解系統市場按技術、原料類型、產能範圍、加熱方式、催化劑類型、應用和最終用途產業分類-全球預測,2026-2032年

全球能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)車載氨分解系統市場:依車輛類型、推進方式、功率、催化劑、整合方式、應用領域、最終用戶分類,全球預測,2026-2032年分散式氨裂解系統市場按技術、原料類型、產能範圍、加熱方式、催化劑類型、應用和最終用途產業分類-全球預測,2026-2032年