|

市場調查報告書

商品編碼

2045729

固定式氫能儲存市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Stationary Hydrogen Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

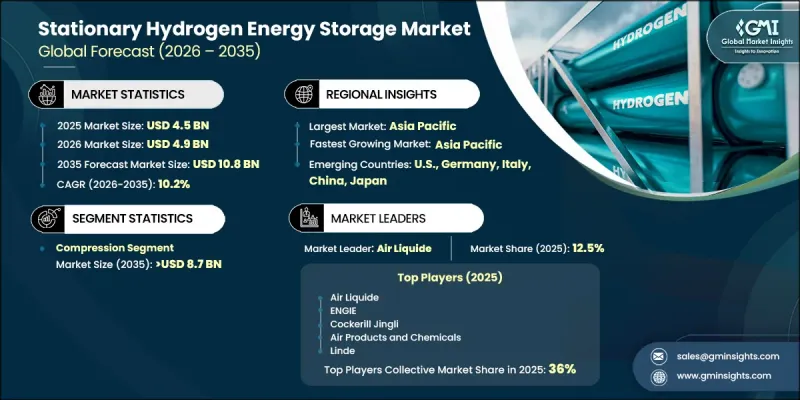

預計到 2025 年,全球固定式氫能儲存市場規模將達到 45 億美元,並有望以 10.2% 的複合年成長率成長,到 2035 年達到 108 億美元。

隨著氫能逐漸成為能源系統中長期儲能和電網穩定的關鍵組成部分,市場發展勢頭強勁。包括固體和液態儲能系統在內的儲氫技術的不斷進步,在提高效率的同時降低了全生命週期成本。這些創新增強了氫能儲能解決方案的經濟可行性,並拓展了其在大規模能源基礎設施中的部署潛力。全球向脫碳轉型以及對再生能源來源日益成長的依賴,進一步加速了對能夠應對間歇性發電的可靠儲能系統的需求。氫能透過確保穩定的能源供應和增強系統韌性,在將風能和太陽能等波動性可再生能源整合到現代電網中發揮著至關重要的作用。公共和私營部門不斷增加的投資正在支持氫氣生產、儲存和分配基礎設施的擴張。各國政府正透過財政獎勵、政策框架和監管支持來加強市場發展,旨在加速氫能的普及應用。同時,可再生能源裝置容量的擴張也進一步催生了對可擴展、高效能儲能技術的需求。這些因素共同作用,使得固定式氫能儲存成為未來世界各地能源轉型策略的關鍵組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 45億美元 |

| 預計金額 | 108億美元 |

| 複合年成長率 | 10.2% |

預計到2035年,壓縮儲氫市場規模將達87億美元。隨著氫能作為能源載體的日益普及,對高效能、可擴展儲氫解決方案的需求不斷成長,而壓縮技術在實現實用化中發揮核心作用。系統效率、安全性和能耗的持續提升正在推動該領域的擴張。設計工程和材料科學的進步正引領著更具成本效益和可靠性的壓縮系統的開發。此外,與其他儲氫方法相比,壓縮儲氫技術操作簡單、技術成熟,這使其在廣泛的應用領域中更具商業性吸引力。

預計到2025年,美國固定式氫能儲存市場將佔據77%的市場佔有率,市場規模將達到7.802億美元。美國市場成長的驅動力包括強大的脫碳目標、持續的電網基礎設施現代化以及再生能源來源的日益普及。聯邦政府支持清潔氫氣生產的扶持計劃,以及對電解槽部署和長期能源儲存系統的獎勵,正在推動大規模投資。電力公司正在擴大氫能儲存技術的應用,以提高電網可靠性、應對可再生能源波動並取代傳統的石化燃料尖峰電力解決方案。氫能樞紐的建設、國防相關微電網應用以及關鍵基礎設施的備用電源系統,進一步刺激了市場需求。先進技術供應商的存在、強大的研發能力以及各州清潔能源扶持政策,持續鞏固美國在該領域的領先地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和生產情況

- 主要製造商的生產能力

- 運轉率和擴張計劃

- 新機會和趨勢

- 投資分析及未來展望

- 永續發展措施與工業4.0的融合

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 重要夥伴關係和聯盟

- 主要併購趨勢

- 產品創新和新產品發布

- 市場擴大策略

- 競爭定位矩陣

第5章 市場規模及預測:依方法論分類,2022-2035年

- 壓縮

- 液化

- 基於材料的

第6章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 其他

第7章:公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Cockerill Jingli Compressed hydrogen

- ENGIE

- FuelCell Energy, Inc.

- GKN Compressed Hydrogen

- Gravitricity Ltd

- ITM Power PLC

- Linde plc

- McPhy Energy SA

- Nel ASA

- SSE

The Global Stationary Hydrogen Energy Storage Market was valued at USD 4.5 billion in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 10.8 billion by 2035.

The market is gaining traction as hydrogen emerges as a key enabler of long-duration energy storage and grid stability in evolving energy systems. Ongoing advancements in hydrogen storage technologies, including solid-state and liquid-based systems, are improving efficiency while reducing overall lifecycle costs. These innovations are strengthening the economic viability of hydrogen-based storage solutions and expanding their deployment potential across large-scale energy infrastructure. The global shift toward decarbonization and increasing reliance on renewable energy sources is further accelerating demand for reliable storage systems that can balance intermittent power generation. Hydrogen plays a crucial role in integrating variable renewable energy such as wind and solar into modern grids by ensuring consistent energy supply and enhancing system resilience. Rising investments from both public and private sectors are supporting the expansion of hydrogen production, storage, and distribution infrastructure. Governments are reinforcing market development through financial incentives, policy frameworks, and regulatory support aimed at accelerating hydrogen adoption. At the same time, the growing deployment of renewable energy capacity is creating additional pressure for scalable and efficient storage technologies. Collectively, these factors are positioning stationary hydrogen energy storage as a critical component of future energy transition strategies worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.5 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 10.2% |

The compression segment is anticipated to reach USD 8.7 billion by 2035. Increasing adoption of hydrogen as an energy carrier has intensified the need for efficient and scalable storage solutions, with compression technology playing a central role in enabling practical applications. Continuous improvements in system efficiency, safety performance, and energy consumption are driving segment expansion. Advances in engineering design and material science are contributing to the development of more cost-effective and reliable compression systems. The segment is also benefiting from its operational simplicity and established technological maturity compared to alternative hydrogen storage approaches, which enhances its commercial attractiveness across multiple applications.

U.S. Stationary Hydrogen Energy Storage Market accounted for 77% share in 2025, generating USD 780.2 million. Growth in the country is driven by strong decarbonization targets, ongoing modernization of grid infrastructure, and increasing integration of renewable energy sources. Federal support programs promoting clean hydrogen production, along with incentives for electrolyzer deployment and long-duration energy storage systems, are encouraging large-scale investments. Utilities are increasingly adopting hydrogen-based storage to improve grid reliability, manage renewable energy fluctuations, and replace conventional fossil-fuel-based peaking power solutions. Expanding hydrogen hub development, defense-related microgrid applications, and backup power systems for critical infrastructure are further strengthening market demand. The presence of advanced technology providers, strong research and development capabilities, and supportive state-level clean energy policies continues to reinforce the country's leadership in this sector.

Major players operating in the Global Stationary Hydrogen Energy Storage Industry include SSE, FuelCell Energy, Inc., ENGIE, ITM Power PLC, McPhy Energy S.A., Linde plc, Air Liquide, Nel ASA, Air Products and Chemicals, Inc., Cockerill Jingli Compressed Hydrogen, GKN Hydrogen, and Gravitricity Ltd. Companies in the stationary hydrogen energy storage market are actively focusing on technological advancement to enhance storage efficiency, reduce costs, and improve system scalability. Many players are investing heavily in research and development to advance compression, liquefaction, and solid-state storage technologies. Strategic collaborations with energy utilities, industrial users, and government bodies are helping expand large-scale deployment opportunities. Firms are also strengthening their market position through investments in hydrogen infrastructure projects, including production and distribution networks. Expansion of manufacturing capacity and optimization of supply chains are enabling better cost control and improved project execution timelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Method trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Trade data analysis (HS Code- 85042100) (Driven by Primary Research)

- 3.7.1 Import/export value trends (Driven by Primary Research)

- 3.7.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.8 Capacity & production landscape (Driven by Primary Research)

- 3.8.1 Capacity by key producer (Driven by Primary Research)

- 3.8.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future prospects

- 3.11 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Method, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Compression

- 5.3 Liquefaction

- 5.4 Material-based

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products and Chemicals, Inc.

- 7.3 Cockerill Jingli Compressed hydrogen

- 7.4 ENGIE

- 7.5 FuelCell Energy, Inc.

- 7.6 GKN Compressed Hydrogen

- 7.7 Gravitricity Ltd

- 7.8 ITM Power PLC

- 7.9 Linde plc

- 7.10 McPhy Energy S.A.

- 7.11 Nel ASA

- 7.12 SSE

氫能儲存市場:2026-2032年全球市場預測(按儲存技術、物理狀態、壓力等級、儲存週期、儲存基礎設施類型和最終用途分類)

氫能儲存市場:2026-2032年全球市場預測(按儲存技術、物理狀態、壓力等級、儲存週期、儲存基礎設施類型和最終用途分類) 氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測。

氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測。 氫能儲存市場:市場規模、佔有率和趨勢分析(按技術、物理狀態、應用和地區分類),細分市場預測(2026-2033 年)工業氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測

氫能儲存市場:市場規模、佔有率和趨勢分析(按技術、物理狀態、應用和地區分類),細分市場預測(2026-2033 年)工業氫能儲存市場機會、成長要素、產業趨勢分析及2026-2035年預測 氫能儲存市場規模、佔有率、趨勢和預測:按產品類型、技術、應用、最終用戶和地區分類,2026-2034年

氫能儲存市場規模、佔有率、趨勢和預測:按產品類型、技術、應用、最終用戶和地區分類,2026-2034年 氫能儲存市場:按技術、應用和地區分類

氫能儲存市場:按技術、應用和地區分類 固定式氫燃料電池:全球市場展望、詳細分析及至2032年預測

固定式氫燃料電池:全球市場展望、詳細分析及至2032年預測 全球能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)車載氨分解系統市場:依車輛類型、推進方式、功率、催化劑、整合方式、應用領域、最終用戶分類,全球預測,2026-2032年分散式氨裂解系統市場按技術、原料類型、產能範圍、加熱方式、催化劑類型、應用和最終用途產業分類-全球預測,2026-2032年

全球能源儲存系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)車載氨分解系統市場:依車輛類型、推進方式、功率、催化劑、整合方式、應用領域、最終用戶分類,全球預測,2026-2032年分散式氨裂解系統市場按技術、原料類型、產能範圍、加熱方式、催化劑類型、應用和最終用途產業分類-全球預測,2026-2032年