|

市場調查報告書

商品編碼

2045807

翻新電腦及筆記型電腦:市場機會、成長要素、產業趨勢分析及2026-2035年預測Refurbished Computers and Laptop Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球翻新電腦和筆記型電腦市場預計到 2025 年價值 62 億美元,預計到 2035 年將以 6.3% 的複合年成長率成長至 122 億美元。

翻新電腦和筆記型電腦市場的成長主要得益於遠距辦公和混合辦公環境的快速發展,這使得人們對價格合理且可靠的數位設備的需求日益成長。隨著教育、就業和基本服務不斷向線上平台轉移,擁有功能齊全的電腦設備不再是可選項,而是必需品。新筆記型電腦和桌上型電腦價格的不斷上漲仍然是個人和小型企業購買的一大障礙,因此,性能可靠且價格更低的翻新產品需求旺盛。翻新產品在提高弱勢群體(尤其是在價格敏感地區)的數位接入方面也發揮著至關重要的作用。政府、教育機構和各類組織擴大分發翻新筆記型電腦和桌上型電腦,以支持人們的持續學習和就業。此外,日益增強的環保意識也促使消費者將翻新電子產品納入永續消費行為,進一步推動了全球各地市場的擴張。循環經濟原則的日益普及也增強了翻新電腦和筆記型電腦市場的長期需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 62億美元 |

| 預計金額 | 122億美元 |

| 複合年成長率 | 6.3% |

翻新電腦和筆記型電腦市場也呈現穩定成長態勢,這主要得益於各方為彌合數位落差所做的努力不斷加大,以及消費者對翻新技術解決方案的接受度日益提高。消費者在選擇計算設備時,越來越重視性價比、性能可靠性和永續性。翻新生態系統的擴展、品質保證流程的改進以及消費者對認證翻新產品信心的增強,進一步推動了翻新產品在已開發市場和新興市場的滲透率。

預計到2025年,筆記型電腦市場規模將達到44億美元。由於筆記型電腦的便攜性、靈活的使用方式以及能夠處理包括工作、學習和娛樂在內的各種應用,市場對翻新筆記型電腦的需求持續成長。筆記型電腦將處理器、顯示器和電池功能整合於一體,使其成為行動工作者、學生和企業用戶的理想選擇。處理器效能、電池效率和輕薄設計的不斷提升,進一步增強了筆記型電腦作為個人和企業首選運算解決方案的吸引力。

到2025年,A級翻新機將佔據52%的市場。 A級設備被認為是翻新機中最高品質的類別,不僅外觀優良,而且性能可靠。這些設備通常外觀和功能都接近全新,因為它們使用頻率低,在進入翻新流程之前幾乎沒有磨損徵兆。消費者之所以青睞A級翻新機,是因為它們在價格和品質保證之間取得了完美的平衡,對於注重成本、希望以較低價格獲得可靠計算解決方案的買家來說,A級翻新機是一個非常可靠的選擇。

美國翻新電腦和筆記型電腦市場佔據78.9%的市場佔有率,預計2025年市場規模將達到15億美元。在企業和消費者頻繁的技術升級週期推動下,美國已發展成為一個成熟且穩定的市場。企業更換設備類型和個人用戶提供的穩定翻新設備供應,支撐著美國強大的翻新生態系統。消費者對認證翻新專案的信心不斷增強,加上線上零售通路的普及,進一步提升了市場滲透率。此外,提供品質保證和實施標準化品質檢測,也進一步提高了美國消費者對翻新電腦設備的接受度。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 數位包容與遠距辦公

- 永續發展和循環經濟的發展趨勢

- 企業IT資產處分(ITAD)生態系統

- 產業潛在風險與挑戰

- 有限保固和售後服務

- 技術過時

- 機會

- OEM認證翻新計劃

- 再生技術和自動化方面的進步

- 促進因素

- 成長潛力分析

- 監理框架

- 電子廢棄物管理法規

- 資料隱私和安全標準(GDPR、CCPA)

- 有關維修權的法律規定

- 有關再生產品的消費者保護法

- 環境認證(EPEAT、能源之星)

- 價格分析

- 2022-2025年歷史價格趨勢分析

- 按業務類型分類的定價策略(OEM認證企業、第三方企業和平台型市場)

- 不同等級的價格差異

- 價格平價與新設備平均售價的比較

- 貿易數據分析(847130)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 跨境電商分銷趨勢

- 對區域貿易政策的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於細分市場的生成式人工智慧的應用案例和部署藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 以區域業態(現代零售與傳統零售)分類的通路覆蓋率

- 缺乏最後一公里基礎設施和不斷變化的管道

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 個人電腦

- 筆記型電腦

第6章 市場估算與預測:依等級分類,2022-2035年

- A級

- B級

- C級

- D級

第7章 市場估計與預測:依作業系統分類,2022-2035年

- 基於Windows系統的翻新電腦和筆記型電腦

- 翻新Mac電腦和筆記型電腦

- 其他

第8章 市場估價與預測:依螢幕尺寸分類,2022-2035年

- 11-13英寸

- 14-16英寸

- 17吋或更大

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 個人消費者

- 公司

- 其他

第10章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Apple

- Dell Technologies

- HP

- Lenovo Group

- Microsoft

- Razer

- MSI(Micro-Star International)

- 當地公司

- Acer

- Vaio

- Framework Computer

- System76

- Eluktronics

- Maingear

- Honor

- 新興企業

- Pine64

- Chuwi

- One Netbook(ONEXPLAYER)

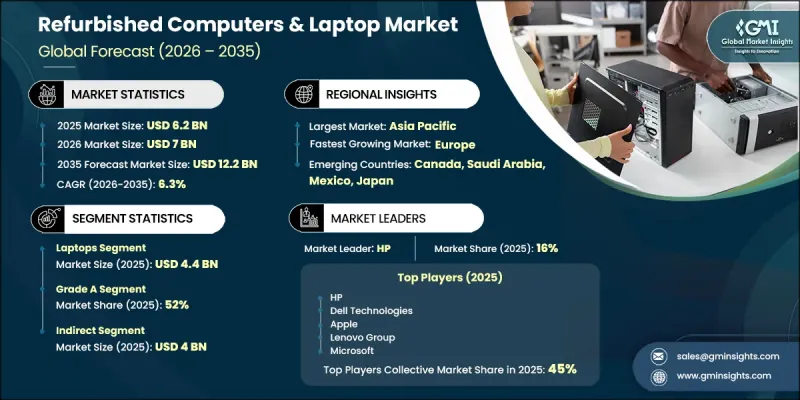

The Global Refurbished Computers & Laptop Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 12.2 billion by 2035.

Growth in the refurbished computing devices industry is supported by the rapid expansion of remote and hybrid work environments, which has increased reliance on affordable and reliable digital devices. As education, employment, and essential services continue shifting toward online platforms, access to functional computing devices has become a necessity rather than a discretionary purchase. High pricing of new laptops and computers continues to limit affordability for individuals and small businesses, creating strong demand for refurbished alternatives that offer reliable performance at lower costs. Refurbished devices are also playing a crucial role in improving digital accessibility for underserved populations, particularly in price-sensitive regions. Governments, educational institutions, and organizations are increasingly distributing refurbished laptops and computers to support learning continuity and workforce participation. In addition, growing environmental awareness is encouraging consumers to adopt refurbished electronics as part of sustainable purchasing behavior, further supporting market expansion across global regions. The increasing integration of circular economy principles is also reinforcing long-term demand within the refurbished computers and laptops market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 6.3% |

The Refurbished Computers & Laptop Market is also witnessing steady growth due to rising digital inclusion initiatives and increasing acceptance of pre-owned technology solutions. Consumers are increasingly prioritizing cost efficiency, performance reliability, and sustainability when selecting computing devices. Expanding refurbishment ecosystems, improved quality assurance processes, and growing trust in certified pre-owned products are further strengthening market adoption across both developed and emerging economies.

The laptops segment generated USD 4.4 billion in 2025. Demand for refurbished laptops continues to grow due to their portability, flexible usage, and ability to support a wide range of applications, including work, education, and entertainment. Their integrated design, combining processing power, display, and battery functionality in a single device, makes them highly suitable for mobile professionals, students, and businesses. Continuous improvements in processing performance, battery efficiency, and lightweight design are further enhancing the appeal of laptops as the preferred computing solution in both personal and professional environments.

The Grade A segment held a 52% share in 2025. Grade A devices are considered the highest-quality refurbished category, offering strong performance reliability along with excellent physical condition. These devices are typically lightly used before entering the refurbishment cycle and exhibit minimal signs of wear, making them visually and functionally close to new products. Consumers prefer Grade A refurbished devices because they provide a strong balance between affordability and quality assurance, making them a highly trusted option for cost-conscious buyers seeking dependable computing solutions without paying full retail prices.

U.S. Refurbished Computers & Laptop Market held a 78.9% share, generating USD 1.5 billion in 2025. The country represents a mature and well-established market driven by frequent technology replacement cycles across enterprises and consumers. A steady supply of pre-owned devices from corporate upgrades and individual users supports a strong refurbishment ecosystem. Growing consumer confidence in certified refurbishment programs, combined with expanded availability through online retail channels, continues to strengthen market penetration. The presence of warranty-backed offerings and standardized quality checks has further increased acceptance of refurbished computing devices across the United States.

Major companies operating in the Global Refurbished Computers & Laptop Industry include Apple, Dell Technologies, HP Inc., Lenovo Group, Microsoft, Razer, and MSI. Regional players include Acer, VAIO, Framework Computer, System76, Eluktronics, Maingear, and HONOR. Emerging participants include Pine64, Chuwi, and One Netbook. Companies operating in the Refurbished Computers & Laptop Industry are adopting several strategic initiatives to strengthen their competitive positioning and expand market reach. Manufacturers and refurbishment specialists are focusing on enhancing quality assurance processes, including rigorous testing, certification, and grading systems to build stronger consumer trust. Businesses are also investing in advanced refurbishment technologies to improve product reliability, performance, and lifespan. Expansion of online sales channels and direct-to-consumer platforms is helping companies reach a broader customer base while improving pricing transparency. Strategic partnerships with educational institutions, government programs, and corporate IT asset disposition services are also supporting steady supply and demand growth. In addition, companies are emphasizing sustainability-driven branding, warranty-backed offerings, and extended after-sales services to increase customer confidence and retention. Geographic expansion and circular economy integration are further strengthening long-term market positioning in the global refurbished computing devices industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Grade

- 2.2.4 Operating system

- 2.2.5 Screen size

- 2.2.6 End use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Digital inclusion & remote work

- 3.2.1.2 Sustainability & circular economy trends

- 3.2.1.3 Enterprise IT asset disposition (ITAD) ecosystem

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Limited warranty & after-sales support

- 3.2.2.2 Technological obsolescence

- 3.2.3 Opportunities

- 3.2.3.1 Certified refurbishment programs by OEMs

- 3.2.3.2 Advancements in refurbishment technology and automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 E-waste management regulations

- 3.4.2 Data privacy & security standards (GDPR, CCPA)

- 3.4.3 Right to repair legislation

- 3.4.4 Consumer protection laws for refurbished goods

- 3.4.5 Environmental certifications (EPEAT, Energy Star)

- 3.5 Pricing analysis

- 3.5.1 Historical price trend analysis (2022-2025)

- 3.5.2 Pricing strategy by player type (OEM-certified vs third-party vs platform marketplaces)

- 3.5.3 Grade-based price differentials

- 3.5.4 Price parity vs new device ASPs

- 3.6 Trade data analysis (driven by paid data base) (847130)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.6.3 Cross-border e-commerce flows

- 3.6.4 Regional trade policy implications

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 AI-driven disruption of existing business models

- 3.7.2 GenAI use cases & adoption roadmap by segment

- 3.7.3 Risks, limitations & regulatory considerations

- 3.8 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.8.1 Channel coverage by region & format (modern vs. Traditional trade)

- 3.8.2 Last-mile infrastructure gaps & emerging channel shifts

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Computers

- 5.3 Laptops

Chapter 6 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Grade A

- 6.3 Grade B

- 6.4 Grade C

- 6.5 Grade D

Chapter 7 Market Estimates and Forecast, By Operating System, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Windows refurbished computers & laptops

- 7.3 Mac refurbished computers & laptops

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Screen Size, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 11-13 inches

- 8.3 14-16 inches

- 8.4 17 inches and above

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Individual consumers

- 9.3 Businesses

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Apple

- 12.1.2 Dell Technologies

- 12.1.3 HP

- 12.1.4 Lenovo Group

- 12.1.5 Microsoft

- 12.1.6 Razer

- 12.1.7 MSI (Micro-Star International)

- 12.2 Regional players

- 12.2.1 Acer

- 12.2.2 Vaio

- 12.2.3 Framework Computer

- 12.2.4 System76

- 12.2.5 Eluktronics

- 12.2.6 Maingear

- 12.2.7 Honor

- 12.3 Emerging players

- 12.3.1 Pine64

- 12.3.2 Chuwi

- 12.3.3 One Netbook (ONEXPLAYER)