|

市場調查報告書

商品編碼

2045795

2026 年至 2035 年施工機械融資市場的商業機會、成長要素、產業趨勢與預測。Construction Equipment Finance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

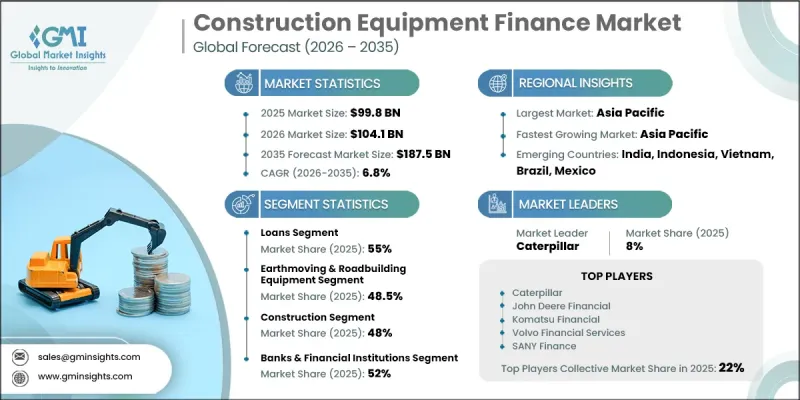

全球施工機械融資市場預計到 2025 年將達到 998 億美元,預計到 2035 年將以 6.8% 的複合年成長率成長至 1875 億美元。

已開發經濟體和新興經濟體對交通基礎設施、能源項目、住宅開發和大規模建設活動的投資增加,推動了市場成長。隨著資本密集型建設專案對資金籌措解決方案的依賴性日益增強,承包商和專案開發商正在採用能夠提供更大財務柔軟性和流動性的施工機械融資模式。建築公司擴大資金籌措解決方案來獲取挖土機、起重機、裝載機和重型設備等先進機械,而無需大量前期投資。貸款和租賃協議等資金籌措選擇使建築公司能夠更有效率地更新設備,同時支援專案的同步推進。建築收入的週期性和錯峰付款週期也促使企業更重視最佳化營運資本管理。資金籌措解決方案使企業能夠將設備成本分攤到長期,從而緩解短期財務壓力並提高業務永續營運。全球基礎設施開發舉措的擴展和建設活動的活性化,持續增強了多個行業對施工機械融資服務的長期需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 998億美元 |

| 預計金額 | 1875億美元 |

| 複合年成長率 | 6.8% |

貸款業務佔市場佔有率的55%,預計2026年至2035年將以6.4%的複合年成長率成長。對於大型建築公司和參與由機構投資者和政府支持計畫資助的大規模基礎設施項目的機構而言,貸款資金籌措仍然是普遍的首選。基礎設施擴建投資的增加推動了對用於支持重型設備採購的結構性定期貸款的強勁需求。此外,不斷變化的利率環境促使借款人尋求能夠提供更大還款柔軟性和更佳現金流管理的混合資金籌措結構。

預計到2025年,土方工程和道路施工設備市場佔有率將達到48.5%,並在2035年之前以5.5%的複合年成長率成長。挖土機、裝載機、推土機和平平土機等設備廣泛應用於基礎建設、城市建設和採礦等多個領域,因此資金籌措需求強勁。這些設備的高昂購置成本和較短的使用壽命是承包商和建設公司在購買或更換設備時選擇融資方案的主要原因。

美國施工機械融資市場預計到2025年將達到209億美元,並預計在2026年至2035年間以7.1%的複合年成長率穩定成長。美國擁有高度發展的施工機械融資生態系統,這得益於金融機構、製造商和產業協會之間的緊密合作。基礎設施現代化項目的增加和建設活動的擴張推動了全國金融交易量的成長。此外,數位化貸款平台簡化了承包商和小型企業的信用評估流程,使他們能夠更快、更方便地獲得施工機械融資解決方案。

目錄

第1章:調查方法

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 快速的基礎設施建設和都市化

- 該設備的初始投資成本相對較高。

- 人們對現金流最佳化的興趣日益濃厚

- 拓展靈活的資金籌措模式

- 產業潛在風險與挑戰

- 高昂的初始投資成本

- 維護和營運的複雜性

- 市場機遇

- 設備即服務 (EaaS) 的成長

- 拓展新興市場(亞太地區、非洲)

- 數位和金融科技解決方案的整合

- 永續綠色金融

- 促進因素

- 成長潛力分析

- 技術與創新展望

- 最新科技趨勢

- 新技術

- 價格分析

- 對過去價格趨勢的分析

- 根據參與企業的類型(高階、價值、成本加成)所製定的定價策略

- 監理情勢

- 北美洲

- 美國聯邦儲備系統(Fed)/貨幣監理署/消費者金融保護局

- 加拿大金融機構監理局(OSFI)

- 歐洲

- 歐盟委員會 - 金融穩定與安全管理總司

- 歐洲銀行管理局(EBA)

- 亞太地區

- 中國銀行保險監督管理委員會(銀保監會)/中國人民銀行(人民銀行)

- 印度儲備銀行(RBI)

- 拉丁美洲

- 巴西中央銀行(BCB)

- 墨西哥銀行證券委員會(CNBV)

- 中東和非洲

- 沙烏地阿拉伯中央銀行 (SAMA)

- 南非儲備銀行(SARB)/金融部門行為監理局(FSCA)

- 北美洲

- 波特的分析

- PESTLE分析

- 成本細分分析

- 專利分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於細分市場的生成式人工智慧的應用案例和部署藍圖

- 風險、限制和監管考量

- 永續性和環境方面

- 永續發展計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮碳足跡

- 預測假設和情境分析

- 基本案例:驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境:宏觀經濟與產業的利多因素

- 悲觀情景:宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依資金籌措方式分類,2022-2035年

- 貸款

- 租

- 融資租賃/資本租賃

- 經營租賃

- 抵押

第6章 市場估算與預測:依設備類型分類,2022-2035年

- 土木工程/道路施工設備

- 後鏟

- 液壓挖土機

- 裝載機

- 壓實設備

- 其他

- 物料輸送和起重機

- 儲存和運輸設備

- 工程系統

- 工業車輛

- 散裝物料輸送設備

- 混凝土設備

- 混凝土泵

- 破碎機

- 混凝土攪拌車

- 瀝青攤舖機

- 攪拌站

第7章 市場估計與預測:依產業區隔市場分類,2022-2035年

- 建造

- 礦業

- 林業和伐木

- 石油和天然氣

- 政府/公共工程

- 其他

第8章 市場估算與預測:依供應商分類,2022-2035年

- 銀行和金融機構

- 專屬式金融公司

- 獨立金融機構

- 金融科技公司和另類貸款機構

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 越南

- 印尼

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Bank of America Equipment Finance

- BNP Paribas Leasing Solutions

- Caterpillar Financial Services

- CNH Industrial Capital

- JP Morgan Equipment Finance

- John Deere Financial

- Komatsu Financial

- Liebherr Financial Services

- Volvo Financial Services

- Wells Fargo Equipment Finance

- 當地公司

- ANZ Equipment Finance

- BBVA Equipment Finance

- DBS Equipment Leasing

- JCB Finance

- Santander Equipment Finance

- TD Equipment Finance

- 新興企業

- Greensill Equipment Finance

- Sany Finance

- Stenn International

- XCMG Finance

The Global Construction Equipment Finance Market was valued at USD 99.8 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 187.5 billion by 2035.

Market growth is driven by rising investments in transportation infrastructure, energy projects, housing development, and large-scale construction activities across both developed and emerging economies. Increasing reliance on financing solutions for capital-intensive construction projects is encouraging contractors and project developers to adopt equipment financing models that improve financial flexibility and preserve liquidity. Construction businesses are increasingly utilizing financing solutions to access advanced machinery such as excavators, cranes, loaders, and heavy-duty equipment without requiring substantial upfront capital expenditure. Financing options, including loans and leasing arrangements, are enabling contractors to modernize fleets more efficiently while supporting simultaneous project execution. The cyclical nature of construction revenues and delayed payment cycles are also encouraging companies to focus on optimized working capital management. Financing solutions allow businesses to distribute equipment costs over extended periods, reducing immediate financial pressure and improving operational continuity. Growing infrastructure development initiatives and expanding construction activity worldwide continue to strengthen long-term demand for construction equipment financing services across multiple industry sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $99.8 Billion |

| Forecast Value | $187.5 Billion |

| CAGR | 6.8% |

The loans segment held a 55% share and is expected to grow at a CAGR of 6.4% from 2026 to 2035. Loan-based financing remains widely preferred among large contractors and organizations involved in major infrastructure projects supported by institutional or government-backed funding programs. Increasing investment in infrastructure expansion is contributing to strong demand for structured term loans designed to support heavy equipment acquisition. In addition, changing interest rate environments are encouraging borrowers to seek hybrid financing structures that provide greater repayment flexibility and improved cash flow management.

The earthmoving and roadbuilding equipment segment held a 48.5% share in 2025 and is projected to grow at a CAGR of 5.5% through 2035. Equipment categories such as excavators, loaders, bulldozers, and graders continue to witness strong financing demand due to their widespread application across infrastructure development, urban construction, and mining operations. High equipment acquisition costs and intensive usage cycles are major factors encouraging contractors and construction firms to utilize financing solutions when purchasing or upgrading machinery fleets.

U.S. Construction Equipment Finance Market generated USD 20.9 billion in 2025 and is expected to witness robust growth at a CAGR of 7.1% during 2026-2035. The United States maintains a highly developed equipment financing ecosystem supported by strong collaboration between financial institutions, manufacturers, and industry associations. Increasing infrastructure modernization projects and expanding construction activity are contributing to higher financing volumes across the country. In addition, digital lending platforms are simplifying the approval process for contractors and small and medium-sized enterprises, enabling faster and more convenient access to equipment financing solutions.

Leading companies operating in the Global Construction Equipment Finance Market include Bank of America Equipment Finance, BNP Paribas Leasing Solutions, Caterpillar Financial Services, CNH Industrial Capital, J.P. Morgan Equipment Finance, John Deere Financial, Komatsu Financial, Liebherr Financial Services, Volvo Financial Services, and Wells Fargo Equipment Finance. Companies operating in the construction equipment finance market are implementing several strategic initiatives to strengthen their competitive position and expand market presence. Leading providers are focusing on flexible financing models, customized repayment plans, and hybrid loan structures that align with the evolving cash flow requirements of contractors and construction firms. Investments in digital lending technologies and automated approval systems are helping companies accelerate financing processes and improve customer experience. Strategic collaborations with construction equipment manufacturers and dealerships are also enabling finance providers to expand distribution networks and improve equipment accessibility. In addition, companies are strengthening risk management capabilities through advanced analytics and credit assessment technologies to support more efficient financing operations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Financing type

- 2.2.3 Equipment

- 2.2.4 Industry vertical

- 2.2.5 Provider

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid infrastructure development & urbanization

- 3.2.1.2 High capital cost of equipment

- 3.2.1.3 Growing preference for cash flow optimization

- 3.2.1.4 Expansion of flexible financing models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost

- 3.2.2.2 Maintenance and operational complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of Equipment-as-a-Service (EaaS)

- 3.2.3.2 Emerging market expansion (Asia-Pacific, Africa)

- 3.2.3.3 Integration of digital & fintech solutions

- 3.2.3.4 Sustainable & green financing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 Federal Reserve System (Fed) / OCC / CFPB

- 3.6.1.2 Office of the Superintendent of Financial Institutions (OSFI)

- 3.6.2 Europe

- 3.6.2.1 European Commission - DG FISMA

- 3.6.2.2 European Banking Authority (EBA)

- 3.6.3 Asia Pacific

- 3.6.3.1 China Banking and Insurance Regulatory Commission (CBIRC) / People's Bank of China (PBOC)

- 3.6.3.2 Reserve Bank of India (RBI)

- 3.6.4 Latin America

- 3.6.4.1 Banco Central do Brasil (BCB)

- 3.6.4.2 Comision Nacional Bancaria y de Valores (CNBV)

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Central Bank (SAMA)

- 3.6.5.2 South African Reserve Bank (SARB) / Financial Sector Conduct Authority (FSCA)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Financing Type, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Loans

- 5.3 Leases

- 5.3.1 Finance Leases/Capital Leases

- 5.3.2 Operating Leases

- 5.4 Mortgage

Chapter 6 Market Estimates & Forecast, By Equipment, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Earthmoving & roadbuilding equipment

- 6.2.1 Backhoe

- 6.2.2 Excavator

- 6.2.3 Loader

- 6.2.4 Compaction equipment

- 6.2.5 Others

- 6.3 Material handling and cranes

- 6.3.1 Storage and handling equipment

- 6.3.2 Engineered systems

- 6.3.3 Industrial trucks

- 6.3.4 Bulk material handling equipment

- 6.4 Concrete equipment

- 6.4.1 Concrete pumps

- 6.4.2 Crusher

- 6.4.3 Transit mixers

- 6.4.4 Asphalt pavers

- 6.4.5 Batching plants

Chapter 7 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Mining

- 7.4 Forestry & Logging

- 7.5 Oil & Gas

- 7.6 Government & Public Works

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Provider, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Banks & financial institutions

- 8.3 Captive finance companies

- 8.4 Independent lenders

- 8.5 Fintechs & alternative lenders

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Bank of America Equipment Finance

- 10.1.2 BNP Paribas Leasing Solutions

- 10.1.3 Caterpillar Financial Services

- 10.1.4 CNH Industrial Capital

- 10.1.5 J.P. Morgan Equipment Finance

- 10.1.6 John Deere Financial

- 10.1.7 Komatsu Financial

- 10.1.8 Liebherr Financial Services

- 10.1.9 Volvo Financial Services

- 10.1.10 Wells Fargo Equipment Finance

- 10.2 Regional players

- 10.2.1 ANZ Equipment Finance

- 10.2.2 BBVA Equipment Finance

- 10.2.3 DBS Equipment Leasing

- 10.2.4 JCB Finance

- 10.2.5 Santander Equipment Finance

- 10.2.6 TD Equipment Finance

- 10.3 Emerging players

- 10.3.1 Greensill Equipment Finance

- 10.3.2 Sany Finance

- 10.3.3 Stenn International

- 10.3.4 XCMG Finance