|

市場調查報告書

商品編碼

2045791

食品儲存容器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Food Storage Container Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

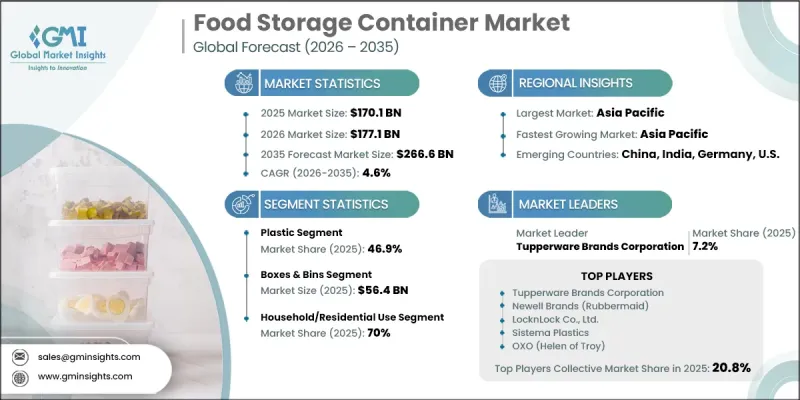

2025年全球食品儲存容器市場價值為1,701億美元,預計到2035年將以4.6%的複合年成長率成長至2,666億美元。

包裝食品、簡便食品和即食產品的消費量不斷成長,顯著推動了全球市場的擴張。隨著住宅和商業領域對高效食品保鮮解決方案的依賴日益增強,對耐用、高性能的儲物容器的需求也十分旺盛。人們對食品安全、衛生和減少廢棄物意識的提高也促進了市場的發展。消費者越來越傾向於選擇有助於延長保存期限和保持食品新鮮的高品質容器。此外,永續發展計劃和循環經濟政策鼓勵製造商開發可重複使用、可回收且環保的儲物解決方案。多功能食品容器的日益普及,滿足了儲存、加熱和盛放等多種用途,進一步推動了產業成長。產品設計、防漏技術、可堆疊形狀和微波爐適用材料的進步,也提升了消費者的使用便利性,並推動了全球家庭、餐廳和餐飲服務業對產品的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1701億美元 |

| 預計金額 | 2666億美元 |

| 複合年成長率 | 4.6% |

預計到2035年,玻璃器皿市場將以5.9%的複合年成長率成長,這主要得益於消費者對永續、無毒且防異味食品保鮮解決方案日益成長的偏好。玻璃容器因其更佳的耐用性、更優異的衛生性能以及適用於微波爐和烤箱等優點,深受追求經久耐用廚具的消費者青睞。消費者對環保、高品質儲物容器的需求不斷成長,並持續推動著玻璃器皿在住宅和商用廚房中的普及。

預計2026年至2035年間,罐裝食品市場將以5.8%的複合年成長率成長。隨著消費者越來越重視廚房空間的整潔有序和便捷的食品儲藏方案,對這類產品的需求也不斷成長。罐裝食品不僅能提升乾貨的可見度、易取性和儲存效率,還能提升現代廚房的美感。人們對家居收納和高階廚房配件日益成長的興趣也進一步推動了這一市場的成長。

預計到2025年,北美食品儲存容器市佔率將達到27.8% 。全部區域對包裝食品、冷凍食品和散裝食品的強勁需求持續推動市場擴張。成熟的零售網路、不斷變化的飲食習慣以及消費者對耐用、大容量儲存解決方案日益成長的偏好,都對產品滲透率產生了積極影響。可支配收入的增加以及消費者在家庭收納和廚房升級方面的支出增加,進一步推動了該地區對高階食品儲存容器的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 包裝食品和即食食品的消費量增加

- 來自餐飲服務業和商用廚房的需求不斷成長。

- 消費者對永續和可重複使用的儲存解決方案的需求日益成長

- 對先進的密封和保鮮功能有著強勁的需求。

- 由於市場對高耐用性和高品質材料的需求,優質化。

- 產業潛在風險與挑戰

- 與低成本、無組織的製造商展開激烈競爭。

- 對塑膠安全性和監管合規性的擔憂

- 市場機遇

- 推出智慧化的數位化食品保鮮生態系統。

- 新興國家的都市化和廚房基礎設施的進步推動了市場擴張。

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- R&D

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興企業競爭公司和新創企業的發展趨勢

第5章 市場估計與預測:依材料分類,2022-2035年

- 塑膠

- 聚丙烯(PP)

- 高密度聚苯乙烯(HDPE)

- 聚對苯二甲酸乙二醇酯(PET)

- 其他

- 玻璃

- 金屬

- 其他

- 矽酮

- 竹纖維

- 小麥秸稈複合材料

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 盒子和容器

- 瓶子和罐子

- 瓶子和罐子

- 袋子和小袋

- 其他

- 備餐

- 便當

- 便當

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 冷藏庫庫

- 攜帶式午餐盒

- 冷凍庫儲存

- 食品儲藏室

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 適用於家庭/住宅用途

- 商業用途

- 速食店(QSR)

- 飯店和住宿設施

- 雲廚房

- 咖啡館和咖啡店

- 其他

- 對機構而言

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 全球主要公司

- Tupperware Brands Corporation

- Newell Brands(Rubbermaid)

- LocknLock Co., Ltd.

- Sistema Plastics

- OXO(Helen of Troy)

- 該地區的主要公司

- 北美洲

- Amcor plc

- Anchor Hocking

- Berry Global Inc.

- Cambro

- Corelle Brands

- Novolex

- Sabert Corporation

- Sonoco Products Company

- 亞太地區

- Borosil Limited

- Decor Corporation Pty. Ltd.

- Glasslock USA, Inc.

- Hamilton Housewares Pvt. Ltd.

- Zojirushi

- Zishta

- 歐洲

- EMSA GmbH

- Mepal

- Brabantia Branding BV

- 北美洲

The Global Food Storage Container Market was valued at USD 170.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 266.6 billion by 2035.

Rising consumption of packaged meals, convenience foods, and ready-to-eat products is significantly contributing to market expansion worldwide. Increasing reliance on efficient food preservation solutions across residential and commercial sectors is creating strong demand for durable and high-performance storage containers. The market is also benefiting from growing awareness regarding food safety, hygiene, and waste reduction. Consumers are increasingly favoring premium-quality containers that help extend shelf life and maintain freshness. In addition, sustainability initiatives and circular economy policies are encouraging manufacturers to develop reusable, recyclable, and eco-conscious storage solutions. Growing adoption of multifunctional food containers that support storage, reheating, and serving applications is further strengthening industry growth. Advancements in product design, leak-proof technology, stackable formats, and microwave-safe materials are also improving consumer convenience and driving product demand across households, restaurants, and foodservice establishments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $170.1 Billion |

| Forecast Value | $266.6 Billion |

| CAGR | 4.6% |

The glass segment is anticipated to record a CAGR of 5.9% through 2035, supported by increasing consumer preference for sustainable, non-toxic, and odor-resistant food storage solutions. Glass-based containers provide enhanced durability, superior hygiene, and compatibility with microwave and oven applications, making them highly attractive among consumers seeking long-lasting kitchen products. Rising demand for environmentally friendly and premium storage materials continues to accelerate adoption across residential and commercial kitchens.

The jars and canisters segment is forecast to grow at a CAGR of 5.8% during 2026-2035. Demand for these products is increasing as consumers prioritize organized kitchen spaces and convenient pantry storage solutions. Jars and canisters improve visibility, accessibility, and storage efficiency for dry food items while complementing modern kitchen aesthetics. Growing interest in home organization and premium kitchen accessories is further contributing to segment growth.

North America Food Storage Container Market accounted for 27.8% share in 2025. Strong demand for packaged, frozen, and bulk food products across the region continues to support market expansion. The presence of established retail networks, changing eating habits, and increasing preference for durable and large-capacity storage solutions are positively influencing product adoption. Rising disposable income and growing consumer spending on home organization and kitchen upgrades are further driving regional demand for advanced food storage containers.

Key companies operating in the Global Food Storage Container Market include Amcor plc, Brabantia Branding B.V., Sistema Plastics, Sonoco Products Company, Novolex, LocknLock Co., Berry Global Inc., Sabert Corporation, OXO, EMSA GmbH, Zojirushi, Decor Corporation Pty. Ltd., Mepal, Tupperware, Borosil Limited, Anchor Hocking, Glasslock USA, Inc., Hamilton Housewares Pvt. Ltd., Corelle Brands, Rubbermaid Commercial Products, Cambro, and Zishta. Companies operating in the food storage container market are focusing on product innovation, sustainability initiatives, and expansion of premium product portfolios to strengthen their market position. Manufacturers are increasingly introducing reusable, BPA-free, recyclable, and microwave-safe containers to align with changing consumer preferences and environmental regulations. Many companies are investing in advanced material technologies to improve durability, leak resistance, and multifunctionality. Strategic collaborations with retail chains and e-commerce platforms are helping brands expand product accessibility and strengthen customer reach globally. Businesses are also emphasizing smart packaging designs, stackable storage formats, and aesthetically appealing products to improve customer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End-User trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumption of packaged and ready-to-eat food products

- 3.2.1.2 Growing demand from foodservice and commercial kitchen operations

- 3.2.1.3 Rising consumer shift toward sustainable and reusable storage solutions

- 3.2.1.4 Strong demand for advanced sealing and freshness-preserving features

- 3.2.1.5 Premiumization driven by demand for durable and high-quality materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High competition from low-cost and unorganized manufacturers

- 3.2.2.2 Concerns related to plastic safety and regulatory compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of smart and digitally enabled food storage ecosystems

- 3.2.3.2 Market expansion driven by urbanization and evolving kitchen infrastructure in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Plastic

- 5.2.1 Polypropylene (PP)

- 5.2.2 High-density polyethylene (HDPE)

- 5.2.3 Polyethylene terephthalate (PET)

- 5.2.4 Others

- 5.3 Glass

- 5.4 Metal

- 5.5 Others

- 5.5.1 Silicone

- 5.5.2 Bamboo fiber

- 5.5.3 Wheat straw composites

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Boxes & bins

- 6.3 Jars & canisters

- 6.4 Bottles & cans

- 6.5 Bags & pouches

- 6.6 Others

- 6.6.1 Meal prep

- 6.6.2 Lunch boxes

- 6.6.3 Bento boxes

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Refrigerator storage

- 7.3 On-the-go & lunch containers

- 7.4 Freezer storage

- 7.5 Pantry storage

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Household/residential use

- 8.3 Commercial use

- 8.3.1 Quick-service restaurants (QSR)

- 8.3.2 Hotels & lodging

- 8.3.3 Cloud kitchens

- 8.3.4 Cafes & coffee shops

- 8.3.5 Others

- 8.4 Institutional use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Tupperware Brands Corporation

- 10.1.2 Newell Brands (Rubbermaid)

- 10.1.3 LocknLock Co., Ltd.

- 10.1.4 Sistema Plastics

- 10.1.5 OXO (Helen of Troy)

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Amcor plc

- 10.2.1.2 Anchor Hocking

- 10.2.1.3 Berry Global Inc.

- 10.2.1.4 Cambro

- 10.2.1.5 Corelle Brands

- 10.2.1.6 Novolex

- 10.2.1.7 Sabert Corporation

- 10.2.1.8 Sonoco Products Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Borosil Limited

- 10.2.2.2 Decor Corporation Pty. Ltd.

- 10.2.2.3 Glasslock USA, Inc.

- 10.2.2.4 Hamilton Housewares Pvt. Ltd.

- 10.2.2.5 Zojirushi

- 10.2.2.6 Zishta

- 10.2.3 Europe

- 10.2.3.1 EMSA GmbH

- 10.2.3.2 Mepal

- 10.2.3.3 Brabantia Branding B.V.

- 10.2.1 North America

食品容器市場:2026-2032年全球市場預測(按材料、產品類型、應用、產業、最終用戶和分銷管道分類)

食品容器市場:2026-2032年全球市場預測(按材料、產品類型、應用、產業、最終用戶和分銷管道分類) 歐洲家居收納整理產品:市佔率分析、產業趨勢與統計及成長預測(2026-2031)

歐洲家居收納整理產品:市佔率分析、產業趨勢與統計及成長預測(2026-2031) 食品容器市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、材料、分銷管道、地區和競爭格局分類,2021-2031年

食品容器市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、材料、分銷管道、地區和競爭格局分類,2021-2031年 2026年全球散裝食品儲存產品市場報告家用食品儲存容器市場:2026-2032年全球市場預測(依產品類型、材質、容量、封蓋類型、最終用途及通路分類)陽台儲能市場:按電池技術、儲能容量、系統類型、充電方式、應用、最終用途和銷售管道分類-2026-2032年全球預測家用儲能分體器市場:按技術、電壓、相數、容量、最終用戶和應用分類,全球預測,2026-2032年

2026年全球散裝食品儲存產品市場報告家用食品儲存容器市場:2026-2032年全球市場預測(依產品類型、材質、容量、封蓋類型、最終用途及通路分類)陽台儲能市場:按電池技術、儲能容量、系統類型、充電方式、應用、最終用途和銷售管道分類-2026-2032年全球預測家用儲能分體器市場:按技術、電壓、相數、容量、最終用戶和應用分類,全球預測,2026-2032年 保溫食品容器市場:依產品類型、分銷通路和地區分類

保溫食品容器市場:依產品類型、分銷通路和地區分類 食品壓板市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、最終用戶、功能、製程及組件分類食品容器市場分析及預測(至2035年):類型、材質、產品類型、應用、技術、最終用戶、形狀、功能與組件

食品壓板市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、最終用戶、功能、製程及組件分類食品容器市場分析及預測(至2035年):類型、材質、產品類型、應用、技術、最終用戶、形狀、功能與組件