|

市場調查報告書

商品編碼

2045749

積木玩具市場機會、成長要素、產業趨勢分析及2026-2035年預測Building Blocks Toys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

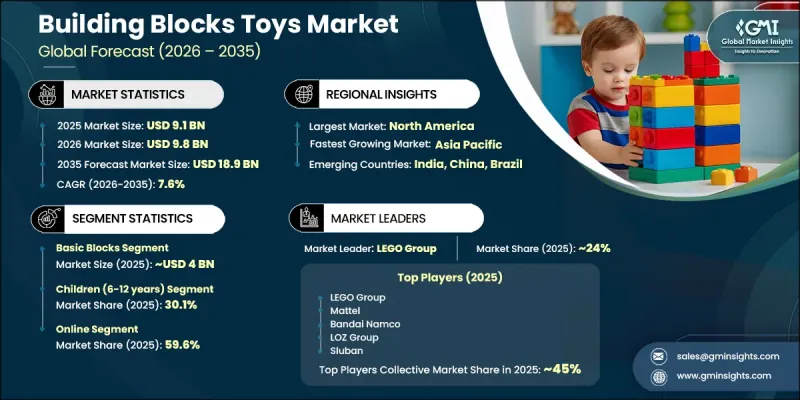

全球積木市場預計到 2025 年將價值 91 億美元,預計到 2035 年將以 7.6% 的複合年成長率成長至 189 億美元。

隨著人們對STEM教育的興趣日益濃厚,能夠促進問題解決能力、創造力和動手實踐的玩具越來越受歡迎。家長、教育工作者和政策制定者越來越強調早期培養基礎技能的重要性,這些技能有助於孩子的長期發展。這種轉變不僅源自於學術方面的考量,也源自於對兒童全面發展的更廣泛關注。消費者積極尋求兼具娛樂性和教育價值的產品,這反映出他們越來越偏好「寓教於樂」的遊戲方式。積木玩具透過促進認知、社交和情緒發展,滿足了這些需求。製造商正透過改進產品設計和推出吸引兒童和家長的創新理念來回應這一需求。隨著需求的持續成長,全球積木玩具市場預計將保持強勁的成長勢頭,這得益於其在提供引人入勝且注重發展的玩樂體驗方面的優勢。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 91億美元 |

| 預計金額 | 189億美元 |

| 複合年成長率 | 7.6% |

預計到2025年,基礎積木市場規模將達到40億美元,並在2026年至2035年間以7.1%的複合年成長率成長。該細分市場持續成長的主要動力源於其靈活的設計和在各個年齡層中經久不衰的受歡迎程度。模組化結構使用戶能夠自由地修改和自訂結構,從而激發創造力和想像。互鎖設計使其應用範圍廣泛,使用者可以在嘗試各種形狀和結構的同時,進一步提升創造力。

預計到2025年,6至12歲兒童市場將佔據30.1%的市場。該年齡層兒童是重要的消費群體,因為相關產品與兒童成長發展的需求高度契合。結構化的遊戲活動有助於認知發展和社交互動,因此積木成為該年齡層兒童的首選。積木產品能夠持續滿足不斷變化的學習需求和興趣,也支撐了市場對這些產品的持續需求。

美國積木玩具市場預計到2025年將達到18億美元,並在2026年至2035年間以7.5%的複合年成長率成長。市場需求強勁成長的驅動力是人們對寓教於樂和早期發展意識的不斷提高。憑藉持續的產品創新和廣泛的消費者吸引力,知名品牌繼續保持強大的市場地位。同時,各公司也致力於使用永續材料,以應對日益增強的環保意識。創新與負責任的生產方式結合,共同推動了市場需求的長期穩定成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 產業生態系分析

- 原物料供應商

- 零件製造商

- 玩具製造商和品牌

- 銷售代理商和批發商

- 零售商

- 最終消費者

- 每個階段增加的價值

- 影響產業的因素

- 促進因素

- STEM教育和益智玩具越來越受歡迎。

- 拓展授權與品牌合作關係

- 對無螢幕遊戲和創造性發展的需求日益成長。

- 市場挑戰

- 激烈的競爭和對價格的敏感性

- 安全隱患和嚴格的監管挑戰

- 機會

- 永續與環保產品創新

- 數位整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 世界玩具安全標準

- ASTM F963(美國)

- EN 71(歐盟)

- GB 6675

- ISO 8124

- 化學物質管制

- 窒息風險和年齡標籤要求

- 進出口合規與認證

- 數位產品護照的要求(歐盟)

- 世界玩具安全標準

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 材料創新

- 智慧建構模組與物聯網的整合

- 擴增實境(AR)整合

- 製造技術的進步

- 數位設計和客製化工具

- 2025年價格分析

- 按地區

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 供應鏈分析

- 世界製造地

- 原料採購和永續性

- 物流及配送網路

- 供應鏈脆弱性與風險緩解

- 近岸外包與區域製造業趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 中國的貿易趨勢與跨境電子商務

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 按地區和格式分類的頻道覆蓋範圍

- 缺乏最後一公里基礎設施和不斷變化的管道

- 消費行為分析

- 人口趨勢和買家畫像

- 購買決策因素

- 採購流程和接觸點分析

- 區域和文化偏好

- 品牌忠誠度和重複購買行為

- 購買後的操作

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 基本積木

- 主題套裝

- 教育模組

- 其他(磁性玩具、電子積木玩具等)

第6章 市場估計與預測:依材料分類,2022-2035年

- 塑膠

- 樹

- 形式

- 矽酮

- 其他(回收材料等)

第7章 市場估計與預測:依年齡層別分類,2022-2035年

- 嬰幼兒(0-2歲)

- 幼兒(3-5歲)

- 兒童(6-12歲)

- 青少年

- 成人

第8章 市場估算與預測:依價格區間分類,2022-2035年

- 低的

- 中等的

- 高的

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 玩具專賣店

- 百貨公司

- 其他(例如,教育類商店)

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

第11章:公司簡介

- 世界公司

- The LEGO Group

- Mattel, Inc.

- Hasbro, Inc.

- Spin Master Corp.

- Bandai Namco Holdings Inc.

- Ravensburger AG

- 當地公司

- Magna-Tiles(Valtech LLC)

- Guidecraft

- Melissa &Doug

- Geomagworld SA

- HABA

- COBI SA

- Sluban

- 新興企業

- Magformers LLC

- PicassoTiles

- Tegu

- K'NEX Brands

- Plus-Plus A/S

- Kawada Co. Ltd.

- LaQ

- LOZ Group

The Global Building Blocks Toys Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 18.9 billion by 2035.

Increasing emphasis on STEM-focused learning is encouraging the adoption of toys that promote problem-solving, creativity, and hands-on engagement. Parents, educators, and policymakers are placing greater importance on early exposure to foundational skills that support long-term development. This shift is not only driven by academic considerations but also by a broader focus on well-rounded child development. Consumers are actively seeking products that combine entertainment with educational value, reflecting a growing preference for purposeful play. Building block toys align with these expectations by supporting cognitive, social, and emotional growth. Manufacturers are responding by enhancing product designs and introducing innovative concepts that appeal to both children and guardians. As demand continues to rise, the global building blocks toys market is expected to maintain strong momentum, driven by its ability to deliver engaging and development-oriented play experiences.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $18.9 Billion |

| CAGR | 7.6% |

The basic blocks segment generated USD 4 billion in 2025 and is anticipated to grow at a CAGR of 7.1% from 2026 to 2035. This segment remains dominant due to its flexible design and long-standing appeal across different age groups. Modular construction allows users to modify and customize structures, encouraging creativity and imaginative thinking. The interlocking design supports a wide range of applications, enabling users to explore various forms and structures while enhancing their creative capabilities.

The children aged 6 to 12 years segment accounted for 30.1% share in 2025. This segment represents a key consumer base, as products are closely aligned with developmental requirements during formative years. Structured play activities contribute to cognitive development and social interaction, making building block toys a preferred choice for this age group. Continued demand is supported by the alignment of these products with evolving learning needs and interests.

United States Building Blocks Toys Market reached USD 1.8 billion in 2025 and is projected to grow at a CAGR of 7.5% from 2026 to 2035. Strong demand is driven by increasing awareness of educational play and early development. Established brands continue to maintain a strong presence, supported by consistent product innovation and broad consumer appeal. Companies are also focusing on sustainable materials to align with growing environmental awareness. The integration of innovation and responsible manufacturing practices is helping sustain long-term demand in the market.

Key companies operating in the Global Building Blocks Toys Market include The LEGO Group, Mattel, Inc., Hasbro, Inc., Spin Master Corp., Bandai Namco Holdings Inc., Ravensburger AG, Magna-Tiles (Valtech LLC), Guidecraft, Melissa & Doug, Geomagworld SA, HABA, COBI S.A., Sluban, Magformers LLC, PicassoTiles, Tegu, K'NEX Brands, Plus-Plus A/S, Kawada Co. Ltd., LaQ, and LOZ Group. Companies in the Building Blocks Toys Market are strengthening their market position through continuous innovation, product diversification, and strategic collaborations. Manufacturers are focusing on developing educational and skill-based products that align with modern learning trends. Investment in research and development is enabling the introduction of new designs, improved materials, and enhanced product functionality. Companies are also expanding their distribution networks to increase global reach and accessibility. Sustainability initiatives, including the use of eco-friendly materials, are becoming a key focus area to meet consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Age Group

- 2.2.5 Price

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Industry ecosystem analysis

- 3.1.2 Raw material suppliers

- 3.1.3 Component manufacturers

- 3.1.4 Toy manufacturers & brands

- 3.1.5 Distributors & wholesalers

- 3.1.6 Retailers

- 3.1.7 End consumers

- 3.1.8 Value addition at each stage

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising popularity of STEM education & educational toys

- 3.2.1.2 Expansion of licensing & brand collaborations

- 3.2.1.3 Increasing demand for screen-free play & creative development

- 3.2.2 Market pitfalls

- 3.2.2.1 Intense competition & price sensitivity

- 3.2.2.2 Safety concerns & stringent regulatory challenges

- 3.2.3 Opportunities

- 3.2.3.1 Sustainable & Eco-Friendly Product Innovation

- 3.2.3.2 Digital Integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global Toy Safety Standards

- 3.4.1.1 ASTM F963 (United States)

- 3.4.1.2 EN 71 (European Union)

- 3.4.1.3 GB 6675

- 3.4.1.4 ISO 8124

- 3.4.2 Chemical restrictions

- 3.4.3 Choking hazard & age labeling requirements

- 3.4.4 Import/export compliance & certification

- 3.4.5 Digital product passport requirements (EU)

- 3.4.1 Global Toy Safety Standards

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Material innovation

- 3.6.2 Smart building blocks & IoT integration

- 3.6.3 Augmented reality (AR) integration

- 3.6.4 Manufacturing technology advances

- 3.6.5 Digital design & customization tools

- 3.7 Pricing analysis, 2025

- 3.7.1 By region

- 3.7.2 Historical price trend analysis

- 3.7.3 Pricing strategy by player type (premium / value / cost-plus)

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Supply chain analysis

- 3.11.1 Global manufacturing hubs

- 3.11.2 Raw material sourcing & sustainability

- 3.11.3 Logistics & distribution network

- 3.11.4 Supply chain vulnerabilities & risk mitigation

- 3.11.5 Nearshoring & regional manufacturing trends

- 3.12 Trade data analysis (driven by paid database) (HS code- 950300)

- 3.12.1 Import/export volume & value trends

- 3.12.2 Key trade corridors & tariff impact

- 3.12.3 China trade dynamics & cross-border e-commerce

- 3.13 Impact of AI & Generative AI on the market

- 3.13.1 AI-Driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Distribution infrastructure & channel penetration landscape

- 3.14.1 Channel coverage by region & format

- 3.14.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.15 Consumer behavior analysis

- 3.15.1 Demographic trends & buyer profiles

- 3.15.2 Purchase decision factors

- 3.15.3 Shopping journey & touchpoint analysis

- 3.15.4 Regional & cultural preferences

- 3.15.5 Brand loyalty & repeat purchase behavior

- 3.15.6 Post-purchase behavior

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Basic blocks

- 5.3 Themed sets

- 5.4 Educational blocks

- 5.5 Others (magnetic, electronic block toys, etc.)

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Wood

- 6.4 Foam

- 6.5 Silicone

- 6.6 Others (recycled materials, etc.)

Chapter 7 Market Estimates & Forecast, By Age Group, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Infants (0-2 years)

- 7.3 Toddlers (3-5 years)

- 7.4 Children (6-12 years)

- 7.5 Teenagers

- 7.6 Adults

Chapter 8 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Specialty toy stores

- 9.3.2 Departmental stores

- 9.3.3 Others (educational shops, etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 The LEGO Group

- 11.1.2 Mattel, Inc.

- 11.1.3 Hasbro, Inc.

- 11.1.4 Spin Master Corp.

- 11.1.5 Bandai Namco Holdings Inc.

- 11.1.6 Ravensburger AG

- 11.2 Regional Players

- 11.2.1 Magna-Tiles (Valtech LLC)

- 11.2.2 Guidecraft

- 11.2.3 Melissa & Doug

- 11.2.4 Geomagworld SA

- 11.2.5 HABA

- 11.2.6 COBI S.A.

- 11.2.7 Sluban

- 11.3 Emerging Brands

- 11.3.1 Magformers LLC

- 11.3.2 PicassoTiles

- 11.3.3 Tegu

- 11.3.4 K'NEX Brands

- 11.3.5 Plus-Plus A/S

- 11.3.6 Kawada Co. Ltd.

- 11.3.7 LaQ

- 11.3.8 LOZ Group