|

市場調查報告書

商品編碼

2045724

數位伺服馬達及驅動器市場機會、成長要素、產業趨勢分析及2026-2035年預測Digital Servo Motors and Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

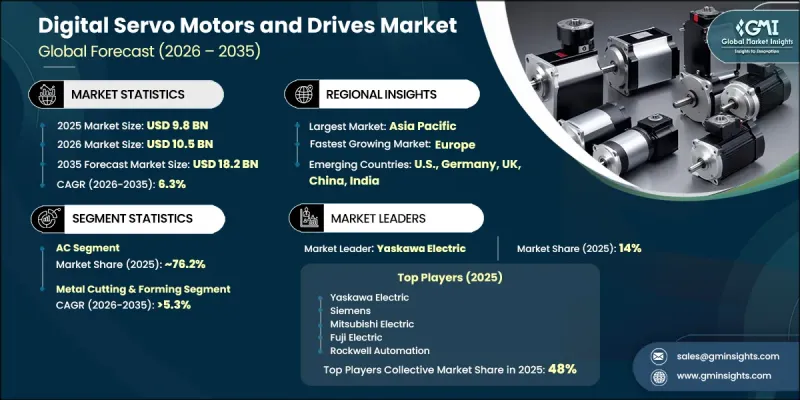

全球數位伺服馬達和驅動器市場預計到 2025 年將達到 98 億美元,年複合成長率為 6.3%,到 2035 年將達到 182 億美元。

節能技術的日益普及,以及旨在降低工業能耗的日益嚴格的法規,正顯著推動市場成長。工業基礎設施現代化投資的增加和對先進自動化技術需求的不斷成長,進一步鞏固了產業發展。數位伺服馬達和驅動器已成為現代工業活動中不可或缺的一部分,能夠實現精確的速度控制、提高運行效率、增強製程精度並最佳化系統性能。機器人、智慧製造系統和工業自動化技術的快速融合,正在加速全球對先進馬達控制解決方案的需求。此外,物聯網 (IoT) 技術和工業 4.0舉措的廣泛應用,正透過提升連接性、生產柔軟性和營運效率,改變製造業環境。對減少工業排放和排放製造設施能源管理的日益重視,也促進了數位化伺服系統的普及。隨著自動化技術的不斷進步和智慧製造方法的日益普及,預計未來幾年數位伺服馬達和驅動器行業的前景將更加光明。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 98億美元 |

| 預計金額 | 182億美元 |

| 複合年成長率 | 6.3% |

預計到2025年,交流伺服系統市佔率將達到76.2%,並在2035年之前以6.5%的複合年成長率成長。工業設施的持續現代化改造、維修和擴建,使得各行各業對先進的交流伺服系統需求強勁。自動化技術和數位通訊基礎設施在工業環境中的日益普及,進一步加速了產品的市場應用。交流伺服馬達和驅動器因其在恆定和變化負載條件下均能高效運行,提供精確的運動控制和可靠的性能而備受青睞。其柔軟性、能源效率以及與先進工業自動化系統的兼容性,不斷鞏固了其在全球市場的地位。

預計到2025年,金屬切削成形市場規模將達到18億美元,並在2026年至2035年間以5.3%的複合年成長率成長。對更高生產精度、更快運作速度和更強製造柔軟性的需求不斷成長,是推動該市場成長的主要動力。先進加工和成形製程的日益普及,需要精確定位、同步運作和快速反應能力,進一步提升了對數位伺服系統的需求。此外,機器人、CNC工具機、自動化生產線和智慧製造技術的日益廣泛應用,也推動了金屬加工領域產品的普及。

預計到2025年,美國數位伺服馬達和驅動器市場將佔據75%的市場佔有率,市場規模將達到18億美元。製造業、半導體製造設備、汽車應用及其他工業領域對工業自動化和機器人技術的積極應用,推動了對高精度伺服馬達和驅動器的需求。對智慧製造基礎設施、先進生產技術和工業效率提升的持續投資,進一步促進了美國市場的成長。隨著對操作精度、生產效率提升和節能工業系統的日益重視,預計美國市場對該產品的需求將繼續擴大。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 影響價值鏈的關鍵因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 成本結構分析:數位伺服馬達和驅動器

- 新機會與趨勢

- 利用物聯網技術實現數位轉型

- 進入新興市場

- 投資分析及未來展望

- 價格趨勢分析

- 透過驅動系統

- 按地區

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

- 生產能力和生產情況

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依驅動系統分類,2022-2035年

- AC

- DC

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 石油和天然氣

- 金屬切削/成型

- 物料輸送設備

- 包裝和貼標機械

- 機器人技術

- 醫療機器人

- 橡膠和塑膠機械

- 倉儲業

- 自動化

- 在惡劣環境下使用

- 半導體製造設備

- AGV

- 電子設備

- 其他

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 挪威

- 瑞典

- 丹麥

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 泰國

- 馬來西亞

- 菲律賓

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 卡達

- 南非

- 奈及利亞

- 埃及

- 阿爾及利亞

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第8章:公司簡介

- ABB

- Advanced Motion Controls

- Allient

- Applied Motion Products

- Baumuller

- Beckhoff Automation

- Bosch Rexroth

- Danfoss

- Delta Electronics

- Elmo Motion Control

- Festo

- Fuji Electric

- Harmonic Drive

- Infranor

- Kollmorgen

- Leadshine

- Mitsubishi Electric

- Nidec

- Omron

- Panasonic Industry

- Rockwell Automation

- Schneider Electric

- Siemens

- Yaskawa Electric

The Global Digital Servo Motors and Drives Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 18.2 billion by 2035.

Increasing adoption of energy-efficient technologies, combined with stricter regulations focused on reducing industrial energy consumption, is significantly supporting market expansion. Growing investments in industrial infrastructure modernization and the rising demand for advanced automation technologies are further strengthening industry growth. Digital servo motors and drives enable accurate speed control, improved operational efficiency, enhanced process precision, and optimized system performance, making them essential across modern industrial operations. The rapid integration of robotics, smart manufacturing systems, and industrial automation technologies is accelerating demand for advanced motor control solutions worldwide. In addition, the increasing implementation of Internet of Things technologies and Industry 4.0 initiatives is reshaping manufacturing environments by improving connectivity, production flexibility, and operational efficiency. Rising emphasis on reducing industrial emissions and improving energy management across manufacturing facilities is also contributing to increased deployment of digitally enabled servo systems. Continuous advancements in automation technologies and the growing adoption of intelligent manufacturing practices are expected to further strengthen the outlook for the digital servo motors and drives industry over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $18.2 Billion |

| CAGR | 6.3% |

The AC segment held a 76.2% share in 2025 and is anticipated to grow at a CAGR of 6.5% through 2035. Ongoing modernization, retrofitting, and expansion of industrial facilities are creating strong demand for advanced AC servo systems across multiple industries. Increasing integration of automation technologies and digital communication infrastructure within industrial environments is further accelerating product adoption. AC servo motors and drives are widely preferred due to their capability to operate efficiently under both constant and variable load conditions while delivering precise motion control and reliable performance. Their flexibility, energy efficiency, and compatibility with advanced industrial automation systems continue to strengthen their position across the global market.

The metal cutting and forming segment generated USD 1.8 billion in 2025 and is projected to grow at a CAGR of 5.3% from 2026 to 2035. Rising demand for greater production precision, faster operational speed, and improved manufacturing flexibility is contributing significantly to segment growth. Increasing adoption of advanced machining technologies and shaping processes requiring accurate positioning, synchronized movement, and rapid response capabilities is further supporting demand for digital servo systems. The growing utilization of robotics, CNC machinery, automated manufacturing lines, and intelligent production technologies is also driving product deployment across metal processing applications.

U.S. Digital Servo Motors and Drives Market accounted for 75% share in 2025 and generated USD 1.8 billion. Strong adoption of industrial automation and robotics across manufacturing operations, semiconductor equipment production, automotive applications, and other industrial sectors is fueling demand for high-precision servo motors and drives. Continued investments in smart manufacturing infrastructure, advanced production technologies, and industrial efficiency improvements are further supporting market growth throughout the country. The increasing focus on operational accuracy, productivity enhancement, and energy-efficient industrial systems is expected to continue driving product demand across the U.S. market.

Leading companies operating in the Global Digital Servo Motors and Drives Market include ABB, Siemens, Mitsubishi Electric, Yaskawa Electric, Schneider Electric, Rockwell Automation, Bosch Rexroth, Omron, Panasonic Industry, Delta Electronics, Danfoss, Fuji Electric, Kollmorgen, Beckhoff Automation, Leadshine, Advanced Motion Controls, Allient, Applied Motion Products, Baumuller, Elmo Motion Control, Festo, Harmonic Drive, Infranor, and Nidec. Companies operating in the digital servo motors and drives market focus on multiple strategic initiatives to strengthen their competitive position and expand global market presence. Manufacturers are increasing investments in research and development to introduce highly efficient servo systems with enhanced precision, connectivity, and energy-saving capabilities. Many companies are integrating artificial intelligence, IoT technologies, and advanced analytics into servo solutions to support smart manufacturing environments and predictive maintenance applications. Strategic collaborations, mergers, and acquisitions are also helping market participants expand technological expertise and strengthen regional distribution networks. In addition, businesses are focusing on customized automation solutions tailored to industry-specific requirements across manufacturing, robotics, and industrial processing sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Drive trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of digital servo motors and drives

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

- 3.10 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.10.1 By drive (Driven by Primary Research)

- 3.10.2 By region (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-Driven production optimization (Solution Core)

- 3.11.2 Predictive maintenance & fault detection (Solution Core)

- 3.12 Capacity & production landscape (Driven by Primary Research)

- 3.12.1 Capacity by region & key producer (Driven by Primary Research)

- 3.12.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Drive, 2022 - 2035 (USD Million, '000 Units)

- 5.1 Key trends

- 5.2 AC

- 5.3 DC

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, '000 Units)

- 6.1 Key trends

- 6.2 Oil and Gas

- 6.3 Metal Cutting & Forming

- 6.4 Material Handling Equipment

- 6.5 Packaging and Labeling Machinery

- 6.6 Robotics

- 6.7 Medical Robotics

- 6.8 Rubber & Plastics Machinery

- 6.9 Warehousing

- 6.10 Automation

- 6.11 Extreme Environment Applications

- 6.12 Semiconductor Machinery

- 6.13 AGV

- 6.14 Electronics

- 6.15 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Norway

- 7.3.7 Sweden

- 7.3.8 Denmark

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Thailand

- 7.4.7 Malaysia

- 7.4.8 Philippines

- 7.4.9 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.5.5 Nigeria

- 7.5.6 Egypt

- 7.5.7 Algeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Advanced Motion Controls

- 8.3 Allient

- 8.4 Applied Motion Products

- 8.5 Baumuller

- 8.6 Beckhoff Automation

- 8.7 Bosch Rexroth

- 8.8 Danfoss

- 8.9 Delta Electronics

- 8.10 Elmo Motion Control

- 8.11 Festo

- 8.12 Fuji Electric

- 8.13 Harmonic Drive

- 8.14 Infranor

- 8.15 Kollmorgen

- 8.16 Leadshine

- 8.17 Mitsubishi Electric

- 8.18 Nidec

- 8.19 Omron

- 8.20 Panasonic Industry

- 8.21 Rockwell Automation

- 8.22 Schneider Electric

- 8.23 Siemens

- 8.24 Yaskawa Electric

伺服馬達及驅動器市場:全球市場預測,2026-2032年

伺服馬達及驅動器市場:全球市場預測,2026-2032年 伺服馬達及驅動器市場預測至2034年-按組件、電壓範圍、產業、應用、最終用戶和地區分類的全球分析

伺服馬達及驅動器市場預測至2034年-按組件、電壓範圍、產業、應用、最終用戶和地區分類的全球分析 伺服馬達市場規模、佔有率和成長分析:按產品類型、電壓範圍、額定功率、通訊協定、系統類型、最終用戶產業、應用和地區分類-2026-2033年產業預測

伺服馬達市場規模、佔有率和成長分析:按產品類型、電壓範圍、額定功率、通訊協定、系統類型、最終用戶產業、應用和地區分類-2026-2033年產業預測 2026年全球房車減速機市場研究報告

2026年全球房車減速機市場研究報告 伺服馬達和步進馬達市場規模、佔有率和成長分析:按馬達類型、最終用戶細分市場、技術、銷售管道和地區分類-2026-2033年產業預測無鐵心直線伺服馬達市場:依馬達類型、行程長度、工作電壓、組件、安裝方式、應用、終端用戶產業分類,全球預測,2026-2032年

伺服馬達和步進馬達市場規模、佔有率和成長分析:按馬達類型、最終用戶細分市場、技術、銷售管道和地區分類-2026-2033年產業預測無鐵心直線伺服馬達市場:依馬達類型、行程長度、工作電壓、組件、安裝方式、應用、終端用戶產業分類,全球預測,2026-2032年 數位伺服馬達及驅動器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、設備分類

數位伺服馬達及驅動器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、設備分類 伺服馬達及驅動器:市場佔有率分析、產業趨勢及統計數據、成長預測(2026-2031)

伺服馬達及驅動器:市場佔有率分析、產業趨勢及統計數據、成長預測(2026-2031) 全球交流伺服馬達及驅動器市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球伺服馬達市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球交流伺服馬達及驅動器市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球伺服馬達市場規模、佔有率、趨勢和成長分析報告(2026-2034)