|

市場調查報告書

商品編碼

2045719

宗教和精神產品的市場機會、成長要素、產業趨勢以及 2026-2035 年的預測。Religious and Spiritual Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

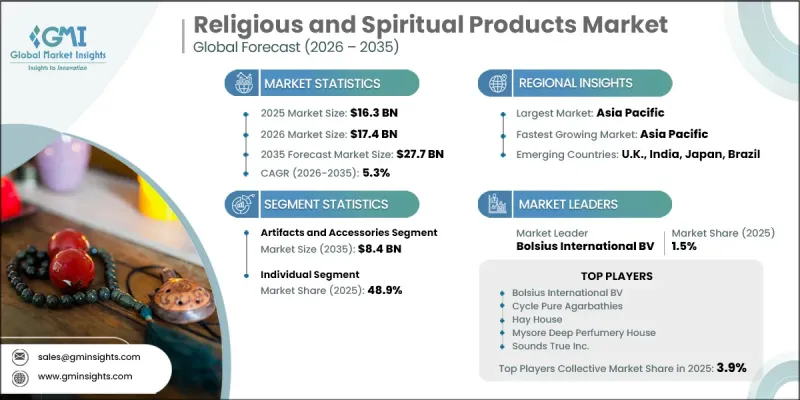

2025年全球宗教和精神產品市場價值163億美元,預計到2035年將以5.3%的複合年成長率成長至277億美元。

宗教和靈性產品產業的擴張源於靈性、情緒健康和日常實踐之間日益緊密的聯繫。消費者擴大將靈性產品融入日常生活,以此作為實現心理平衡、緩解壓力和獲得內心平靜的一種方式。人們對個人福祉和正念的日益重視,使得宗教和靈性產品對更廣泛的消費者群體更具吸引力。開發中國家可支配收入的成長也促使人們增加對高階宗教產品和儀式用品的支出,這些產品先前被視為奢侈品。此外,線上零售平台的快速發展極大地改變了產品的供應方式,使消費者無論身處何地都能購買到正宗的靈性產品。數位商務平台幫助知名品牌和利基品牌觸及更廣泛的客戶群,同時提升了客戶的購物便利性。政府主導的旅遊發展項目和宗教旅遊景點周邊基礎設施的改善,透過增加遊客數量和提升對宗教用品、收藏級靈性產品以及與聖地相關的豪華紀念品的需求,進一步推動了市場成長。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 163億美元 |

| 預測市場規模 | 277億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,工藝品及配件市場的銷售額將達到58億美元,到2035年將達到84億美元。由於消費者對能夠支持個人信仰活動和靈修實踐的實體產品有著強烈的偏好,因此該品類在宗教和靈性產品市場中持續佔據主導地位。裝飾品和禮拜用品被廣泛用於營造有意義的靈性環境,並提升個人禮拜體驗。消費者越來越重視兼具靈性意義和美學價值的產品,這使得工藝品及配件在功能性和裝飾性方面都成為至關重要的品類。人們對在家中和個人禮拜場所進行靈修實踐的興趣日益濃厚,進一步推動了該品類的需求成長。

到2025年,個人消費市場將佔48.9%的佔有率。個人靈修和以家庭為中心的宗教實踐的興起,持續推動著該品類強勁的消費支出。人們越來越傾向於投資能夠提升個人靈修體驗和促進個人健康習慣的產品。快節奏的都會生活和對精神平衡日益成長的需求,促使消費者在家中打造專屬空間,用於冥想、正念練習和靈修活動。這種個人化靈修方式的轉變,顯著提升了個人消費產品的需求,從而推動了個人消費市場的持續成長。

預計到2025年,美國宗教和靈性產品市佔率將達到76.8%。美國市場持續受益於龐大且多元化的消費群體,他們對信仰類和健康類產品有著濃厚的興趣。對家居靈修用品、冥想產品和信仰類商品的需求不斷成長,顯著推動了市場擴張。消費者對正念、情緒健康和超越傳統宗教實踐的自我護理的日益關注,也擴大了市場基本客群。此外,電子商務通路、訂閱式零售服務和數位靈性平台的快速發展,提高了產品的可及性,並推動了全部區域購買頻率的提升。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 文化建構與儀式延續

- 信仰型企業的興起與倫理消費主義

- 數位普及和電子商務的擴張

- 產業潛在風險與挑戰

- 對商業化的抵制與道德考量

- 職場和組織內部的緊張關係

- 機會

- 將精神健康融入老年醫療保健和服務中

- 體驗式與社群式精神消費的興起

- 促進因素

- 成長潛力分析

- 監理框架

- 關鍵市場趨勢與顛覆性因素

- 價格分析

- 對過去價格趨勢的分析

- 根據參與企業的類型(高階、價值、成本加成)所製定的定價策略

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於細分市場的生成式人工智慧的應用案例和部署藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 目前分銷基礎設施和通路滲透情況

- 以區域業態分類的通路覆蓋率(現代零售與傳統零售)

- 缺乏最後一公里基礎設施和不斷變化的管道

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 手工藝品和配件

- 宗教偶像和雕塑

- 念珠/玫瑰念珠

- 宗教飾品

- 蠟燭和香

- 裝飾性宗教用品

- 其他

- 禮儀用品

- 祭祀用品和儀式套裝

- 祈禱油和聖水

- 禮拜服和宗教服裝

- 祭壇用品

- 儀式用具和設備

- 數位產品

- 行動應用與平台

- 網路偏差內容

- 虛擬社區與服務

- 電子書和數位出版物

- 直播冥想和祈禱服務

- 教科書/文學

- 神聖的文本和經文

- 信仰書籍

- 教育和學習材料

- 精神自助書籍

- 其他

第6章 市場估算與預測:依最終用戶分類,2022-2035年

- 個人

- 宗教團體

- 其他

第7章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 企業網站

- 電子商務網站

- 離線

- 宗教書店

- 禮品店

- 專賣店

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

第9章:公司簡介

- 世界公司

- Bolsius

- Cathedral Candle

- Delsbo

- Hay House

- Llewellyn

- Nippon Kodo

- Shoyeido

- 當地公司

- Arte Barsanti

- FC Ziegler

- Ghirelli

- PEMA

- Sacred Source

- Sounds True

- Stuller

- 新興企業

- Cycle Pure

- HEM

- Hari Darshan

- Mysore Deep

- Rgyan

- Satya

- Shubhkart

- Veronese Design

The Global Religious and Spiritual Products Market was valued at USD 16.3 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 27.7 billion by 2035.

Expansion across the religious and spiritual products industry is by the increasing connection between spirituality, emotional wellness, and everyday lifestyle practices. Consumers are increasingly incorporating spiritual products into their daily routines as part of their efforts to achieve mental balance, stress relief, and emotional comfort. Growing awareness regarding personal well-being and mindfulness has significantly broadened the appeal of faith-based and spiritual merchandise across multiple consumer groups. Rising disposable incomes in developing economies are also contributing to higher spending on premium devotional products and ceremonial items that were previously considered luxury purchases. In addition, the rapid growth of online retail platforms has transformed product accessibility by enabling consumers to purchase authentic spiritual goods regardless of geographic location. Digital commerce platforms are helping both established and niche brands reach wider audiences while improving customer convenience. Government-backed tourism development programs and infrastructure improvements around religious destinations are further supporting market growth by increasing visitor traffic and demand for devotional merchandise, collectible spiritual products, and premium commemorative items associated with sacred locations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.3 Billion |

| Forecast Value | $27.7 Billion |

| CAGR | 5.3% |

The artifacts and accessories segment generated USD 5.8 billion in 2025 and is expected to reach USD 8.4 billion by 2035. This category continues to hold a leading position within the religious and spiritual products market due to strong consumer preference for tangible items that support personal faith practices and spiritual routines. Decorative and devotional products are widely used to create meaningful spiritual environments and enhance individual worship experiences. Consumers increasingly value products that combine spiritual significance with aesthetic appeal, making artifacts and accessories an important category across both functional and decorative applications. Rising interest in home-based spiritual practices and personalized devotional spaces is further strengthening demand within this segment.

The individual consumer segment accounted for 48.9% share in 2025. The growing shift toward personal spirituality and home-centered religious practices continues to support strong consumer spending within this category. Individuals are increasingly investing in products that enhance private spiritual experiences and support personal wellness routines. Fast-paced urban lifestyles and growing demand for emotional balance have encouraged consumers to establish dedicated spaces within their homes for reflection, mindfulness, and spiritual activities. This transition toward individualized spiritual engagement has significantly increased demand for products designed for personal use, contributing to the continued expansion of the individual consumer segment.

United States Religious and Spiritual Products Market held a 76.8% share in 2025. The U.S. market continues to benefit from a large and diverse consumer base with a strong interest in devotional and wellness-oriented products. Growing demand for home-focused spiritual items, meditation-related products, and faith-based merchandise is contributing significantly to market expansion. Increasing consumer focus on mindfulness, emotional wellness, and self-care beyond traditional religious practices has also expanded the market's customer base. Additionally, the rapid development of e-commerce channels, subscription-based retail services, and digital spiritual platforms has improved product accessibility and encouraged higher purchasing frequency throughout the region.

Key companies operating in the Global Religious and Spiritual Products Market include Arte Barsanti, Bolsius, Cathedral Candle, Cycle Pure, Delsbo, F.C. Ziegler, Ghirelli, Hari Darshan, Hay House, HEM, Llewellyn, Mysore Deep, Nippon Kodo, PEMA, Rgyan, Sacred Source, Satya, Shoyeido, Shubhkart, Sounds True, Stuller, and Veronese Design. Companies operating in the religious and spiritual products industry are implementing multiple strategies to strengthen their market presence and improve long-term competitiveness. Leading brands are focusing on expanding product portfolios with premium-quality, handcrafted, and eco-friendly devotional products to meet changing consumer preferences. Businesses are also increasing investments in digital commerce platforms and direct-to-consumer sales channels to improve product accessibility and customer engagement worldwide. Many companies are strengthening brand visibility through collaborations with spiritual organizations, wellness communities, and online influencers. Product customization, limited-edition collections, and culturally inspired designs are helping manufacturers attract a wider customer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.9 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 End user

- 2.2.4 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Cultural embeddedness and ritual continuity

- 3.2.1.2 Rise of faith-based enterprises and ethical consumerism

- 3.2.1.3 Digital evangelism and e-commerce expansion

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Commercialization backlash and moral sensitivities

- 3.2.2.2 Workplace and organizational tensions

- 3.2.3 Opportunities

- 3.2.3.1 Integration of spiritual wellness into healthcare and aging services

- 3.2.3.2 Rise of experiential and community-based spiritual consumption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.5 Major market trends and disruptions

- 3.6 Pricing Analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Future market trends

- 3.8 Trade data analysis (driven by paid database) (HS Code 71171930)

- 3.8.1 Import/export volume & value trends (driven by primary research)

- 3.8.2 Key trade corridors & tariff impact (driven by primary research)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Gen-AI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. Traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Artifacts & Accessories

- 5.2.1 Religious Idols & Statues

- 5.2.2 Prayer Beads & Rosaries

- 5.2.3 Religious Jewelry

- 5.2.4 Candles & Incense

- 5.2.5 Decorative Religious Items

- 5.2.6 Others

- 5.3 Ceremonial Items

- 5.3.1 Puja Kits & Ritual Sets

- 5.3.2 Prayer Oils & Holy Water

- 5.3.3 Vestments & Religious Garments

- 5.3.4 Altar Supplies

- 5.3.5 Ritual Tools & Instruments

- 5.4 Digital Products

- 5.4.1 Mobile Apps & Platforms

- 5.4.2 Online Devotional Content

- 5.4.3 Virtual Communities & Services

- 5.4.4 E-books & Digital Publications

- 5.4.5 Streaming Meditation & Prayer Services

- 5.5 Textbooks & Literature

- 5.5.1 Sacred Texts & Scriptures

- 5.5.2 Devotional Books

- 5.5.3 Educational & Study Materials

- 5.5.4 Spiritual Self-Help Literature

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Individual

- 6.3 Religious institutions

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Online

- 7.2.1 Company website

- 7.2.2 E-commerce website

- 7.3 Offline

- 7.3.1 Religious bookstores

- 7.3.2 Gift shops

- 7.3.3 Specialty stores

- 7.3.4 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Global Companies

- 9.1.1 Bolsius

- 9.1.2 Cathedral Candle

- 9.1.3 Delsbo

- 9.1.4 Hay House

- 9.1.5 Llewellyn

- 9.1.6 Nippon Kodo

- 9.1.7 Shoyeido

- 9.2 Regional Companies

- 9.2.1 Arte Barsanti

- 9.2.2 F.C. Ziegler

- 9.2.3 Ghirelli

- 9.2.4 PEMA

- 9.2.5 Sacred Source

- 9.2.6 Sounds True

- 9.2.7 Stuller

- 9.3 Emerging Companies

- 9.3.1 Cycle Pure

- 9.3.2 HEM

- 9.3.3 Hari Darshan

- 9.3.4 Mysore Deep

- 9.3.5 Rgyan

- 9.3.6 Satya

- 9.3.7 Shubhkart

- 9.3.8 Veronese Design

零浪費消費品市場預測至2034年:按產品類型、廢棄物減量方法、材料類型、分銷通路和最終用戶分類的全球分析

零浪費消費品市場預測至2034年:按產品類型、廢棄物減量方法、材料類型、分銷通路和最終用戶分類的全球分析 古董和收藏品市場規模、佔有率和成長分析:按產品類型、分銷通路、價格範圍、最終用戶細分市場、銷售管道和地區分類-2026-2033年產業預測

古董和收藏品市場規模、佔有率和成長分析:按產品類型、分銷通路、價格範圍、最終用戶細分市場、銷售管道和地區分類-2026-2033年產業預測 古董和收藏品市場機會、成長促進因素、產業趨勢分析與預測(2026-2035年)

古董和收藏品市場機會、成長促進因素、產業趨勢分析與預測(2026-2035年) 2026-2030年全球永續消費品市場消費品市場環境評估系統預測(至 2032 年):按評估類型、部署模型、技術、應用、最終用戶和地區進行的全球分析

2026-2030年全球永續消費品市場消費品市場環境評估系統預測(至 2032 年):按評估類型、部署模型、技術、應用、最終用戶和地區進行的全球分析 如何在印度消費品市場中獲勝(全面實用的行銷指南)進軍印度快速消費品市場的第一步

如何在印度消費品市場中獲勝(全面實用的行銷指南)進軍印度快速消費品市場的第一步