|

市場調查報告書

商品編碼

2038663

重組蛋白市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Recombinant Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

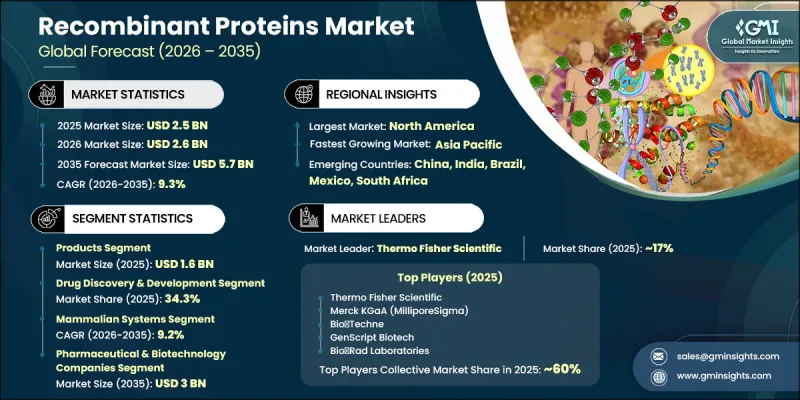

全球重組蛋白市場預計到 2025 年將價值 25 億美元,預計到 2035 年將以 9.3% 的複合年成長率成長至 57 億美元。

這一成長主要得益於治療性蛋白質在癌症、糖尿病和自體免疫疾病等慢性病和危及生命的疾病治療中日益廣泛的應用。慢性病負擔的加重,加上全球人口老化,進一步加速了創新治療方法的需求。重組蛋白利用DNA重組技術設計,並在細菌、酵母菌或哺乳動物細胞等宿主系統中生產。這使得難以在自然界中提取的目標蛋白質能夠大規模生產。由於其精確性、擴充性和可靠性,這些蛋白在治療、診斷和研究領域有著廣泛的應用。生物技術的不斷進步,以及在藥物開發和個人化醫療領域應用的不斷擴展,正提升其在現代醫療保健系統中的重要性。對研究基礎設施投入的增加和生物製藥的日益普及,也進一步推動了市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預測金額 | 57億美元 |

| 複合年成長率 | 9.3% |

預計到2025年,該產品市場規模將達到16億美元。重組蛋白在製藥、生技和科研領域的廣泛應用推動了強勁的需求。對生物製藥治療方法的日益依賴進一步促進了產品的普及。此外,蛋白質工程技術的不斷進步使得開發更穩定、功能更優的蛋白質產品成為可能,從而鞏固了該市場的持續主導地位。

預計到2025年,藥物發現與開發領域將佔據34.3%的市場。此領域涵蓋生物製藥、疫苗以及細胞和基因治療等應用。重組蛋白廣泛應用於藥物發現過程的多個階段,包括標靶識別、檢驗和臨床評估。它們在闡明生物學機制和推動治療方法創新方面發揮著重要作用,從而推動了強勁的需求。對個人化醫療的日益重視,以及慢性病盛行率的不斷上升,進一步凸顯了重組蛋白在藥物研發活動中的重要性。

預計北美重組蛋白市場將保持領先地位,2025年市佔率將達到48.4%。該地區受益於強大的生物技術和製藥生態系統,為蛋白質治療方法的創新提供了有力支持。完善的醫療基礎設施和慢性病的高發生率持續推動對先進治療方案的需求。健全的管理體制以及對研發的大量投入,進一步促進了市場擴張。精準醫療的日益普及也為該地區的持續成長做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 生物製藥和治療性蛋白質的需求不斷成長

- 蛋白質工程的進展

- 慢性疾病和感染疾病增加

- 產業潛在風險與挑戰

- 高昂的生產成本

- 嚴格的監管要求

- 市場機遇

- 個人化醫療和精準蛋白質療法的擴展

- 將外包業務擴展到專業的蛋白質服務供應商

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 技術與創新趨勢(基於初步調查)

- 目前技術

- 新興技術

- 投資和資金籌措趨勢(基於初步調查)

- 人工智慧/通用人工智慧對市場的影響(基於初步研究)

- 專利分析(基於初步研究)

- 價格分析(基於初步調查)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品與服務分類,2022-2035年

- 產品

- 細胞激素和生長因子

- 干擾素(IFN)

- 白細胞介素(IL)

- 其他細胞激素和生長因子

- 抗體

- 免疫查核點蛋白

- 病毒抗原

- 酵素

- 激酶

- 代謝酵素

- 其他酵素

- 重組調控蛋白

- 荷爾蒙

- 其他產品

- 細胞激素和生長因子

- 生產服務

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 藥物發現與開發

- 生物製藥

- 疫苗

- 細胞和基因治療

- 調查

- 診斷

- 其他用途

第7章 市場估計與預測:依宿主細胞類型分類,2022-2035年

- 哺乳動物系統

- 昆蟲細胞

- 酵母和真菌

- 細菌細胞

- 其他宿主細胞

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 製藥和生物技術公司

- 學術和研究機構

- 合約研究組織(CRO)

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abnova

- ACROBiosystems Group

- Bio Rad Laboratories

- Bio Techne

- BPS Bioscience

- Creative BioMart

- GenScript Biotech

- Merck KGaA(MilliporeSigma)

- Miltenyi Biotec

- Proteintech Group

- ProteoGenix

- RayBiotech

- Sino Biological

- Thermo Fisher Scientific

The Global Recombinant Proteins Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 5.7 billion by 2035.

Growth is driven by the increasing use of therapeutic proteins in treating chronic and life-threatening conditions, including cancer, diabetes, and autoimmune diseases. A rising global geriatric population, along with a higher burden of chronic illnesses, is further accelerating demand for innovative treatment approaches. Recombinant proteins are engineered through DNA recombination techniques and produced using host systems such as bacterial, yeast, or mammalian cells, enabling large-scale production of targeted proteins that are otherwise difficult to extract naturally. These proteins are widely applied across therapeutics, diagnostics, and research activities due to their precision, scalability, and reliability. Continuous advancements in biotechnology, combined with expanding applications in drug development and personalized medicine, are strengthening their importance in modern healthcare systems. Increasing investment in research infrastructure and growing adoption of biologics are further reinforcing market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 9.3% |

The products segment reached USD 1.6 billion in 2025. Strong demand is supported by the widespread use of recombinant proteins across pharmaceutical, biotechnology, and research applications. Growing reliance on biologic-based therapies is further driving product adoption. Continuous improvements in protein engineering are also enabling the development of more stable and functionally enhanced protein products, supporting sustained market dominance.

The drug discovery and development segment held 34.3% share in 2025. This segment includes biologics, vaccines, and cell and gene therapy applications. Recombinant proteins are widely used in multiple stages of drug development, including target identification, validation, and clinical evaluation. Their role in studying biological mechanisms and supporting therapeutic innovation is driving strong demand. Increasing focus on personalized treatment approaches, along with rising chronic disease prevalence, is further strengthening the importance of recombinant proteins in pharmaceutical research and development activities.

North America Recombinant Proteins Market accounted for 48.4% share in 2025, maintaining its leading position. The region benefits from a strong biotechnology and pharmaceutical ecosystem that supports innovation in protein-based therapies. A well-established healthcare infrastructure and high prevalence of chronic diseases continue to drive demand for advanced treatment solutions. Strong regulatory systems, along with significant investment in research and development, further support market expansion. Growing emphasis on precision medicine is also contributing to sustained regional growth.

Key companies operating in the Global Recombinant Proteins Market include Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), GenScript Biotech, Bio-Techne, Sino Biological, ACROBiosystems Group, Abnova, Proteintech Group, RayBiotech, Creative BioMart, BPS Bioscience, ProteoGenix, Bio-Rad Laboratories, and Miltenyi Biotec. Companies in the Recombinant Proteins Market are strengthening their position through continuous innovation in protein engineering and expansion of product portfolios. They are investing in advanced manufacturing technologies to improve production efficiency and scalability. Strategic collaborations with pharmaceutical and biotechnology firms are enhancing research capabilities and accelerating product development. Many players are focusing on expanding their global distribution networks to improve market access. In addition, companies are increasing investment in GMP-compliant production facilities to ensure product quality and regulatory compliance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Products & services trends

- 2.2.3 Application trends

- 2.2.4 Host-cell trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for biopharmaceuticals and therapeutic proteins

- 3.2.1.2 Advancements in protein engineering

- 3.2.1.3 Growing prevalence of chronic and infectious diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized medicine and precision protein therapeutics

- 3.2.3.2 Growing outsourcing to specialized protein service providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Investment and funding landscape (Driven by Primary Research)

- 3.7 Impact of AI/ gen AI on the market (Driven by Primary Research)

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Products & Services, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Products

- 5.2.1 Cytokines & growth factors

- 5.2.1.1 Interferons (IFNs)

- 5.2.1.2 Interleukins (ILs)

- 5.2.1.3 Other cytokines & growth factors

- 5.2.2 Antibodies

- 5.2.3 Immune checkpoint proteins

- 5.2.4 Virus antigens

- 5.2.5 Enzymes

- 5.2.5.1 Kinases

- 5.2.5.2 Metabolic enzymes

- 5.2.5.3 Other enzymes

- 5.2.6 Recombinant regulatory proteins

- 5.2.7 Hormones

- 5.2.8 Other products

- 5.2.1 Cytokines & growth factors

- 5.3 Production services

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Drug discovery & development

- 6.2.1 Biologics

- 6.2.2 Vaccines

- 6.2.3 Cell & gene therapies

- 6.3 Research

- 6.4 Diagnostics

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Host-cell, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Mammalian systems

- 7.3 Insect cells

- 7.4 Yeast & fungi

- 7.5 Bacterial cells

- 7.6 Other host-cells

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical & biotechnology companies

- 8.3 Academic & research institutes

- 8.4 Contract research organizations (CRO's)

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abnova

- 10.2 ACROBiosystems Group

- 10.3 Bio Rad Laboratories

- 10.4 Bio Techne

- 10.5 BPS Bioscience

- 10.6 Creative BioMart

- 10.7 GenScript Biotech

- 10.8 Merck KGaA (MilliporeSigma)

- 10.9 Miltenyi Biotec

- 10.10 Proteintech Group

- 10.11 ProteoGenix

- 10.12 RayBiotech

- 10.13 Sino Biological

- 10.14 Thermo Fisher Scientific

重組蛋白市場-2026-2032年全球市場預測

重組蛋白市場-2026-2032年全球市場預測 重組蛋白市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年

重組蛋白市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年 天然蛋白質市場報告:趨勢、預測和競爭分析(至2035年)

天然蛋白質市場報告:趨勢、預測和競爭分析(至2035年) 重組人類紅血球生成素市場:按藥物類型、應用、分銷管道和地區分類客製化重組蛋白生產服務市場:按表達系統、最終用戶和地區分類重組蛋白市場:依產品類型、表現系統、應用、最終用戶和地區分類GMP蛋白質市場報告:趨勢、預測和競爭分析(至2035年)

重組人類紅血球生成素市場:按藥物類型、應用、分銷管道和地區分類客製化重組蛋白生產服務市場:按表達系統、最終用戶和地區分類重組蛋白市場:依產品類型、表現系統、應用、最終用戶和地區分類GMP蛋白質市場報告:趨勢、預測和競爭分析(至2035年) 重組蛋白全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

重組蛋白全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 重組蛋白市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年重組Glucocerebrosidase市場依產品、劑型、通路及最終用戶分類,全球預測(2026-2032年)

重組蛋白市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年重組Glucocerebrosidase市場依產品、劑型、通路及最終用戶分類,全球預測(2026-2032年)