|

市場調查報告書

商品編碼

2038658

2026 年至 2035 年 3D 列印塑膠的市場機會、成長要素、產業趨勢分析與預測。3D Printing Plastics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

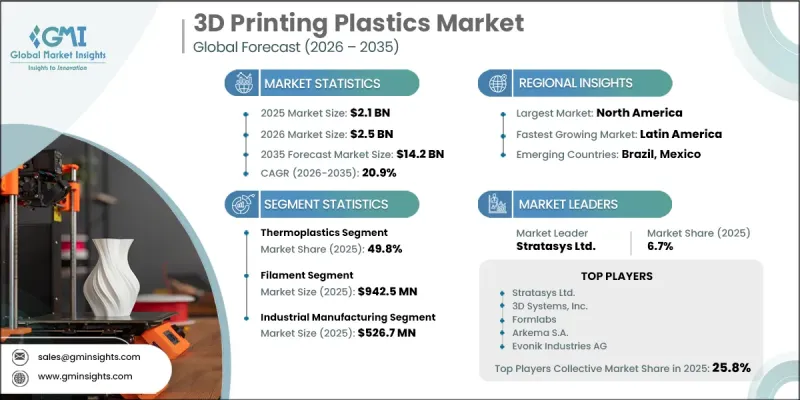

預計到 2025 年,全球 3D 列印用塑膠市場價值將達到 21 億美元,並以 20.9% 的複合年成長率成長,到 2035 年將達到 142 億美元。

受積層製造技術快速發展、材料持續創新以及3D列印在工業應用中日益廣泛的使用所驅動,該市場呈現強勁成長勢頭。其中一個關鍵成長要素是向多材料和複合材料列印系統的轉變,這些系統能夠提高成品零件的結構強度、耐久性和耐熱性。人工智慧(AI)和衍生設計能力的整合,透過提高材料利用率、減少廢棄物以及實現預測性和自動化製造工作流程,進一步變革了生產流程。工業製造仍是核心應用領域,其在模具、原型和終端功能零件等領域已廣泛應用。汽車、航太、醫療和消費品產業的需求也在不斷成長,這些產業對客製化和設計柔軟性要求極高。從區域來看,亞太地區憑藉其大規模的工業擴張引領銷售,而北美則受益於強大的技術創新和支援性政策框架。歐洲持續推廣永續性製造實踐,而拉丁美洲和中東及非洲地區儘管面臨基礎設施方面的限制,但其採用率也逐漸提高。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 21億美元 |

| 預計金額 | 142億美元 |

| 複合年成長率 | 20.9% |

熱塑性樹脂市場佔有率高達49.8%,預計到2035年將以20.8%的複合年成長率成長。其市場主導地位源自於其與廣泛應用的積層製造技術(尤其是熔融沈積成型(FDM)和選擇性雷射燒結(SLS))的高度相容性,使其在工業生產中用途廣泛。此外,其易於加工、可回收和優異的機械性能也進一步推動了其在眾多領域的應用。

預計到 2025 年,長絲材料市場規模將達到 9.425 億美元,並在 2026 年至 2035 年期間以 20.6% 的複合年成長率成長。由於長絲材料在擠出列印系統中廣泛應用,因此它們繼續主導積層製造市場,使其成為工業和商業應用中原型製作和經濟高效生產應用的理想材料。

預計2026年至2035年間,北美3D列印塑膠市場將以20.9%的複合年成長率成長。該地區在航太、醫療和汽車行業正經歷著高普及率,這得益於早期的技術成熟度和領先企業組成的強大生態系統。成熟企業的存在以及產品研發領域的持續創新,進一步加速了材料進步和市場擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 熱塑性樹脂

- 丙烯腈丁二烯苯乙烯(ABS)

- 聚乳酸(PLA)

- 聚醯胺(尼龍)

- 聚醚醚酮(PEEK)

- 聚碳酸酯(PC)

- 聚對苯二甲酸乙二醇酯(PETG)

- 聚苯碸(PPSU)

- 其他材料(TPU、PPS、PEI)

- 光固化樹脂

- 標準樹脂

- 高強度耐久樹脂

- 柔軟性樹脂

- 耐熱樹脂

- 生物相容性樹脂

- 其他

第6章 市場估計與預測:依類型分類,2022-2035年

- 燈絲

- 標準直徑(1.75毫米)

- 大直徑(2.85毫米或以上)

- 粉末

- 細懸浮微粒(小於50微米)

- 中等大小的顆粒(50-100微米)

- 液體/樹脂

- 紫外光固化樹脂

- 熱固性樹脂

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 車

- 內部零件

- 外部部件

- 動力傳動系統部件

- 模具和夾具

- 航太/國防

- 飛機內裝部件

- 結構部件

- 無人機和無人飛行器應用

- 模具和夾具

- 衛生保健

- 醫療設備

- 義肢和矯正器具

- 牙科用途

- 手術計劃和解剖模型

- 消費品

- 鞋類

- 眼鏡產品

- 玩具和遊戲

- 體育用品

- 家居用品

- 工業製造

- 生產模具

- 夾具和固定裝置

- 機械臂末端執行器

- 功能原型

- 其他

- 建築/施工

- 教育與研究

- 電子學

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Stratasys Ltd.

- 3D Systems, Inc.

- Formlabs

- Arkema SA

- Evonik Industries AG

- EOS GmbH

- SABIC

- Henkel AG &Co. KGaA

- Materialise NV

- Shenzhen eSUN

The Global 3D Printing Plastics Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 20.9% to reach USD 14.2 billion in 2035.

The market is experiencing strong momentum driven by rapid advancements in additive manufacturing technologies, continuous material innovation, and the widening use of 3D printing across industrial applications. A major growth driver is the increasing shift toward multi-material and composite printing systems that enable enhanced structural strength, durability, and thermal resistance in finished components. The integration of artificial intelligence and generative design capabilities is further transforming production processes by improving material efficiency, reducing waste, and enabling predictive and automated manufacturing workflows. Industrial manufacturing remains a core application area, supported by widespread use in tooling, prototyping, and end-use functional parts. Demand is also expanding across automotive, aerospace, healthcare, and consumer goods industries, where customization and design flexibility are highly valued. Regionally, Asia Pacific leads in revenue due to large-scale industrial expansion, while North America benefits from strong technological innovation and supportive policy frameworks. Europe continues to emphasize sustainability-driven manufacturing practices, whereas Latin America and the Middle East & Africa are gradually increasing adoption despite infrastructure limitations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $14.2 Billion |

| CAGR | 20.9% |

The thermoplastics segment held a 49.8% share and is projected to grow at a CAGR of 20.8% through 2035. Their dominance is attributed to strong compatibility with widely used additive manufacturing techniques, particularly Fused Deposition Modeling and Selective Laser Sintering, which makes them highly versatile for industrial production. Their ease of processing, recyclability, and mechanical performance further strengthen their adoption across multiple sectors.

The filament materials accounted USD 942.5 million in 2025 and is expected to grow at a CAGR of 20.6% during 2026-2035. Filaments continue to dominate the additive manufacturing landscape due to their extensive use in extrusion-based printing systems, making them the preferred material for prototyping and cost-efficient production applications across both industrial and commercial use cases.

North America 3D Printing Plastics Market is projected to grow at a CAGR of 20.9% during 2026-2035. The region demonstrates strong adoption across aerospace, healthcare, and automotive industries, supported by early technological maturity and a robust ecosystem of leading manufacturers. The presence of established companies and continuous innovation in product development further accelerates material advancements and market expansion.

Major players operating in the Global 3D Printing Plastics Industry are Stratasys Ltd., 3D Systems, Inc., Formlabs, Arkema S.A., Evonik Industries AG, EOS GmbH, SABIC, Henkel AG & Co. KGaA, Materialise NV, and Shenzhen eSUN. Key strategies adopted by companies in the 3D Printing Plastics Market include heavy investment in research and development to create high-performance and application-specific materials with improved mechanical and thermal properties. Firms are expanding their product portfolios to include advanced composite and multi-material solutions that cater to industrial-grade applications. Strategic partnerships with end-use industries such as aerospace, healthcare, and automotive are helping companies strengthen application-specific customization capabilities. Manufacturers are also focusing on scaling production capacity and optimizing supply chains to meet rising global demand efficiently. Adoption of sustainable and recyclable plastic formulations is gaining traction as environmental regulations tighten. In addition, companies are leveraging digital manufacturing platforms, software integration, and AI-driven design tools to enhance precision, reduce material waste, and improve production efficiency, thereby strengthening their competitive position in the rapidly evolving additive manufacturing ecosystem.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastics

- 5.2.1 Acrylonitrile Butadiene Styrene (ABS)

- 5.2.2 Polylactic Acid (PLA)

- 5.2.3 Polyamide (Nylon)

- 5.2.4 Polyetheretherketone (PEEK)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyethylene Terephthalate Glycol (PETG)

- 5.2.7 Polyphenylsulfone (PPSU)

- 5.2.8 Others (TPU, PPS, PEI)

- 5.3 Photopolymers

- 5.3.1 Standard Resins

- 5.3.2 Tough/Durable Resins

- 5.3.3 Flexible Resins

- 5.3.4 High-Temperature Resins

- 5.3.5 Biocompatible Resins

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Filament

- 6.2.1 Standard Diameter (1.75mm)

- 6.2.2 Large Diameter (2.85mm & Above)

- 6.3 Powder

- 6.3.1 Fine Particle (< 50 microns)

- 6.3.2 Medium Particle (50-100 microns)

- 6.4 Liquid/Resin

- 6.4.1 UV-Curable Resins

- 6.4.2 Thermal-Curable Resins

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 Interior Components

- 7.2.2 Exterior Components

- 7.2.3 Powertrain Components

- 7.2.4 Tooling & Fixtures

- 7.3 Aerospace & Defense

- 7.3.1 Aircraft Interior Components

- 7.3.2 Structural Components

- 7.3.3 UAV & Drone Applications

- 7.3.4 Tooling & Jigs

- 7.4 Healthcare

- 7.4.1 Medical Devices

- 7.4.2 Prosthetics & Orthotics

- 7.4.3 Dental Applications

- 7.4.4 Surgical Planning & Anatomical Models

- 7.5 Consumer Goods

- 7.5.1 Footwear

- 7.5.2 Eyewear

- 7.5.3 Toys & Games

- 7.5.4 Sporting Goods

- 7.5.5 Home Products

- 7.6 Industrial Manufacturing

- 7.6.1 Production Tooling

- 7.6.2 Jigs & Fixtures

- 7.6.3 End-of-Arm Tooling

- 7.6.4 Functional Prototypes

- 7.7 Others

- 7.7.1 Architecture & Construction

- 7.7.2 Education & Research

- 7.7.3 Electronics

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Stratasys Ltd.

- 9.2 3D Systems, Inc.

- 9.3 Formlabs

- 9.4 Arkema S.A.

- 9.5 Evonik Industries AG

- 9.6 EOS GmbH

- 9.7 SABIC

- 9.8 Henkel AG & Co. KGaA

- 9.9 Materialise NV

- 9.10 Shenzhen eSUN

3D列印塑膠市場:2026-2032年全球市場預測(依塑膠類型、形狀、列印技術、應用、終端用戶產業和分銷管道分類)

3D列印塑膠市場:2026-2032年全球市場預測(依塑膠類型、形狀、列印技術、應用、終端用戶產業和分銷管道分類) 3D列印塑膠市場報告:按類型、形式、應用、最終用戶和地區分類(2026-2034年)

3D列印塑膠市場報告:按類型、形式、應用、最終用戶和地區分類(2026-2034年) 高性能3D列印塑膠市場規模、佔有率和成長分析:按材料類型、形狀、列印技術、應用、終端用戶產業、特性類型和地區分類-2026-2033年產業預測

高性能3D列印塑膠市場規模、佔有率和成長分析:按材料類型、形狀、列印技術、應用、終端用戶產業、特性類型和地區分類-2026-2033年產業預測 3D列印塑膠市場規模、佔有率和趨勢分析報告:按類型、形式、最終用途、地區和細分市場分類(2026-2033年)高性能塑膠3D列印市場:按材料類型、形狀、列印技術、應用和最終用途產業分類,全球預測(2026-2032)

3D列印塑膠市場規模、佔有率和趨勢分析報告:按類型、形式、最終用途、地區和細分市場分類(2026-2033年)高性能塑膠3D列印市場:按材料類型、形狀、列印技術、應用和最終用途產業分類,全球預測(2026-2032) 高性能3D列印塑膠市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶及組件分類

高性能3D列印塑膠市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶及組件分類 高性能聚合物3D列印材料市場:依類型、形態、技術和終端應用產業劃分-全球預測至2036年

高性能聚合物3D列印材料市場:依類型、形態、技術和終端應用產業劃分-全球預測至2036年 全球高性能3D列印塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球高性能3D列印塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球3D列印塑膠市場報告

2026年全球3D列印塑膠市場報告 3D列印塑膠市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、形狀、應用、終端用戶產業、地區和競爭格局分類,2021-2031年

3D列印塑膠市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、形狀、應用、終端用戶產業、地區和競爭格局分類,2021-2031年