|

市場調查報告書

商品編碼

2038482

汽車市場機會、成長要素、產業趨勢分析及2026-2035年預測。Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

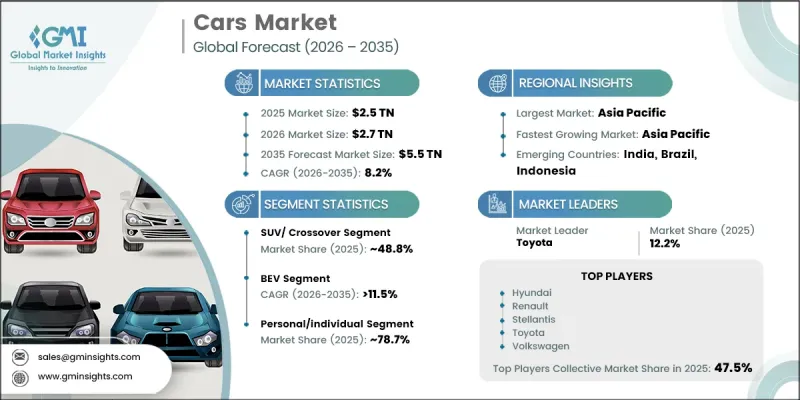

2025年全球汽車市場價值為2.5兆美元,預計將以8.2%的複合年成長率成長,到2035年達到5.5兆美元。

全球都市化加快、可支配收入增加以及消費者對個人出行方式偏好的持續轉變,是推動市場成長的主要因素。中產階級的壯大是汽車市場成長的主要動力,尤其是在消費者從共享交通和摩托車轉向私家車之後。購買力的提升也推動了對豪華和功能豐富的車型的需求。同時,隨著產業重心轉向電氣化和永續出行,汽車產業正經歷結構性轉型。日益增強的環保意識加速了人們對低排放氣體汽車的興趣,而更嚴格的排放氣體法規迫使製造商轉向更清潔的技術。車輛設計、安全系統和連網功能的持續創新進一步提升了產品的吸引力。政府的獎勵和支持性政策框架也在促進已開發市場和新興市場採用先進的出行解決方案方面發揮著至關重要的作用,從而加速了市場擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2.5兆美元 |

| 預測金額 | 5.5兆美元 |

| 複合年成長率 | 8.2% |

SUV和跨界車細分市場佔據48.8%的市場佔有率,預計到2025年銷售額將達到1.2兆美元。消費者對這類車款的需求持續強勁成長,它們仍然是家庭用車和日常通勤的首選。雖然緊湊型和中型車型的銷售量最大,但高階車型對整體盈利的貢獻也十分顯著。最初應用於高階車型的功能和技術正擴大被應用到中階車型中,這不僅重新定義了各細分市場消費者的期望,也提升了產品的整體競爭力。

預計2026年至2035年,豪華車和高階車市場將以9.2%的複合年成長率成長。可支配收入的成長是推動這一成長的主要動力,尤其是在已開發市場,消費者購買力的提升尤為顯著。中產階級和中上階級購買力的增強,推動了對性能卓越、技術先進的豪華車的需求。這種轉變反映出汽車產業對舒適性、創新性和品牌價值的日益重視。

美國汽車市場預計到2025年將達到1,853億美元,並在2026年至2035年間以8.2%的複合年成長率成長。美國仍然是全球最大的汽車市場之一,這得益於消費者對傳統汽車和電動車的強勁需求。市場擴張的促進因素包括收入水準的提高、消費者對SUV和皮卡的強烈偏好,以及混合動力汽車汽車和電動車的日益普及。旨在推廣更清潔交通途徑的支持和獎勵進一步促進了向電動出行的轉型。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 新興國家可支配所得增加

- 政府對電動車的獎勵與補貼

- 共乘與交通行動服務(MaaS) 的擴展

- 新興市場中產階級的成長

- 產業潛在風險與挑戰

- 汽車零件供應鏈中斷

- 電動車和先進車輛的初始成本很高

- 市場機遇

- 電動車和混合動力汽車的廣泛應用

- 自動駕駛汽車技術的發展

- 推廣永續和環保製造方法

- 促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 動力傳動系統技術

- ADAS和安全技術

- 連接和資訊娛樂系統

- 新興技術

- 下一代電池技術

- 自動駕駛技術

- 車聯網(V2X)通訊

- 目前技術

- 成長潛力分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 監理情勢

- 北美洲

- 美國-企業平均燃油經濟性(CAFE)標準

- 美國—《清潔空氣法》下的汽車排放氣體標準

- 加拿大 - 加拿大運輸部

- 歐洲

- 德國 - 歐6/歐7排放氣體標準

- 歐盟WLTP(全球輕型車輛測試程序)

- 亞太地區

- 中國—強制性新能源汽車政策

- 印度 - BS-VI排放氣體法規

- 拉丁美洲

- 巴西 - PROCONVE排放氣體法規計劃

- 墨西哥-NOM-163燃油消耗標準

- 中東和非洲

- 沙烏地阿拉伯 - SASO 車輛安全和排放氣體標準

- 阿拉伯聯合大公國-綠色車輛舉措相關法規

- 北美洲

- 波特五力分析

- PESTEL 分析

- 專利分析(基於初步研究)

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的已安裝產能

- 設備運轉率和擴建計劃

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 成本細分分析

- 直接材料採購成本

- 生產和組裝的成本

- 人工人事費用費用

- 間接成本和設施成本

- 合規、品質和保證成本

- 目前電動車充電基礎設施狀況

- 公共充電網路與私人充電網路

- 充電速度技術的演進

- 家用充電解決方案及其普及障礙

- 職場和目的地充電業務的成長

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 掀背車

- 轎車

- SUV/跨界車

- 小轎車

- MPV

- 其他

第6章 市場估計與預測:依實施法分類,2022-2035年

- 內燃機(ICE)

- 混合動力電動車(HEV)

- 電池式電動車(BEV)

- 燃料電池汽車(FCEV)

- 插電式混合動力汽車(PHEV)

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 經濟型/入門級

- 中產階級

- 豪華/高級

第8章 市場估計與預測:依輸電類型分類,2022-2035年

- 手排變速箱

- 自動變速箱

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 個人使用

- 商業的

- 企業用車

- 汽車租賃服務

- 企業用車

- 政府和公共部門車輛

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 波蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 泰國

- 馬來西亞

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Toyota Motor

- Volkswagen

- Hyundai Motor

- Ford Motor

- General Motors(GM)

- Stellantis

- Honda Motor

- Renault

- BMW

- Mercedes-Benz

- 當地公司

- Maruti Suzuki

- Tata Motors Passenger Vehicles

- Mahindra & Mahindra

- SAIC Motor

- BAIC

- Tesla

- Chery Automobile

- 新興企業

- BYD Auto

- XPeng

- Li Auto

The Global Cars Market was valued at USD 2.5 trillion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 5.5 trillion by 2035.

Market growth is driven by rising global urbanization, increasing disposable incomes, and a steady shift in consumer preference toward personal mobility solutions. Expanding middle-class populations are significantly contributing to higher automobile adoption, particularly as consumers transition away from shared and two-wheeler transport options toward private vehicle ownership. Improved financial capacity is also enabling stronger demand for premium and feature-rich vehicles. At the same time, the automotive sector is undergoing a structural transformation with growing emphasis on electrification and sustainable mobility. Increasing awareness of environmental concerns is accelerating interest in low-emission vehicles, while stricter emission regulations are pushing manufacturers toward cleaner technologies. Continuous innovation in vehicle design, safety systems, and connectivity features is further enhancing product appeal. Government-backed incentives and supportive policy frameworks are also playing a key role in accelerating market expansion by encouraging the adoption of advanced mobility solutions across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Trillion |

| Forecast Value | $5.5 Trillion |

| CAGR | 8.2% |

The SUV and crossover segment held a 48.8% share, generating USD 1.2 trillion in 2025. Demand continues to shift strongly toward these vehicle types, as they remain the preferred choice for both family and everyday commuting needs. Compact and mid-size models account for the highest sales volumes, while premium variants contribute significantly to overall profitability. Features and technologies initially introduced in high-end models are increasingly being integrated into mid-tier offerings, reshaping consumer expectations across segments and enhancing overall product competitiveness.

The luxury and premium segment is projected to grow at a CAGR of 9.2% from 2026 to 2035. Rising disposable income levels are a major factor supporting this growth, particularly as consumers in developed markets gain greater purchasing power. Increasing financial capacity among middle and upper-middle income groups is driving higher demand for luxury vehicles equipped with advanced performance capabilities and modern technologies. This shift reflects a growing preference for comfort, innovation, and brand value within the automotive sector.

United States Cars Market reached USD 185.3 billion in 2025 and is expected to grow at a CAGR of 8.2% between 2026 and 2035. The country remains one of the largest automotive markets globally, supported by strong consumer demand for both conventional vehicles and electric models. Market expansion is influenced by rising income levels, strong preference for SUVs and pickup vehicles, and increasing adoption of hybrid and electric cars. The transition toward electric mobility is further reinforced by supportive policy measures and incentives aimed at encouraging cleaner transportation solutions.

Key companies operating in the Global Cars Industry include Toyota, Volkswagen, Ford, Hyundai, GM, Honda, BYD, Stellantis, Renault, and Suzuki. Companies in the Global Cars Market are strengthening their competitive position through rapid electrification strategies, investment in advanced vehicle technologies, and expansion of global production capabilities. Automakers are focusing on developing electric and hybrid models to align with tightening emission standards and rising environmental awareness. Strong emphasis is being placed on research and development to enhance battery performance, vehicle range, and autonomous driving features. Strategic partnerships with technology firms are helping accelerate innovation in connected and smart mobility solutions. Manufacturers are also expanding their dealership and distribution networks to improve market reach. Cost optimization, platform sharing, and localized production are being adopted to improve profitability while meeting diverse regional demand patterns across global automotive markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Vehicle class

- 2.2.5 Transmission

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing disposable income in emerging economies

- 3.2.1.2 Government incentives and subsidies for electric vehicles

- 3.2.1.3 Expansion of ride-sharing and mobility-as-a-service (MaaS)

- 3.2.1.4 Growing middle-class population in the emerging markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions in automotive components

- 3.2.2.2 High initial cost of electric and advanced vehicles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in electric and hybrid vehicle adoption

- 3.2.3.2 Development of autonomous vehicle technology

- 3.2.3.3 Expansion of sustainable and green manufacturing practices

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Powertrain technology

- 3.3.1.2 ADAS & safety technology

- 3.3.1.3 Connectivity & infotainment system

- 3.3.2 Emerging technologies

- 3.3.2.1 Next-generation battery technology

- 3.3.2.2 Autonomous driving technology

- 3.3.2.3 Vehicle-to-everything (V2X) communication

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - Corporate Average Fuel Economy (CAFE) Standards

- 3.6.1.2 US - Clean Air Act Vehicle Emission Standards

- 3.6.1.3 Canada - Transport Canada

- 3.6.2 Europe

- 3.6.2.1 Germany - Euro 6 / Euro 7 Emission Standards

- 3.6.2.2 EU - WLTP (Worldwide Harmonized Light Vehicles Test Procedure)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - New Energy Vehicle (NEV) Mandate Policy

- 3.6.3.2 India - BS-VI Emission Standards

- 3.6.4 Latin America

- 3.6.4.1 Brazil - PROCONVE Emission Control Program

- 3.6.4.2 Mexico - NOM-163 Fuel Economy Standards

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Arabia - SASO Vehicle Safety and Emission Standards

- 3.6.5.2 UAE - Green Vehicle Initiative Regulations

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

- 3.13 Cost breakdown analysis

- 3.13.1 Direct Material Procurement Cost

- 3.13.2 Production & Assembly Line Cost

- 3.13.3 Labor & Workforce Cost

- 3.13.4 Overhead & Facility Cost

- 3.13.5 Compliance, Quality & Warranty Cost

- 3.14 EV charging infrastructure landscape

- 3.14.1 Public vs Private charging networks

- 3.14.2 Charging speed technology evolution

- 3.14.3 Home charging solutions & adoption barriers

- 3.14.4 Workplace & destination charging growth

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022- 2035 ($Bn, Thousand Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV/ Crossover

- 5.5 Coupe

- 5.6 MPV

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022- 2035 ($Bn, Thousand Units)

- 6.1 Key trends

- 6.2 Internal Combustion Engine (ICE)

- 6.3 Hybrid Electric Vehicles (HEV)

- 6.4 Battery Electric Vehicles (BEV)

- 6.5 Fuel Cell Electric Vehicles (FCEV)

- 6.6 Plug-in Hybrid Electric Vehicles (PHEV)

Chapter 7 Market Estimates & Forecast, By Vehicle class, 2022- 2035 ($Bn, Thousand Units)

- 7.1 Key trends

- 7.2 Economy/Entry level

- 7.3 Mid-range

- 7.4 Luxury/Premium

Chapter 8 Market Estimates & Forecast, By Transmission, 2022- 2035 ($Bn, Thousand Units)

- 8.1 Key trends

- 8.2 Manual Transmission

- 8.3 Automatic Transmission

Chapter 9 Market Estimates & Forecast, By End Use, 2022- 2035 ($Bn, Thousand Units)

- 9.1 Key trends

- 9.2 Personal/Individual Use

- 9.3 Commercial

- 9.3.1 Corporate fleet

- 9.3.2 Rental car services

- 9.3.3 Corporate fleet

- 9.3.4 Government/public sector fleet

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Sweden

- 10.3.8 Poland

- 10.3.9 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Thailand

- 10.4.8 Malaysia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Toyota Motor

- 11.1.2 Volkswagen

- 11.1.3 Hyundai Motor

- 11.1.4 Ford Motor

- 11.1.5 General Motors (GM)

- 11.1.6 Stellantis

- 11.1.7 Honda Motor

- 11.1.8 Renault

- 11.1.9 BMW

- 11.1.10 Mercedes-Benz

- 11.2 Regional players

- 11.2.1 Maruti Suzuki

- 11.2.2 Tata Motors Passenger Vehicles

- 11.2.3 Mahindra & Mahindra

- 11.2.4 SAIC Motor

- 11.2.5 BAIC

- 11.2.6 Tesla

- 11.2.7 Chery Automobile

- 11.3 Emerging players

- 11.3.1 BYD Auto

- 11.3.2 XPeng

- 11.3.3 Li Auto

印度乘用車:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度乘用車:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 印度乘用車市場成長機會:2026-2032年

印度乘用車市場成長機會:2026-2032年 智慧交通控制市場預測至2034年-按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析

智慧交通控制市場預測至2034年-按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析 車輛即服務 (VaaS) 市場規模、佔有率和成長分析:按服務類型、車輛類型、最終用戶和地區分類-2026-2033 年產業預測

車輛即服務 (VaaS) 市場規模、佔有率和成長分析:按服務類型、車輛類型、最終用戶和地區分類-2026-2033 年產業預測 乘用車市場規模、佔有率和成長分析:按燃料類型、車輛類型、分銷管道和地區分類-2026-2033年產業預測

乘用車市場規模、佔有率和成長分析:按燃料類型、車輛類型、分銷管道和地區分類-2026-2033年產業預測 2026年全球乘用車市場報告VaaS(車輛即服務)市場全球市場報告(2026年)2026-2034年全球乘用車智慧轉向系統市場規模、佔有率、趨勢及成長分析報告

2026年全球乘用車市場報告VaaS(車輛即服務)市場全球市場報告(2026年)2026-2034年全球乘用車智慧轉向系統市場規模、佔有率、趨勢及成長分析報告 乘用車廢氣排放系統市場-全球產業規模、佔有率、趨勢、機會及預測(依燃料類型、後處理類型、零件類型、地區及競爭格局分類,2021-2031年)乘用車拖車桿市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、地區和競爭格局分類,2021-2031年

乘用車廢氣排放系統市場-全球產業規模、佔有率、趨勢、機會及預測(依燃料類型、後處理類型、零件類型、地區及競爭格局分類,2021-2031年)乘用車拖車桿市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、地區和競爭格局分類,2021-2031年