|

市場調查報告書

商品編碼

2038454

火砲系統市場機會、成長要素、產業趨勢分析及2026-2035年預測。Artillery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

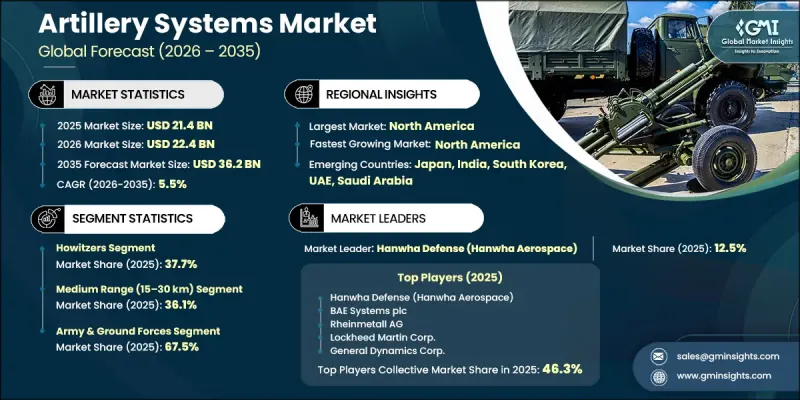

預計到 2025 年,全球火砲系統市場價值將達到 214 億美元,並預計以 5.5% 的複合年成長率成長,到 2035 年達到 362 億美元。

市場成長的驅動力來自國防現代化建設的不斷推進以及軍事技術研發領域國際合作的加強。各國政府和國防製造商正日益積極參與聯合計畫、夥伴關係並簽署技術共用協議,以加速先進火砲解決方案的研發。這些合作有助於降低研發成本、提高創新效率並縮短下一代系統的生產週期。日益加劇的地緣政治緊張局勢和不斷演變的作戰場景也推動了對更先進、更具適應性的火砲平台的需求。向高機動性、高精度和技術驅動型武器系統的轉變進一步影響各國國防部隊的籌資策略。此外,非對稱戰爭的威脅正在重塑作戰需求,更加強調火砲的靈活性和快速反應能力。持續的研發投入,以及多國開展的現代化項目,正在推動市場的長期擴張並增強全球防禦態勢。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 214億美元 |

| 預測金額 | 362億美元 |

| 複合年成長率 | 5.5% |

截至2025年,榴彈砲市佔率將達到37.7%。該細分市場需求強勁,這得益於其作戰柔軟性、遠射程能力以及在各種作戰環境中的有效性。隨著目標捕獲精度、自動化程度和機動性的不斷提升,榴彈砲被廣泛應用於進攻和防禦任務。這些改進增強了其在現代戰場作戰中的重要性,並使其保持市場主導地位。

預計到2025年,中程(15-30公里)飛彈將佔據36.1%的市場。此細分市場持續成長,得益於其均衡的性能特點,兼具射程、精度和戰術性效能。其對各種軍事行動的適應性使其能夠滿足廣泛的任務需求。該細分市場在各種作戰環境下的高效用,促使其被世界各國的國防部隊穩步採用。

到2025年,北美火砲系統市佔率將達到35.7%。該地區的領先地位得益於先進的國防基礎設施、強大的技術能力以及政府對軍事現代化項目的持續投入。下一代火砲平台(包括射程和精度更高的系統)的持續研發正在推動採購活動。主要國防製造商的積極參與進一步鞏固了該地區在全球市場的地位,並支持火砲技術的持續進步。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加強國防領域的合作

- 非對稱戰爭正在增加。

- 網路中心戰的採用

- 增強機動性和部署能力

- 重點發展國內國防生產

- 產業潛在風險與挑戰

- 監理和合規挑戰

- 供應鏈中斷

- 市場機遇

- 精確導引火砲系統的擴展

- 發展中地區國防現代化計畫的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依系統類型分類,2022-2035年

- 榴彈砲

- 牽引式榴彈砲

- 自走榴彈炮

- 輪式自走榴彈炮

- 其他

- 砂漿

- 輕砂漿(小於100毫米)

- 中口徑迫擊砲(100毫米-120毫米)

- 重型迫擊砲(直徑超過120毫米)

- 火箭發射器

- 多管火箭系統(MLRS)

- 導引火箭發射器

- 無導火箭發射器

- 高射砲

- 短程防空砲

- 中程防空砲

- 其他

第6章 市場估計與預測:依平台分類,2022-2035年

- 牽引砲

- 輕型牽引系統

- 中型牽引系統

- 重型牽引系統

- 自走炮

- 履帶式自走炮

- 輪式自走自走炮

- 兩棲自走炮

- 海軍大砲

- 水面艦砲

- 海岸防禦系統

- 電磁砲

第7章 市場估計與預測:依範圍分類,2022-2035年

- 短距離(15公里或更短)

- 中距離(15-30公里)

- 長途(超過30公里)

第8章 市場估算與預測:依組件分類,2022-2035年

- 槍械系統

- 消防系統

- 彈藥

- 支援系統

第9章 市場估計與預測:依口徑分類,2022-2035年

- 小直徑(小於100毫米)

- 中等直徑(100毫米至155毫米)

- 大直徑(超過155毫米)

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- 陸軍和地面部隊

- 裝甲旅戰鬥隊

- 步兵師

- 其他

- 海軍

- 水面作戰艦艇

- 海岸防禦部隊

- 其他

- 防空部隊

- 一體化防空系統

- 機動防空部隊

- 其他

- 邊防安全/準軍事部隊

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- 世界公司

- BAE Systems plc

- Lockheed Martin Corporation

- Rheinmetall AG

- Hanwha Defense

- Nexter Systems(KNDS Group)

- General Dynamics Corporation

- Elbit Systems Ltd.

- 該地區的領先企業

- Bharat Forge Limited(Kalyani Group)

- PT Pindad(Indonesia)

- Denel SOC Ltd.(South Africa)

- 新興企業

- Military Industry Corporation(Iraq)

- Yugoimport SDPR(Serbia)

The Global Artillery Systems Market was valued at USD 21.4 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 36.2 billion by 2035.

Market growth is supported by increasing defense modernization initiatives and stronger international collaboration in military technology development. Governments and defense manufacturers are increasingly engaging in joint programs, partnerships, and technology-sharing agreements to accelerate the development of advanced artillery solutions. These collaborations help reduce development costs, improve innovation efficiency, and shorten production timelines for next-generation systems. Rising geopolitical tensions and evolving combat scenarios are also pushing demand for more advanced and adaptable artillery platforms. The shift toward highly mobile, precise, and technology-enabled weapon systems is further influencing procurement strategies across defense forces. Additionally, asymmetric warfare threats are reshaping operational requirements, leading to greater emphasis on flexible and responsive artillery capabilities. Continuous investment in research and development, combined with modernization programs across multiple countries, is reinforcing long-term market expansion and strengthening global defense readiness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.4 Billion |

| Forecast Value | $36.2 Billion |

| CAGR | 5.5% |

The howitzers segment accounted for 37.7% share in 2025. This segment maintains strong demand due to its operational flexibility, extended range capabilities, and effectiveness across multiple combat environments. It is widely used for both offensive and defensive missions, supported by continuous advancements in targeting precision, automation, and mobility. These improvements have strengthened its relevance in modern battlefield operations and sustained its leadership position within the market.

The medium-range (15-30 km) segment held 36.1% share in 2025. This segment continues to grow due to its balanced performance characteristics, offering a combination of range, accuracy, and tactical efficiency. Its adaptability across diverse military operations makes it suitable for a wide range of mission requirements. The segment's strong operational utility in varied combat conditions is contributing to its steady adoption across defense forces globally.

North America Artillery Systems Market accounted for 35.7% share in 2025. The region's dominance is supported by advanced defense infrastructure, strong technological capabilities, and sustained government investment in military modernization programs. Continuous development of next-generation artillery platforms, including systems with enhanced range and precision capabilities, is driving procurement activity. Strong participation from leading defense manufacturers further strengthens the region's position in the global market and supports ongoing advancements in artillery technology.

Key companies operating in the Global Artillery Systems Market include Lockheed Martin Corporation, BAE Systems plc, Rheinmetall AG, Hanwha Defense, Nexter Systems (KNDS Group), General Dynamics Corporation, and Elbit Systems Ltd. Companies in the Artillery Systems Market are focusing on technological innovation, strategic partnerships, and defense collaboration agreements to strengthen their competitive position. Significant investments are being directed toward research and development to enhance system accuracy, mobility, and automation capabilities. Firms are actively engaging in joint ventures and international defense programs to share expertise and reduce development costs. Expansion of production capacities and modernization of manufacturing facilities are also key priorities to meet rising demand. Additionally, companies are integrating advanced digital systems, including fire control technologies and precision-guided solutions, to improve operational efficiency. Strengthening long-term government contracts and expanding global defense networks are further supporting sustained market positioning and growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Platform trends

- 2.2.3 Range trends

- 2.2.4 Component trends

- 2.2.5 Caliber trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased defense collaboration

- 3.2.1.2 Rising asymmetric warfare

- 3.2.1.3 Adoption of network-centric warfare

- 3.2.1.4 Enhanced mobility and deployment

- 3.2.1.5 Focus on indigenous defense production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and compliance issues

- 3.2.2.2 Supply chain disruptions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of precision-guided artillery systems

- 3.2.3.2 Growth in defense modernization programs in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.11.1 Historical Price Trend Analysis

- 3.11.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.12 Trade Data Analysis (Based on Paid Database)

- 3.12.1 Import/Export Volume & Value Trends

- 3.12.2 Key Trade Corridors & Tariff Impact

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Production Capacity by Region & Key Producer

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Howitzers

- 5.2.1 Towed howitzers

- 5.2.2 Self-propelled howitzers

- 5.2.3 Wheeled self-propelled howitzers

- 5.2.4 Others

- 5.3 Mortars

- 5.3.1 Light mortars (below 100mm)

- 5.3.2 Medium mortars (100mm-120mm)

- 5.3.3 Heavy mortars (above 120mm)

- 5.4 Rocket artillery

- 5.4.1 Multiple launch rocket systems (MLRS)

- 5.4.2 Guided rocket artillery

- 5.4.3 Unguided rocket artillery

- 5.5 Anti-aircraft guns

- 5.5.1 Short-range air defense (SHORAD) artillery

- 5.5.2 Medium-range air defense artillery

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Towed artillery

- 6.2.1 Lightweight towed systems

- 6.2.2 Medium towed systems

- 6.2.3 Heavy towed systems

- 6.3 Self-propelled artillery

- 6.3.1 Tracked self-propelled

- 6.3.2 Wheeled self-propelled

- 6.3.3 Amphibious self-propelled

- 6.4 Naval artillery

- 6.4.1 Surface vessel artillery

- 6.4.2 Coastal defense systems

- 6.5 Rail-based artillery

Chapter 7 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Short range (up to 15 km)

- 7.3 Medium range (15-30 km)

- 7.4 Long range (above 30 km)

Chapter 8 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Gun system

- 8.3 Fire control system

- 8.4 Ammunition

- 8.5 Auxiliary systems

Chapter 9 Market Estimates and Forecast, By Caliber, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Small caliber (below 100mm)

- 9.3 Medium caliber (100mm-155mm)

- 9.4 Large caliber (above 155mm)

Chapter 10 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Army & ground forces

- 10.2.1 Armored brigade combat teams

- 10.2.2 Infantry divisions

- 10.2.3 Others

- 10.3 Naval forces

- 10.3.1 Surface warfare vessels

- 10.3.2 Coastal defense units

- 10.3.3 Others

- 10.4 Air defense forces

- 10.4.1 Integrated air defense systems

- 10.4.2 Mobile air defense units

- 10.4.3 Others

- 10.5 Border security & paramilitary

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.3.7 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 BAE Systems plc

- 12.1.2 Lockheed Martin Corporation

- 12.1.3 Rheinmetall AG

- 12.1.4 Hanwha Defense

- 12.1.5 Nexter Systems (KNDS Group)

- 12.1.6 General Dynamics Corporation

- 12.1.7 Elbit Systems Ltd.

- 12.2 Regional Champions

- 12.2.1 Bharat Forge Limited (Kalyani Group)

- 12.2.2 PT Pindad (Indonesia)

- 12.2.3 Denel SOC Ltd. (South Africa)

- 12.3 Emerging Players

- 12.3.1 Military Industry Corporation (Iraq)

- 12.3.2 Yugoimport SDPR (Serbia)

火砲系統市場:2026-2032年全球市場預測(依系統類型、組件、射程、口徑、平台及最終用戶分類)

火砲系統市場:2026-2032年全球市場預測(依系統類型、組件、射程、口徑、平台及最終用戶分類) 2026-2036年全球105毫米彈藥市場:全球火砲系統市場(2026-2036 年)

2026-2036年全球105毫米彈藥市場:全球火砲系統市場(2026-2036 年) 2026年全球火砲系統市場報告

2026年全球火砲系統市場報告 全球火砲系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球火砲系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 火砲系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、射程、區域和競爭格局分類,2021-2031年

火砲系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、射程、區域和競爭格局分類,2021-2031年 迫擊炮系統的全球市場:各類型,各零件,射程距離,各地區,機會,預測,2018年~2032年

迫擊炮系統的全球市場:各類型,各零件,射程距離,各地區,機會,預測,2018年~2032年 火砲系統市場規模、佔有率及成長分析(按類型、子系統、範圍和地區)-2025-2032 年產業預測

火砲系統市場規模、佔有率及成長分析(按類型、子系統、範圍和地區)-2025-2032 年產業預測 炮兵系統的全球市場:市場規模,趨勢的分析,市場區隔,主要計劃,競爭情形,預測(2024年~2034年)

炮兵系統的全球市場:市場規模,趨勢的分析,市場區隔,主要計劃,競爭情形,預測(2024年~2034年) 火砲系統市場規模、佔有率、趨勢分析報告:按距離、按組件、按類型、按地區、細分市場預測,2024-2030 年

火砲系統市場規模、佔有率、趨勢分析報告:按距離、按組件、按類型、按地區、細分市場預測,2024-2030 年