|

市場調查報告書

商品編碼

2038400

主電源固定式燃料電池市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Prime Power Stationary Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

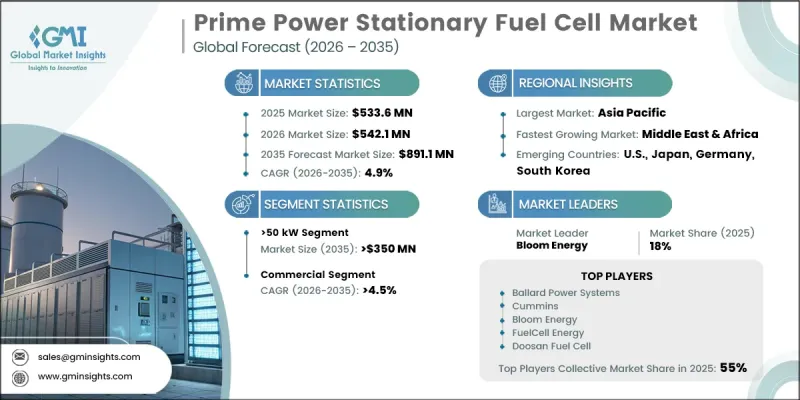

預計到 2025 年,全球用於主電源的固定式燃料電池市值為 5.336 億美元,並將以 4.9% 的複合年成長率成長,到 2035 年達到 8.911 億美元。

市場擴張的驅動力在於對可靠的、獨立於傳統電網基礎設施運作的現場發電系統的需求不斷成長。這些燃料電池系統專為連續運作而設計,並日益被各行各業廣泛採用為主要電力源。不斷成長的電力需求正在加速工業和商業環境中分散式能源解決方案的普及。早期商業化措施和先導計畫正在推動其融入更廣泛的清潔能源和分散式電力生態系統。醫療機構、資料中心、製造工廠和大型商業建築等設施正在部署這些系統,以提高電力可靠性、降低停機風險並最大限度地減少對集中式電網的依賴。固體氧化物燃料電池和熔融碳酸鹽燃料電池的技術進步,憑藉其高效率、燃料柔軟性和適用於連續負載運行的特性,進一步促進了市場普及。偏遠地區能源需求的成長以及人們對替代能源日益成長的興趣也推動了市場成長。此外,公共和私人對氫能基礎設施的支持性投資正在加速產業發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 5.336億美元 |

| 預測金額 | 8.911億美元 |

| 複合年成長率 | 4.9% |

預計到2035年,功率超過50kW的細分市場規模將達到3.5億美元。此細分市場的需求主要來自商業和輕工業應用領域對緊湊型高容量電力系統的需求。這些系統能夠在現場提供穩定的電力供應,同時保持高效率和低排放。分散式能源模式的日益普及以及向綠能技術的轉型,進一步推動了該細分市場的成長。

預計到2035年,商業領域的複合年成長率將達到4.5%。對可靠綠能解決方案的需求不斷成長,推動了辦公大樓、醫療機構、零售商店和資料中心等商業建築對燃料電池的採用。受向低排放能源來源轉型趨勢的推動,各組織正在投資基於燃料電池的主電源系統,以確保業務連續性並降低電網不穩定的風險。

預計2035年,美國主電源固定式燃料電池市場規模將達3,500萬美元。這一成長主要得益於商業和工業領域對容錯性強、低排放發電解決方案的需求不斷成長。各組織機構正擴大採用燃料電池系統,以確保業務連續性,並減少對老舊電網基礎設施的依賴。各州的支持政策和不斷擴大的氫能相關舉措,進一步加速了燃料電池在製造工廠、醫療中心和數據基礎設施等關鍵應用領域的普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 成本結構分析

- 價格趨勢分析,2022-2035年

- 按最終用途

- 按地區

- 新機會與趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析(按國家/地區)

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依產能分類,2022-2035年

- 小於3千瓦

- 3~10 kW

- 10~50 kW

- 超過50千瓦

第6章 市場規模與預測:依最終用途分類,2022-2035年

- 住宅

- 商業的

- 工業和公共產業

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 奧地利

- 亞太地區

- 日本

- 韓國

- 中國

- 印度

- 菲律賓

- 越南

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 拉丁美洲

- 巴西

- 秘魯

- 墨西哥

第8章:公司簡介

- Ballard Power Systems

- Bloom Energy

- Cummins

- Doosan Corporation

- FCT Energy

- Frost and Sullivan

- Fuel Cell Energy

- Fuji Electric

- GenCell

- HDF Energy

- Honda Motor

- Hunter New Energy

- Hyundai Motor

- Hyzon Motors

- Intelligent Energy

- Nedstack Fuel Cell Technology

- NUVERA FUEL CELLS

- Plug Power

- Robert Bosch GmbH

- SFC Energy

The Global Prime Power Stationary Fuel Cell Market was valued at USD 533.6 million in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 891.1 million by 2035.

Market expansion is driven by the rising need for dependable, on-site power generation systems that operate independently of traditional grid infrastructure. These fuel cell systems are designed for continuous operation and are increasingly being adopted as primary electricity sources across multiple sectors. Growing electricity demand is encouraging the deployment of distributed energy solutions across industrial and commercial environments. Early commercialization efforts and pilot projects are supporting integration into broader clean energy and decentralized power ecosystems. Facilities such as healthcare institutions, data centers, manufacturing units, and large commercial properties are adopting these systems to improve power reliability, reduce downtime risks, and minimize dependence on centralized grids. Technological advancements in solid oxide and molten carbonate fuel cells are further supporting market adoption due to their high efficiency, fuel flexibility, and suitability for continuous load operations. Rising energy needs in remote areas, coupled with increasing interest in alternative energy sources, are also contributing to market growth. Additionally, supportive public and private investments in hydrogen infrastructure are accelerating industry development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $533.6 Million |

| Forecast Value | $891.1 Million |

| CAGR | 4.9% |

The above 50 kW segment is expected to reach USD 350 million by 2035. Demand in this category is being driven by the need for compact yet high-capacity power systems across commercial and light industrial applications. These systems provide consistent on-site electricity while maintaining high efficiency and low emissions. Growing adoption of decentralized energy models and the transition toward cleaner power technologies are further strengthening segment growth.

The commercial segment is projected to grow at a CAGR of 4.5% through 2035. Increasing demand for reliable and clean power solutions is encouraging adoption across commercial buildings, including offices, healthcare facilities, retail spaces, and data centers. The need for uninterrupted operations and reduced exposure to grid instability is prompting organizations to invest in fuel cell-based prime power systems, supported by the broader shift toward low-emission energy sources.

U.S. Prime Power Stationary Fuel Cell Market is anticipated to reach USD 35 million by 2035. Growth is being driven by rising demand for resilient and low-emission power generation solutions across commercial and industrial sectors. Organizations are increasingly adopting fuel cell systems to ensure uninterrupted operations and reduce dependence on aging grid infrastructure. Supportive state-level policies and expanding hydrogen initiatives are further accelerating deployment across key application areas, including manufacturing facilities, healthcare centers, and data infrastructure.

Key companies operating in the Global Prime Power Stationary Fuel Cell Market include Bloom Energy, Plug Power, Ballard Power Systems, Fuel Cell Energy, Cummins, Hyundai Motor, Doosan Corporation, Fuji Electric, Robert Bosch GmbH, SFC Energy, Nedstack Fuel Cell Technology, GenCell, HDF Energy, Intelligent Energy, NUVERA FUEL CELLS, Hyzon Motors, Honda Motor, Hunter New Energy, and FCT Energy. Companies in the prime power stationary fuel cell market are focusing on advancing fuel cell efficiency and durability through continuous research and development initiatives. Strategic partnerships with energy providers and hydrogen infrastructure developers are helping accelerate deployment and commercialization. Manufacturers are expanding production capabilities to reduce costs and improve scalability for large-scale applications. Investment in pilot projects and demonstration plants is supporting technology validation and market acceptance. Firms are also prioritizing the integration of fuel cells into hybrid and decentralized energy systems to enhance operational flexibility. In addition, companies are strengthening their presence through geographic expansion, government collaborations, and participation in clean energy programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & Confidence Scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Capacity trends

- 2.4 End Use trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By End Use

- 3.8.2 By Region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 < 3 kW

- 5.3 3 - 10 kW

- 5.4 > 10 - 50 kW

- 5.5 > 50 kW

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industry/Utility

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Austria

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 South Korea

- 7.4.3 China

- 7.4.4 India

- 7.4.5 Philippines

- 7.4.6 Vietnam

- 7.5 Middle East & Africa

- 7.5.1 South Africa

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 Ballard Power Systems

- 8.2 Bloom Energy

- 8.3 Cummins

- 8.4 Doosan Corporation

- 8.5 FCT Energy

- 8.6 Frost and Sullivan

- 8.7 Fuel Cell Energy

- 8.8 Fuji Electric

- 8.9 GenCell

- 8.10 HDF Energy

- 8.11 Honda Motor

- 8.12 Hunter New Energy

- 8.13 Hyundai Motor

- 8.14 Hyzon Motors

- 8.15 Intelligent Energy

- 8.16 Nedstack Fuel Cell Technology

- 8.17 NUVERA FUEL CELLS

- 8.18 Plug Power

- 8.19 Robert Bosch GmbH

- 8.20 SFC Energy

航太與國防燃料電池市場:2026-2032年全球市場預測燃料電池市場:按類型、組件、燃料類型、冷卻方式、系統配置、分銷管道和最終用戶分類-2026-2032年全球市場預測

航太與國防燃料電池市場:2026-2032年全球市場預測燃料電池市場:按類型、組件、燃料類型、冷卻方式、系統配置、分銷管道和最終用戶分類-2026-2032年全球市場預測 全球燃料電池航太應用市場:機會與策略展望(至2035年)

全球燃料電池航太應用市場:機會與策略展望(至2035年) 燃料電池:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

燃料電池:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 燃料電池技術市場規模、佔有率和成長分析:按燃料電池類型、組件、尺寸、應用、最終用戶和地區分類-2026-2033年產業預測

燃料電池技術市場規模、佔有率和成長分析:按燃料電池類型、組件、尺寸、應用、最終用戶和地區分類-2026-2033年產業預測 燃料電池市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

燃料電池市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 燃料電池膜-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。

燃料電池膜-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。 全球石墨烯燃料電池市場研究報告(2026版)

全球石墨烯燃料電池市場研究報告(2026版) 燃料電池市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類-2026-2034年洞察與預測

燃料電池市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類-2026-2034年洞察與預測 燃料電池市場:依應用、技術、區域分類

燃料電池市場:依應用、技術、區域分類