|

市場調查報告書

商品編碼

2038390

再生式渦輪泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Regenerative Turbine Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

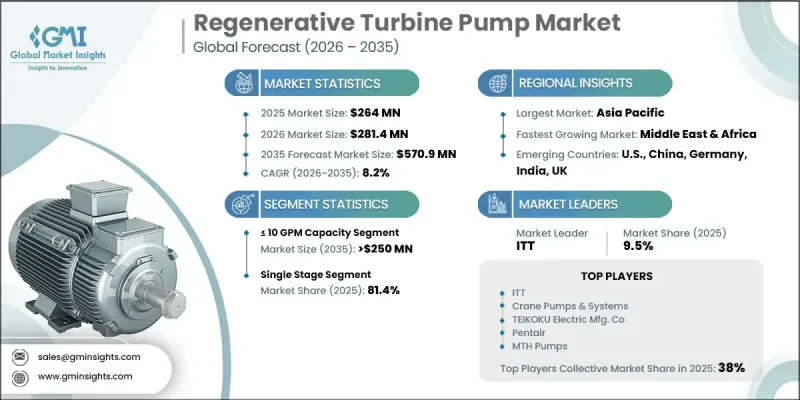

預計到 2025 年,全球再生式渦輪幫浦市場價值將達到 2.64 億美元,年複合成長率為 8.2%,到 2035 年將達到 5.709 億美元。

受工業和商業應用領域對節能型流體處理系統需求不斷成長的推動,該市場正在蓬勃發展。暖通空調(HVAC)產業的擴張,得益於建設活動的活性化和對高效建築基礎設施的需求,對市場需求起到了顯著的推動作用。此外,包括污水處理和發電工程在內的基礎設施建設投資的增加,也促進了這些產品的普及,尤其是在快速工業化和都市化的開發中國家。對系統效率、緊湊型設備設計和先進流體控制技術的日益關注,進一步加速了市場滲透。數位化監控功能的整合和現有泵浦系統的現代化改造,也為各終端用戶領域的持續成長做出了貢獻。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2.64億美元 |

| 預測金額 | 5.709億美元 |

| 複合年成長率 | 8.2% |

再生式渦輪泵採用獨特的葉輪設計,葉片尺寸小巧,即使在低流量條件下也能輸送高壓流體。這類幫浦廣泛應用於需要高揚程和流量控制的場合,例如冷凝水輸送、鍋爐給水系統和高壓液體處理。其高效性、穩定的流量特性以及在嚴苛工況下的出色表現,使其成為工業環境的理想選擇。市場對緊湊型和可客製化泵浦解決方案的需求日益成長,進一步推動了再生式渦輪泵的普及。此外,智慧監控系統和物聯網維修方案的日益廣泛應用,也提高了運作效率,並拓展了其在現代工業設施中的應用前景。

預計到2035年,流量低於10加侖/分鐘(GPM)的流體循環系統市場規模將達到2.5億美元。由於此細分市場適用於對結構緊湊、流體運動控制高度精準的精密系統,因此市場需求不斷成長。高科技製造業的擴張進一步增加了對精密流體循環解決方案的需求。與自動化控制系統和遠端監控技術的整合提高了系統性能和運行可靠性,從而進一步推動了該細分市場的成長。

到2025年,單級再生式渦輪泵將佔據81.4%的市場。這一主導地位歸功於其即使在高溫條件下也能提供穩定的壓力性能和可靠的運作。工業流體輸送和壓力管理應用領域的不斷擴展持續支撐著市場需求。此外,基礎設施的快速發展和應用領域的多元化也為多個行業的應用提供了更多機會。

2025年,美國再生式渦輪幫浦市場規模預計將達3,460萬美元。該國市場成長的主要驅動力是工業和商業領域對精密流量控制系統的需求不斷成長。泵浦效率、壓力處理能力和運作可靠性的持續提升,進一步加速了其在關鍵終端應用領域的普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 再生式渦輪泵成本結構分析

- 新機會與趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

- 價格趨勢分析(美元/單位)(基於初步調查)

- 按地區分類(基於初步調查)

- 按產品分類(基於初步調查)

- 貿易數據分析(基於初步調查)

- 進出口額趨勢(基於初步調查)

- 主要貿易路線及關稅的影響(基於初步調查)

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

- 人工智慧和生成式人工智慧對市場(核心解決方案)的影響

- 人工智慧驅動的生產最佳化(核心解決方案)

- 預測性維護和故障檢測(核心解決方案)

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依產品分類,2022-2035年

- 多階段

- 單級

第6章 市場規模及預測:以首批法計算,2022-2035年

- 自啟動

- 非自啟動型

第7章 市場規模及預測:依產能分類,2022-2035年

- 10 加侖/分鐘或更少

- >10~30 GPM

- >30~60 GPM

- >60 GPM

第8章 市場規模及預測:依應用領域分類,2022-2035年

- 農業

- 化工廠

- 建築/施工

- 用水和污水

- 產業

- 石油和天然氣

- 其他

第9章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 奧地利

- 法國

- 德國

- 英國

- 義大利

- 西班牙

- 挪威

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 阿曼

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 秘魯

第10章:公司簡介

- All Motors &Equipment Direct

- Arroyo Process Equipment

- Circutec

- Corken

- Crane Pumps &Systems

- IDEX India

- ITT INC.

- Iwaki America Inc.

- Magnatex Pumps

- March May

- MTH Pumps

- Nikuni Corporation

- Pentair

- Roth Pump Co.

- SPECK Pumpen Verkaufsgesellschaft GmbH

- Sterling Pumps

- Tapflo

- TEIKOKU ELECTRIC MFG. CO.

- Viking Pump

- Xylem

The Global Regenerative Turbine Pump Market was valued at USD 264 million in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 570.9 million by 2035.

The market is witnessing growth supported by rising demand for energy-efficient fluid handling systems across industrial and commercial applications. Expansion of the HVAC industry, driven by increasing construction activity and the need for efficient building infrastructure, is playing a key role in strengthening demand. Additionally, rising investments in infrastructure development, including wastewater treatment and power generation projects, are supporting broader adoption, particularly in developing economies undergoing rapid industrialization and urbanization. Increasing focus on system efficiency, compact equipment design, and advanced fluid control technologies is further accelerating market penetration. The integration of digital monitoring capabilities and modernization of existing pumping systems is also contributing to sustained growth momentum across end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $264 Million |

| Forecast Value | $570.9 Million |

| CAGR | 8.2% |

The regenerative turbine pump operates using a unique impeller design with small vanes that enable high-pressure fluid movement even at low flow conditions. These pumps are widely used in applications requiring high head and controlled flow, such as condensate transfer, boiler feed systems, and high-pressure liquid handling. Their efficiency, stable flow characteristics, and ability to perform under demanding operating conditions make them highly suitable for industrial environments. Growing demand for compact and customizable pumping solutions is further boosting adoption. In addition, the increasing use of smart monitoring systems and IoT-enabled retrofitting solutions is enhancing operational efficiency and expanding deployment opportunities across modern industrial setups.

The <= 10 GPM capacity segment is projected to reach USD 250 million by 2035. Demand for this segment is rising due to its suitability in precision-driven systems that require compact design and highly controlled fluid movement. Expansion of high-tech manufacturing sectors is further increasing the need for accurate fluid circulation solutions. Integration with automated control systems and remote monitoring technologies is improving system performance and operational reliability, thereby strengthening segment growth.

The single-stage regenerative turbine pump segment accounted for an 81.4% share in 2025. This dominance is attributed to its ability to deliver stable pressure performance and reliable operation under high-temperature conditions. Increasing utilization in industrial fluid transfer and pressure management applications continues to support demand. However, rapid infrastructure development and diversification of application areas are expanding deployment opportunities across multiple sectors.

United States Regenerative Turbine Pump Market was valued at USD 34.6 million in 2025. Growth in the country is supported by rising demand for precise flow control systems in industrial and commercial operations. Continuous advancements in pump efficiency, pressure handling capability, and operational reliability are further driving adoption across critical end-use applications.

Major players operating in the Global Regenerative Turbine Pump Industry include Xylem, Pentair, ITT, Crane Pumps & Systems, Viking Pump, Iwaki America, SPECK Pumpen, Tapflo, TEIKOKU ELECTRIC, and Nikuni Corporation. Companies in the Regenerative Turbine Pump Market are focusing on enhancing product efficiency through advanced impeller designs and improved hydraulic performance to support low-flow, high-pressure applications. They are increasingly investing in digital integration, including IoT-enabled monitoring and predictive maintenance systems, to improve operational reliability and reduce downtime. Manufacturers are expanding product customization capabilities to meet diverse industrial requirements across HVAC, energy, and process industries. Strategic partnerships with infrastructure and industrial project developers are helping firms strengthen market penetration. In addition, companies are optimizing manufacturing processes to reduce production costs while improving durability and performance standards. Expansion of aftermarket services, including maintenance and retrofit solutions, is also being prioritized to build long-term customer relationships and strengthen recurring revenue streams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Priming trends

- 2.1.4 Capacity trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of regenerative turbine pump

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By product (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Core Solution)

- 3.14.1 AI-Driven production optimization (Core Solution)

- 3.14.2 Predictive maintenance & fault detection (Core Solution)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Multi-stage

- 5.3 Single-stage

Chapter 6 Market Size and Forecast, By Priming, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Self priming

- 6.3 Non self priming

Chapter 7 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 ≤ 10 GPM

- 7.3 > 10 - 30 GPM

- 7.4 > 30 - 60 GPM

- 7.5 > 60 GPM

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Agriculture

- 8.3 Chemical plants

- 8.4 Building & construction

- 8.5 Water & wastewater

- 8.6 Industrial

- 8.7 Oil & gas

- 8.8 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Austria

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 UK

- 9.3.5 Italy

- 9.3.6 Spain

- 9.3.7 Norway

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Oman

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Peru

Chapter 10 Company Profiles

- 10.1 All Motors & Equipment Direct

- 10.2 Arroyo Process Equipment

- 10.3 Circutec

- 10.4 Corken

- 10.5 Crane Pumps & Systems

- 10.6 IDEX India

- 10.7 ITT INC.

- 10.8 Iwaki America Inc.

- 10.9 Magnatex Pumps

- 10.10 March May

- 10.11 MTH Pumps

- 10.12 Nikuni Corporation

- 10.13 Pentair

- 10.14 Roth Pump Co.

- 10.15 SPECK Pumpen Verkaufsgesellschaft GmbH

- 10.16 Sterling Pumps

- 10.17 Tapflo

- 10.18 TEIKOKU ELECTRIC MFG. CO.

- 10.19 Viking Pump

- 10.20 Xylem

單軸汽輪機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、功率、終端用戶產業、應用、地區和競爭格局分類,2021-2031年

單軸汽輪機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、功率、終端用戶產業、應用、地區和競爭格局分類,2021-2031年 電輪機市場:按類型、功率範圍、技術和最終用途分類-2026年至2032年全球市場預測

電輪機市場:按類型、功率範圍、技術和最終用途分類-2026年至2032年全球市場預測 2026年全球渦輪馬達市場報告

2026年全球渦輪馬達市場報告 渦輪馬達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測渦輪機市場:按類型、功率範圍、組件和應用分類-2026-2032年全球市場預測

渦輪馬達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測渦輪機市場:按類型、功率範圍、組件和應用分類-2026-2032年全球市場預測 風力發電機控制系統市場規模、佔有率和成長分析:按組件、控制系統類型、應用、最終用戶和地區分類-2026-2033年產業預測立式渦輪泵市場 - 全球產業規模、佔有率、趨勢、機會、預測:按揚程類型、級數、最終用途產業、地區和競爭格局分類,2021-2031年

風力發電機控制系統市場規模、佔有率和成長分析:按組件、控制系統類型、應用、最終用戶和地區分類-2026-2033年產業預測立式渦輪泵市場 - 全球產業規模、佔有率、趨勢、機會、預測:按揚程類型、級數、最終用途產業、地區和競爭格局分類,2021-2031年 再生式渦輪泵市場規模、佔有率和成長分析(按泵浦類型、流量、引水方式、應用和地區分類)—產業預測(2026-2033 年)水下渦輪機市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、按容量、按最終用戶、按地區和競爭細分,2020-2030 年)流量增強渦輪機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、渦輪機類型、最終用戶、材料、地區、競爭進行細分,2020-2030 年預測

再生式渦輪泵市場規模、佔有率和成長分析(按泵浦類型、流量、引水方式、應用和地區分類)—產業預測(2026-2033 年)水下渦輪機市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、按容量、按最終用戶、按地區和競爭細分,2020-2030 年)流量增強渦輪機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、渦輪機類型、最終用戶、材料、地區、競爭進行細分,2020-2030 年預測