|

市場調查報告書

商品編碼

2038379

蛋白質粉市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Protein Powder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

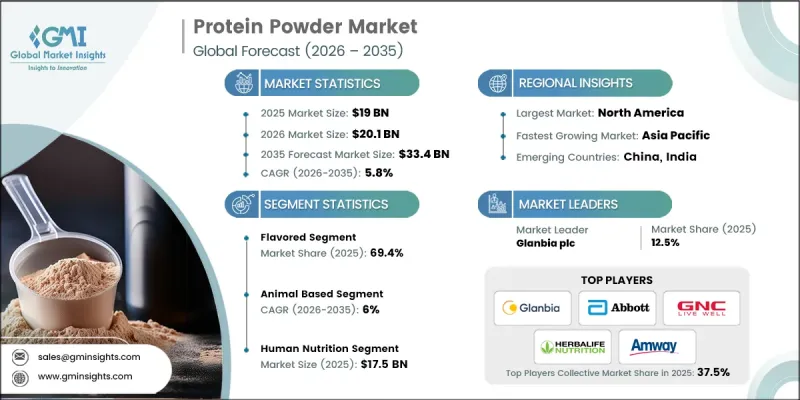

全球蛋白質粉市場預計到 2025 年價值 190 億美元,預計到 2035 年將以 5.8% 的複合年成長率成長至 334 億美元。

隨著消費者偏好轉向更健康的生活方式、功能性營養和創新產品,蛋白質產業也穩步發展。人們對永續性、消化健康和道德採購的日益關注,正在加速向植物來源和混合蛋白產品的轉型。同時,配方技術的進步正在改善產品的口感、質地和營養吸收率,使其更受廣大消費者的青睞。個人化正成為關鍵趨勢,各大品牌紛紛推出客製化的蛋白質解決方案,以滿足個人的飲食需求和健康目標。功能性成分和數位化營養規劃也在推動產品差異化。雖然傳統蛋白質來源仍然佔據主導地位,但隨著飲食習慣的改變,替代蛋白質正迅速崛起。蛋白質粉在健身、臨床營養和一般健康應用領域的日益廣泛,進一步推動了市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 190億美元 |

| 預測金額 | 334億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,風味蛋白粉的市佔率將達到69.4%,並在2035年之前以5.8%的複合年成長率成長。這些產品因其口感更佳、服用方便且易於購買而持續受到消費者的歡迎。消費者對便利美味的營養補充品的強烈偏好不斷推動著市場發展,而這一細分市場競爭激烈,銷售往往是決定性因素。

預計到2025年,運動員和健身者細分市場將佔市場佔有率的28%,到2035年將以5.5%的複合年成長率成長。此細分市場仍是主要的消費群體,其成長動力主要來自對肌肉成長和運動表現提升的需求。同時,老年人口的成長也推動了肌肉維持和恢復需求的成長。此外,受健身趨勢和生活方式變化的影響,蛋白質產品的使用在年輕一代中也越來越普遍。

預計2026年至2035年,北美蛋白粉市場將以6.4%的複合年成長率成長。該地區憑藉較高的消費者意識、先進的產品創新以及個人化、潔淨標示營養產品日益成長的受歡迎程度,保持著強勁的市場地位。成熟市場參與企業的加入以及數位化零售通路的快速擴張,進一步推動了不同消費群的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 無味

- 口味(巧克力、香草、草莓等)

第6章 市場估計與預測:依來源分類,2022-2035年

- 植物來源

- 大豆

- 豌豆

- 米

- 麻

- 螺旋藻

- 小麥

- 混合植物

- 其他

- 動物源性

- 乳清蛋白

- 乳清濃縮物

- 乳清隔離群

- 乳清水解物

- 酪蛋白

- 雞蛋蛋白

- 膠原蛋白

- 昆蟲來源的蛋白質

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 人類營養

- 運動營養

- 機能性食品

- 體重管理

- 臨床和醫療護理

- 整體健康

- 動物營養

- 水產養殖

- 家禽

- 豬

- 牛

- 馬

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 運動員和健身者

- 職業運動員

- 業餘健身者

- 健身愛好者

- 去健身房的人

- 以休閒為目的進行運動的人

- 注重健康的

- 體重管理

- 保持整體健康

- 臨床和醫療用戶

- 術後恢復

- 營養不良的治療

- 老齡化與肌少症

- 青少年和年輕人

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上零售

- 電子商務平台

- D2C網站

- 訂閱服務

- 超級市場/大賣場

- 現代零售連鎖

- 傳統超級市場

- 專賣店

- 營養保健食品

- 營養補充品專賣店

- 藥局/藥局

- 連鎖藥局

- 獨立經營藥房

- 其他

- 健身房/健身中心

- 直銷

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- Glanbia plc

- Abbott Laboratories

- GNC Holdings, Inc.

- Herbalife Nutrition Ltd.

- Amway Corporation

- Nestle SA

- GSK Consumer Healthcare(Haleon)

- Melaleuca Inc.

- Atlantic Multipower UK Limited

- Tata Consumer Products

The Global Protein Powder Market was valued at USD 19 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 33.4 billion by 2035.

The industry is evolving steadily as consumer preferences shift toward healthier lifestyles, functional nutrition, and innovative product offerings. Growing awareness of sustainability, digestive wellness, and ethical sourcing is accelerating the transition toward plant-based and blended protein formulations. At the same time, advancements in formulation technologies are improving taste, texture, and nutrient absorption, making products more appealing to a broader consumer base. Personalization is becoming a key trend, with brands introducing customized protein solutions aligned with individual dietary needs and wellness goals. Functional ingredients and digitally supported nutrition planning are also enhancing product differentiation. While traditional protein sources continue to maintain a strong foothold, alternative proteins are gaining momentum due to changing dietary habits. The expanding role of protein powders across fitness, clinical nutrition, and general wellness applications is further supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19 Billion |

| Forecast Value | $33.4 Billion |

| CAGR | 5.8% |

Flavored protein powder accounted for 69.4% share in 2025 and is expected to grow at a CAGR of 5.8% through 2035. These products remain highly popular due to their enhanced taste profiles, ease of consumption, and widespread availability. Strong consumer preference for convenient and enjoyable nutrition options continues to drive demand, making this segment highly competitive and volume-focused.

The athletes and bodybuilders segment held a share of 28% in 2025 and is anticipated to grow at a CAGR of 5.5% by 2035. This segment continues to represent a major consumer base due to the need for muscle development and performance enhancement. At the same time, an expanding demographic of older consumers is contributing to demand, driven by the need to maintain strength and support recovery. Younger populations are also increasingly adopting protein-based products, influenced by evolving fitness trends and lifestyle changes.

North America Protein Powder Market is expected to grow at a CAGR of 6.4% during 2026-2035. The region maintains a strong position due to high consumer awareness, advanced product innovation, and increasing adoption of personalized and clean-label nutrition. The presence of established industry participants and the rapid expansion of digital retail channels are further supporting market growth across diverse consumer segments.

Key companies operating in the Protein Powder Market include Abbott Laboratories, Glanbia plc, Amway Corporation, Nestle S.A., GNC Holdings Inc., Herbalife Nutrition Ltd., Tata Consumer Products, Melaleuca Inc., Atlantic Multipower UK Limited, and GSK Consumer Healthcare (Haleon). Companies in the protein powder market are strengthening their market position by investing in research and development to introduce innovative formulations with improved taste, texture, and nutritional value. They are expanding their product portfolios to include plant-based, blended, and functional protein options that cater to evolving consumer preferences. Strategic partnerships and collaborations are being utilized to enhance distribution networks and expand global reach. Firms are also focusing on digital transformation, leveraging e-commerce platforms and personalized nutrition tools to engage consumers directly. In addition, companies are emphasizing clean-label ingredients, sustainable sourcing, and transparent branding to build trust. Enhanced marketing strategies and influencer-driven campaigns are further supporting brand visibility and customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Source

- 2.2.4 Application

- 2.2.5 End-user

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Unflavored

- 5.3 Flavored (Chocolate, Vanilla, Strawberry, Others)

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plant-Based

- 6.2.1 Soy

- 6.2.2 Pea

- 6.2.3 Rice

- 6.2.4 Hemp

- 6.2.5 Spirulina

- 6.2.6 Wheat

- 6.2.7 Mixed Plant

- 6.2.8 Others

- 6.3 Animal-Based

- 6.3.1 Whey Protein

- 6.3.2 Whey Concentrate

- 6.3.3 Whey Isolate

- 6.3.4 Whey Hydrolysate

- 6.3.5 Casein

- 6.3.6 Egg Protein

- 6.3.7 Collagen

- 6.3.8 Insect Protein

- 6.3.9 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Human Nutrition

- 7.2.1 Sports Nutrition

- 7.2.2 Functional Foods

- 7.2.3 Weight Management

- 7.2.4 Clinical/Medical

- 7.2.5 General Wellness

- 7.3 Animal Nutrition

- 7.3.1 Aquaculture

- 7.3.2 Poultry

- 7.3.3 Swine

- 7.3.4 Cattle

- 7.3.5 Equine

- 7.3.6 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Athletes & Bodybuilders

- 8.2.1 Professional Athletes

- 8.2.2 Amateur Bodybuilders

- 8.3 Fitness Enthusiasts

- 8.3.1 Gym-Goers

- 8.3.2 Recreational Exercisers

- 8.4 Health-Conscious

- 8.4.1 Weight Management

- 8.4.2 General Wellness

- 8.5 Clinical/Medical Users

- 8.5.1 Post-Surgery Recovery

- 8.5.2 Malnutrition Treatment

- 8.5.3 Aging & Sarcopenia

- 8.6 Teenage & Youth

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Online Retail

- 9.2.1 E-commerce Platforms

- 9.2.2 D2C Websites

- 9.2.3 Subscription Services

- 9.3 Supermarkets/Hypermarkets

- 9.3.1 Modern Trade Chains

- 9.3.2 Traditional Supermarkets

- 9.4 Specialty Stores

- 9.4.1 Nutrition & Health Food

- 9.4.2 Supplement Specialty

- 9.5 Pharmacies/Drugstores

- 9.5.1 Chain Pharmacies

- 9.5.2 Independent Pharmacies

- 9.6 Others

- 9.6.1 Gyms & Fitness Centers

- 9.6.2 Direct Sales

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Glanbia plc

- 11.2 Abbott Laboratories

- 11.3 GNC Holdings, Inc.

- 11.4 Herbalife Nutrition Ltd.

- 11.5 Amway Corporation

- 11.6 Nestle S.A.

- 11.7 GSK Consumer Healthcare (Haleon)

- 11.8 Melaleuca Inc.

- 11.9 Atlantic Multipower UK Limited

- 11.10 Tata Consumer Products