|

市場調查報告書

商品編碼

2038369

衛星地面站市場機會、成長要素、產業趨勢分析及2026-2035年預測Satellite Ground Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球衛星地面站市場價值為587億美元,預計2035年將以8.5%的複合年成長率成長至1,326億美元。

衛星廣播服務覆蓋範圍的不斷擴大以及地面站技術的持續進步(提高了通訊效率和資料處理能力)是推動市場成長的主要因素。對基於衛星的遙感探測應用日益成長的需求,以及政府對太空探勘和研究活動的支持,也顯著促進了市場擴張。衛星發射數量的激增和對高容量全球連接日益成長的需求,進一步加速了對先進地面基礎設施的需求。此外,地球觀測資料的擴展和分析主導應用的普及,提升了衛星地面站對商業和機構領域的重要性。對高解析度、超高解析度和即時內容傳送的日益依賴,也提高了對訊號傳輸和接收基礎設施的要求。對自動化追蹤系統、雲端整合地面站解決方案以及擴充性通訊網路(支援持續衛星監測和資料交換)的投資增加,進一步支撐了市場發展。所有這些因素共同鞏固了衛星地面站作為全球現代太空通訊生態系統重要組成部分的地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 587億美元 |

| 預測市場規模 | 1326億美元 |

| 複合年成長率 | 8.5% |

到2025年,硬體部分將佔69.1%的市場佔有率。這一主導地位主要得益於天線、射頻系統、衛星追蹤技術以及對可靠衛星通訊運作至關重要的配套基礎設施的廣泛部署。硬體構成地面部分能力的核心,能夠有效率地在地球靜止軌道和低地球軌道衛星系統中實現遙測、追蹤、指令和訊號傳輸。大規模衛星星系的日益部署和全球地面網路的擴展,進一步推動了對先進高效能硬體系統的需求。

到2025年,低地球軌道(LEO)衛星將佔61.2%的市佔率。這一主導地位主要得益於用於寬頻連接、地球觀測服務和物聯網(IoT)應用的LEO衛星星系的快速擴張。由於LEO衛星軌道周期短且移動頻繁,因此需要廣泛的地面站覆蓋和持續的追蹤支援。這促使人們加速投資自動化即時監控技術和先進的數據處理系統,以防止通訊中斷並確保高效的衛星切換管理。

預計到2025年,北美衛星地面站市佔率將達到42.6%。這得歸功於其強大的技術基礎設施和日益成長的衛星通訊需求。該地區市場成長的主要驅動力是低地球軌道(LEO)衛星網路的快速擴張,以及美國和加拿大對寬頻和地球觀測服務需求的不斷成長。憑藉成熟的航太技術、雲端地面站平台的廣泛應用以及各國政府對安全衛星通訊系統的大量投資,該地區正鞏固其在全球市場的領先地位。

亞馬遜網路服務 (AWS)、微軟 Azure Orbital、L3Harris Technologies、Viasat Inc.、Hughes Network Systems (EchoStar)、Consberg Satellite Services (KSAT)、瑞典航太公司 (SSC)、Girat Satellite Networks、Atlas Space 月和日本宇宙航空研究開發機構 (JAXA) 是全球衛星地面站市場的主要參與者。這些公司致力於擴展其自動化和雲端整合的地面基礎設施,以提高營運效率和擴充性。他們投資先進的追蹤系統、人工智慧驅動的數據處理和即時衛星監控解決方案,以提高通訊可靠性。與衛星營運商和雲端服務供應商的策略合作正在擴大服務覆蓋範圍並加快地面網路的部署。此外,各公司也優先開發模組化、軟體定義的地面站架構,以降低營運成本並提高柔軟性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 衛星廣播服務滲透率的提高

- 衛星地面站技術的不斷進步

- 遙感探測應用領域對衛星服務的需求日益成長

- 政府對航太研究機構的支持

- 地球觀測影像和分析解決方案的廣泛應用

- 產業潛在風險與挑戰

- 缺乏規章制度和政策措施

- 持續的頻寬問題

- 市場機遇

- 利用人工智慧實現自主地面站運行

- 虛擬化與共用地面站網路

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢(基於付費資料庫)

- 歷史價格分析(2022-2025)

- 影響價格趨勢的因素

- 區域價格波動

- 價格預測(2026-2035)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估算與預測:依解類型分類,2022-2035年

- 硬體

- 天線系統

- 射頻系統和定時

- 基頻和記錄硬體

- 儲存和網路單元

- 電源和機架

- 軟體

- 任務控制和飛行動力學

- 基頻/虛擬調變解調器和波形

- 網路安全和金鑰管理

- 網路監控/編配

- 服務

- Direct-to-Satellite(DTS)

- 衛星地面站回程傳輸

- 託管服務和系統整合

第6章 市場估計與預測:依平台類型分類,2022-2035年

- 固定的

- 可攜式的

- 移動站

第7章 市場估計與預測:依頻段分類,2022-2035年

- L波段

- S波段

- C波段

- X波段

- Ku,Ka波段

- 高頻/甚高頻/UHF頻段

- 其他

第8章 市場估算與預測:依發展軌跡類型分類,2022-2035年

- 低地球軌道(LEO)

- 中軌道(MEO)

- 地球靜止軌道(GEO)

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 溝通

- 地球觀測

- 導航

- 太空探索

- 衛星遙測、追蹤與控制子系統

- 閘道器和網路互連

- 其他

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- 防禦

- 軍隊

- 空軍

- 海軍

- 政府

- 公共安全和私人組織

- 航太機構和研究中心

- 商業的

- 衛星和傳送服務提供商

- 通訊業者和服務供應商

- 商業和移動性

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Kongsberg Satellite Services(KSAT)

- Viasat Inc.

- Amazon Web Services

- Microsoft Azure Orbital

- Swedish Space Corporation(SSC)

- Comtech Telecommunications Corp.

- L3Harris Technologies

- 本地球員

- Japan Aerospace Exploration Agency(JAXA)

- 歐洲太空總署(ESA)

- Gilat Satellite Networks

- Hughes Network Systems(EchoStar)

- 新興企業

- RBC Signals

- Atlas Space Operations

- KLEO Connect

- Leaf Space

- Northstar Earth & Space

- QuadSAT

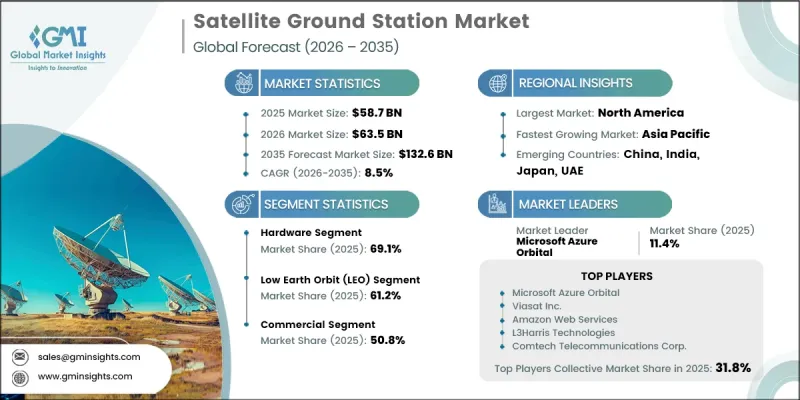

The Global Satellite Ground Station Market was valued at USD 58.7 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 132.6 billion by 2035.

Market growth is driven by the increasing penetration of satellite-based broadcasting services and continuous advancements in ground station technologies that enhance communication efficiency and data processing capabilities. Rising demand for satellite-enabled remote sensing applications is also contributing significantly to expansion, alongside supportive government initiatives promoting space exploration and research activities. The rapid increase in satellite launches and the growing need for high-capacity global connectivity are further accelerating demand for advanced ground infrastructure. In addition, the expansion of Earth observation data, along with analytics-driven applications, is strengthening the importance of satellite ground stations across commercial and institutional sectors. Increasing reliance on high-definition, ultra-high-definition, and real-time content delivery is also reinforcing infrastructure requirements for signal transmission and reception. The market is further supported by growing investments in automated tracking systems, cloud-integrated ground station solutions, and scalable communication networks that enable continuous satellite monitoring and data exchange. These combined factors are positioning satellite ground stations as a critical component of modern space-based communication ecosystems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $58.7 Billion |

| Forecast Value | $132.6 Billion |

| CAGR | 8.5% |

The hardware segment accounted for a share of 69.1% in 2025. This dominance is attributed to the extensive deployment of antennas, RF systems, satellite tracking technologies, and supporting infrastructure essential for reliable satellite communication operations. Hardware forms the core foundation of ground segment functionality, enabling efficient telemetry, tracking, command, and signal transmission across both geostationary and low Earth orbit satellite systems. Increasing deployment of large satellite constellations and expanding global ground networks is further strengthening demand for advanced and high-performance hardware systems.

The Low Earth Orbit segment held a 61.2% share in 2025. This leadership is driven by the rapid expansion of LEO satellite constellations used for broadband connectivity, Earth observation services, and Internet of Things applications. Due to their short orbital duration and frequent movement, LEO satellites require extensive ground station coverage and continuous tracking support. This is accelerating investment in automated, real-time monitoring technologies and advanced data processing systems to ensure uninterrupted communication and efficient satellite handover management.

North America Satellite Ground Station Market accounted for 42.6% share in 2025, supported by strong technological infrastructure and growing satellite communication requirements. Market growth in the region is driven by the rapid expansion of LEO satellite networks and increasing demand for broadband and Earth observation services across the United States and Canada. The region benefits from well-established aerospace capabilities, widespread adoption of cloud-based ground station platforms, and substantial government investment in secure satellite communication systems, strengthening its leadership in the global market.

Amazon Web Services, Microsoft Azure Orbital, L3Harris Technologies, Viasat Inc., Hughes Network Systems (EchoStar), Kongsberg Satellite Services (KSAT), Swedish Space Corporation (SSC), Gilat Satellite Networks, Atlas Space Operations, RBC Signals, Comtech Telecommunications Corp., Leaf Space, QuadSAT, Northstar Earth & Space, KLEO Connect, European Space Agency (ESA), and Japan Aerospace Exploration Agency (JAXA) are among the key players operating in the Global Satellite Ground Station Market. Companies in the Satellite Ground Station Market are focusing on expanding automated and cloud-integrated ground infrastructure to strengthen operational efficiency and scalability. They are investing in advanced tracking systems, AI-driven data processing, and real-time satellite monitoring solutions to improve communication reliability. Strategic partnerships with satellite operators and cloud service providers are enabling wider service coverage and faster deployment of ground networks. Firms are also prioritizing the development of modular and software-defined ground station architectures to reduce operational costs and increase flexibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution type trends

- 2.2.2 Platform type trends

- 2.2.3 Frequency band trends

- 2.2.4 Orbit type trends

- 2.2.5 Application trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased penetration of satellite-based broadcasting services.

- 3.2.1.2 Continuous technological advancements in satellite ground stations.

- 3.2.1.3 Rising satellite service demand for remote sensing applications.

- 3.2.1.4 Favorable government initiatives to support space research agencies.

- 3.2.1.5 Proliferation of Earth observation imagery and analytics solutions.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of regulations and government policies.

- 3.2.2.2 Constant bandwidth issues.

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled autonomous ground station operations

- 3.2.3.2 Virtualized and shared ground station networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends (Based on paid Database)

- 3.8.1 Historical Price Analysis (2022-2025)

- 3.8.2 Price Trend Drivers

- 3.8.3 Regional Price Variations

- 3.8.4 Price Forecast (2026-2035)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Antenna systems

- 5.2.2 RF systems & timing

- 5.2.3 Baseband & recording hardware

- 5.2.4 Storage & networking units

- 5.2.5 Power & racks

- 5.3 Software

- 5.3.1 Mission control & flight dynamics

- 5.3.2 Baseband/virtual modems & waveforms

- 5.3.3 Cybersecurity & key management

- 5.3.4 Network M&C/orchestration

- 5.4 Services

- 5.4.1 Direct-to-Satellite (DTS)

- 5.4.2 Satellite ground station backhaul

- 5.4.3 Managed services & system integration

Chapter 6 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Fixed

- 6.3 Portable

- 6.4 Mobile stations

Chapter 7 Market Estimates and Forecast, By Frequency Band, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 L-Band

- 7.3 S-Band

- 7.4 C-Band

- 7.5 X-Band

- 7.6 Ku & Ka-Band

- 7.7 HF/VHF/UHF-Band

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Low Earth Orbit (LEO)

- 8.3 Medium Earth Orbit (MEO)

- 8.4 Geostationary Earth Orbit (GEO)

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Communication

- 9.3 Earth observation

- 9.4 Navigation

- 9.5 Space research

- 9.6 Satellite telemetry, tracking and control subsystems

- 9.7 Gateway & network interconnection

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Defense

- 10.2.1 Army

- 10.2.2 Air force

- 10.2.3 Navy

- 10.3 Government

- 10.3.1 Public safety & civil agencies

- 10.3.2 Space agencies & research centers

- 10.4 Commercial

- 10.4.1 Satellite & teleport operators

- 10.4.2 Carriers & service providers

- 10.4.3 Enterprise & mobility

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Kongsberg Satellite Services (KSAT)

- 12.1.2 Viasat Inc.

- 12.1.3 Amazon Web Services

- 12.1.4 Microsoft Azure Orbital

- 12.1.5 Swedish Space Corporation (SSC)

- 12.1.6 Comtech Telecommunications Corp.

- 12.1.7 L3Harris Technologies

- 12.2 Regional Players

- 12.2.1 Japan Aerospace Exploration Agency (JAXA)

- 12.2.2 European Space Agency (ESA)

- 12.2.3 Gilat Satellite Networks

- 12.2.4 Hughes Network Systems (EchoStar)

- 12.3 Emerging Players

- 12.3.1 RBC Signals

- 12.3.2 Atlas Space Operations

- 12.3.3 KLEO Connect

- 12.3.4 Leaf Space

- 12.3.5 Northstar Earth & Space

- 12.3.6 QuadSAT

衛星地面站市場:全球市場預測,2026-2032年

衛星地面站市場:全球市場預測,2026-2032年 衛星地面站市場規模、佔有率和成長分析:按組件、頻段、應用、最終用戶和地區分類-2026-2033年產業預測

衛星地面站市場規模、佔有率和成長分析:按組件、頻段、應用、最終用戶和地區分類-2026-2033年產業預測 衛星地面站市場報告:趨勢、預測與競爭分析(至2035年)

衛星地面站市場報告:趨勢、預測與競爭分析(至2035年) 衛星地面站設備市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、產品、功能、地區和競爭格局分類,2021-2031年

衛星地面站設備市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、產品、功能、地區和競爭格局分類,2021-2031年 衛星光學地面站市場分析及預測(至2035年):類型、產品、技術、應用、部署、功能

衛星光學地面站市場分析及預測(至2035年):類型、產品、技術、應用、部署、功能 2026年全球衛星地面站市場報告2026年全球地面站站點多樣性編配市場報告衛星地面站設備市場:2026年至2032年全球市場預測(依設備類型、頻段、部署模式、應用及最終用戶分類)

2026年全球衛星地面站市場報告2026年全球地面站站點多樣性編配市場報告衛星地面站設備市場:2026年至2032年全球市場預測(依設備類型、頻段、部署模式、應用及最終用戶分類) 衛星地面站市場:依解決方案、平台、功能和最終用途劃分-全球預測至2036年

衛星地面站市場:依解決方案、平台、功能和最終用途劃分-全球預測至2036年 衛星地面站市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

衛星地面站市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測