|

市場調查報告書

商品編碼

2038366

2026 年至 2035 年液氫運輸市場的商業機會、成長要素、產業趨勢與預測。Transportation Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

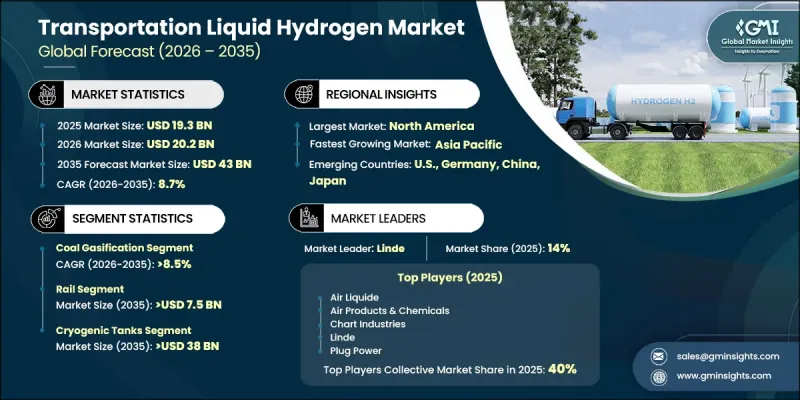

預計到 2025 年,全球液氫運輸市場價值將達到 193 億美元,並預計以 8.7% 的複合年成長率成長,到 2035 年達到 430 億美元。

液氫市場正呈現強勁成長勢頭,其高能量密度日益受到認可,使其極為適用於長途和重型運輸應用。液氫在儲存和運輸方面的效率在交通運輸系統中尤其重要,尤其是在航空和貨運領域,因為這些領域對性能和續航里程要求極高。氫燃料電池交通解決方案(包括巴士和卡車)的日益普及,進一步加速了液氫在產業中的應用。主要市場參與企業對先進氫技術的持續投資,正在加強商業化進程並擴大基礎設施容量。同時,日益嚴格的環境法規和全球永續性正推動運輸業向低排放和零排放的替代能源。對能夠快速加註、延長續航里程和提高運作效率的燃料的需求不斷成長,也促進了市場擴張。此外,不斷提高的淨零排放目標、更嚴格的排放標準以及低溫儲存系統和燃料電池技術的進步,都為液氫在運輸領域的長期成長前景做出了貢獻。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 193億美元 |

| 預測金額 | 430億美元 |

| 複合年成長率 | 8.7% |

預計到2035年,煤炭氣化市場將以8.5%的複合年成長率成長,這得益於有利於清潔能源轉型的政策框架。在政府目標的推動下,氫能經濟舉措的擴展正在促進煤炭氣化技術的更廣泛應用。煤炭氣化系統與二氧化碳捕集與儲存(CCS)解決方案的整合進一步提升了環境績效,並提高了工業界的接受度。此外,氣化製程的持續技術改進,以及低成本原料的供應,正在提高營運效率並降低環境影響。這增強了氫氣生產的經濟吸引力,並促進了市場滲透。

預計到2035年,低溫儲槽市場規模將達380億美元。人們日益關注低溫技術的進步,以提高運作安全性、效率和性能,這是推動市場擴張的主要動力。隔熱材料和工程技術的不斷改進進一步提升了儲罐容量,促進了其在氫氣和工業氣體應用領域的廣泛應用。

美國交通運輸用液氫市場預計到2035年將以8.6%的複合年成長率成長。強而有力的政策和產業支持,推動了清潔旅遊解決方案的普及,也促使各方加強減少溫室氣體排放,以應對氣候變遷。政府和私部門的相關人員都在積極投資交通運輸業的脫碳策略,這加速了氫能在整個出行領域的應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 重點轉向脫碳

- 人們對替代燃料的興趣日益濃厚

- 產業潛在風險與挑戰

- 氫氣加註站網路不足

- 促進因素

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 成本結構分析

- 價格趨勢分析,2022-2035年

- 按類型

- 按地區

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析(按國家/地區)

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依製造方法分類,2022-2035年

- 煤炭氣化

- SMR

- 電解

第6章 市場規模及預測:以分銷方式分類,2022-2035年

- 管道

- 低溫儲罐

第7章 市場規模及預測:依類型分類,2022-2035年

- LDV

- HDV

- 氫動力船

- 鐵路

- 港口機械

- 施工機械

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

第9章:公司簡介

- Air Liquide

- Air Products and Chemicals

- Chart Industries

- Cryolor

- Cryostar

- Demaco

- ENGIE

- Hexagon Purus

- INOX India Limited

- Iwatani Corporation

- Kawasaki Heavy Industries

- Linde plc

- Messer

- Mitsubishi Heavy Industries

- Nikkiso Co., Ltd.

- Plug Power Inc.

- Salzburger Aluminium Group

- Shell plc

- Worthington Industries

- Wuxi Yuantong Gas

The Global Transportation Liquid Hydrogen Market was valued at USD 19.3 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 43 billion by 2035.

The market is gaining strong traction as liquid hydrogen is increasingly recognized for its high energy density, which makes it highly suitable for long-distance and heavy-duty transportation applications. Its efficiency in storage and transport is particularly important for aviation and freight-intensive mobility systems where performance and range are critical. The rising deployment of hydrogen fuel cell-based mobility solutions, including buses and trucks, is further accelerating industry adoption. Continuous investments in advanced hydrogen technologies by key market participants are strengthening commercialization efforts and expanding infrastructure capabilities. At the same time, strict environmental regulations and global sustainability commitments are pushing the transportation sector toward low-emission and zero-emission energy alternatives. Growing demand for fuels that offer fast refueling, extended range, and high operational efficiency is also reinforcing market expansion. In addition, increasing net zero targets, tighter emission standards, and improvements in cryogenic storage systems and fuel cell technologies are collectively supporting the long-term growth outlook of the transportation liquid hydrogen market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.3 Billion |

| Forecast Value | $43 Billion |

| CAGR | 8.7% |

The coal gasification market is projected to grow at a CAGR of 8.5% by 2035, supported by favorable policy frameworks aimed at advancing clean energy transitions. Expanding hydrogen economy initiatives backed by government targets are encouraging wider adoption of coal gasification technologies. Integration of coal gasification systems with carbon capture and storage solutions is further improving environmental performance and enhancing industry acceptance. In addition, continuous technological improvements in gasification processes, along with the availability of cost-effective raw materials, are increasing operational efficiency and reducing environmental impact, making hydrogen production more economically attractive and supporting broader market penetration.

The cryogenic tanks market is expected to reach USD 38 billion by 2035. Growing focus on advancing cryogenic technologies to enhance operational safety, efficiency, and performance is significantly contributing to market expansion. Ongoing improvements in insulation materials and engineering techniques are further strengthening storage capabilities and supporting broader adoption across hydrogen and industrial gas applications.

U.S. Transportation Liquid Hydrogen Market is projected to grow at a CAGR of 8.6% through 2035. Increasing efforts to reduce greenhouse gas emissions and address climate change are driving strong policy and industrial support for clean mobility solutions. Both government bodies and private sector stakeholders are actively investing in decarbonization strategies for the transportation industry, which is accelerating hydrogen adoption across mobility applications.

Major players operating in the Global Transportation Liquid Hydrogen Industry include Air Liquide, Linde plc, Air Products and Chemicals, Shell plc, Chart Industries, Kawasaki Heavy Industries, Cryolor, ENGIE, Cryostar, Nikkiso Co., Ltd., Demaco, Mitsubishi Heavy Industries, Hexagon Purus, Messer, INOX India Limited, Plug Power Inc., Iwatani Corporation, Worthington Industries, Salzburger Aluminium Group, and Wuxi Yuantong Gas. Key companies in the Transportation Liquid Hydrogen Market are actively focusing on expanding large-scale hydrogen infrastructure, including liquefaction plants, storage systems, and transport networks to support growing demand. They are investing heavily in advanced cryogenic technologies to improve safety, efficiency, and cost-effectiveness of hydrogen handling. Strategic collaborations with governments, energy companies, and automotive manufacturers are strengthening ecosystem development and accelerating commercialization. Firms are also prioritizing R&D to enhance fuel cell integration, improve energy density, and reduce operational losses during storage and transport. Expansion into emerging markets through joint ventures and long-term supply contracts is helping companies secure stable revenue streams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Production Method trends

- 2.4 Distribution Method trends

- 2.5 Type trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Shifting focus toward decarbonization

- 3.3.1.2 Surging interest in alternative fuels

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Lack of network of hydrogen fuelling stations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Type

- 3.8.2 By Region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Production Method, 2022 - 2035 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal Gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution Method, 2022 - 2035 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic Tanks

Chapter 7 Market Size and Forecast, By Type, 2022 - 2035 (USD Billion & MT)

- 7.1 Key trends

- 7.2 LDV

- 7.3 HDV

- 7.4 Hydrogen Ship

- 7.5 Rail

- 7.6 Port machinery

- 7.7 Construction machinery

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

Chapter 9 Company Profiles

- 9.1 Air Liquide

- 9.2 Air Products and Chemicals

- 9.3 Chart Industries

- 9.4 Cryolor

- 9.5 Cryostar

- 9.6 Demaco

- 9.7 ENGIE

- 9.8 Hexagon Purus

- 9.9 INOX India Limited

- 9.10 Iwatani Corporation

- 9.11 Kawasaki Heavy Industries

- 9.12 Linde plc

- 9.13 Messer

- 9.14 Mitsubishi Heavy Industries

- 9.15 Nikkiso Co., Ltd.

- 9.16 Plug Power Inc.

- 9.17 Salzburger Aluminium Group

- 9.18 Shell plc

- 9.19 Worthington Industries

- 9.20 Wuxi Yuantong Gas

緊湊型空氣壓縮系統市場預測至2034年-全球產品類型、動力源、壓力範圍、潤滑方式、技術、通路、應用及區域分析全球儲氫材料市場預測至2034年-按材料類型、儲存機制、形態、應用、最終用戶和地區分類的分析

緊湊型空氣壓縮系統市場預測至2034年-全球產品類型、動力源、壓力範圍、潤滑方式、技術、通路、應用及區域分析全球儲氫材料市場預測至2034年-按材料類型、儲存機制、形態、應用、最終用戶和地區分類的分析 液氫儲罐市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

液氫儲罐市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 地下儲氫市場規模、佔有率和成長分析:按儲存類型、終端用戶產業和地區分類-2026-2033年產業預測氫載體市場預測至2034年-按載體類型、形態、來源、技術、應用、分銷、最終用戶和地區分類的全球分析

地下儲氫市場規模、佔有率和成長分析:按儲存類型、終端用戶產業和地區分類-2026-2033年產業預測氫載體市場預測至2034年-按載體類型、形態、來源、技術、應用、分銷、最終用戶和地區分類的全球分析 全球小型空氣壓縮系統市場:按產品類型、壓力、最終用戶和地區分類-預測(至2030年)氫氣儲存腔市場預測至2034年—按儲存類型、儲存容量、功能、應用、最終用戶和地區分類的全球分析

全球小型空氣壓縮系統市場:按產品類型、壓力、最終用戶和地區分類-預測(至2030年)氫氣儲存腔市場預測至2034年—按儲存類型、儲存容量、功能、應用、最終用戶和地區分類的全球分析 液氫儲罐市場:按類型、應用和地區分類氫氣儲存市場:按形式、類型、應用和地區分類

液氫儲罐市場:按類型、應用和地區分類氫氣儲存市場:按形式、類型、應用和地區分類 2026年全球固體儲氫材料市場報告

2026年全球固體儲氫材料市場報告