|

市場調查報告書

商品編碼

2027668

優格市場機會、成長要素、產業趨勢分析及2026-2035年預測Yogurt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

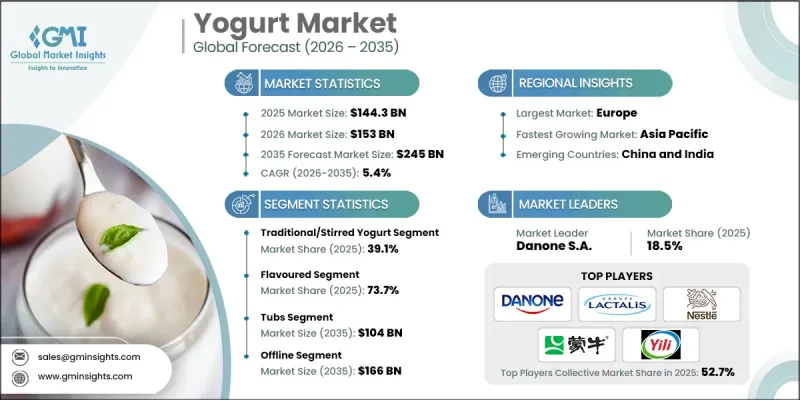

預計到 2025 年,全球優格市場價值將達到 1,443 億美元,年複合成長率為 5.4%,預計到 2035 年將達到 2,450 億美元。

全球優格產業正經歷持續成長,這主要得益於消費者對消化健康和免疫力提升意識的增強。隨著越來越多的人尋求符合健康生活方式的機能性食品,強化型和益生菌優格的需求持續成長。製造商正積極改進產品配方,並添加更多營養成分以滿足不斷變化的飲食需求。同時,快速的都市化和快節奏的生活方式也推動了人們對便利消費方式的需求,以適應繁忙的日程。儘管實體零售通路憑藉其強大的實體店網路仍然佔據主導地位,但隨著消費者轉向線上購物,數位平台也在迅速擴張。從區域來看,亞太地區正崛起為高成長市場,這得益於經濟發展和消費者習慣的改變。而北美和歐洲則是成熟市場,對高階產品的需求強勁。其他地區儘管面臨結構性挑戰,但正在逐步獲得發展動力,為優格市場的長期擴張開闢新的道路。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1443億美元 |

| 預測金額 | 2450億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,風味優格的市佔率將達到73.7%,並在2026年至2035年間以5.6%的複合年成長率成長。該細分市場持續強勁成長,這主要得益於其廣泛的市場需求和口味的不斷創新。相較之下,無糖優格則保持著穩定的需求,滿足了消費者對簡單、百搭、健康飲食和多種烹飪用途的需求。

預計2025年,貨櫃包裝市場規模將達695億美元,2035年將達1,040億美元,年複合成長率為4.1%。由於其實用性和成本效益,貨櫃包裝仍然是最廣泛採用的包裝形式,能夠滿足大眾消費需求。隨著便利性和便攜性日益成為影響購買決策的重要因素,其他包裝形式也越來越受到重視。

預計2026年至2035年,北美優格市場將以3.6%的複合年成長率成長。該地區的優格市場格局成熟且不斷演變,消費者偏好營養價值、產品透明度和優質產品。市場需求持續向高蛋白和功能性產品轉變,創新仍是競爭的關鍵因素。零售通路的拓展和新產品的不斷推出,以及消費者對植物來源替代品的日益關注,都在推動市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 消費者對富含益生菌、能促進腸道健康的益生菌功能性優格產品的需求日益成長。

- 在全球範圍內,人們越來越偏好方便快速、即食或即飲的優格產品。

- 零售基礎設施和低溫運輸物流的擴張提高了產品的供應量。

- 產業潛在風險與挑戰

- 由於容易變質,需要持續的低溫運輸管理,這會增加營運成本。

- 來自植物來源替代品的日益激烈的競爭正在影響傳統優格的消費趨勢。

- 原奶價格波動會影響生產成本和價格穩定性。

- 市場機遇

- 全球對高蛋白、低脂和功能性優格的創新需求日益成長。

- 線上雜貨平台的快速擴張正在擴大其對消費市場的覆蓋範圍。

- 新興市場消費者可支配收入的成長正在提振他們對乳製品的需求。

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 希臘優格

- 全脂希臘優格

- 低脂希臘優格

- 脫脂希臘優格

- 傳統/攪拌型優格

- 全脂傳統優格

- 低脂傳統優格

- 脫脂傳統優格

- 固狀優格

- 固狀優格有水果

- 原味優格固狀優格

- 乳酸飲料

- 乳製品乳酸飲料

- 植物來源乳酸飲料

- 霜凍優格

- 軟冰淇淋霜凍優格

- 包裝霜凍優格

第6章 市場估計與預測:依口味分類,2022-2035年

- 無味

- 原味傳統優格

- 原味希臘優格

- 原味植物優格

- 調味

- 水果味

- 香草風味

- 巧克力口味

- 其他口味

第7章 市場估價與預測:依包裝類型分類,2022-2035年

- 容器

- 單份包裝

- 家庭裝容器

- 小袋

- 可擠壓袋

- 立式袋

- 紙盒

- 利樂包裝盒

- 山形蓋頂紙箱

- 其他

- 瓶子

- 杯子

- 多包裝規格

第8章 市場估算與預測:依通路分類,2022-2035年

- 離線

- 大賣場和超級市場

- 專賣店

- 便利商店

- 其他

- 線上

- 品牌官方網站

- EC平台

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Danone SA

- Lactalis

- Nestle SA

- China Mengniu

- Inner Mongolia Yili

- FrieslandCampina

- Chobani, LLC

- FAGE International

- Meiji Holdings

- General Mills

The Global Yogurt Market was valued at USD 144.3 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 245 billion by 2035.

The global yogurt industry is experiencing sustained growth driven by rising consumer awareness surrounding digestive health and immune support. Demand for nutrient-enriched and probiotic-based yogurt continues to accelerate as individuals seek functional food options that align with wellness-focused lifestyles. Producers are actively enhancing product formulations by incorporating additional nutritional components to meet evolving dietary expectations. At the same time, rapid urban expansion and fast-paced routines are fueling demand for convenient consumption formats that fit into busy schedules. Retail channels remain dominant due to strong physical store networks, while digital platforms are expanding rapidly as consumers increasingly shift toward online purchasing. From a regional perspective, Asia Pacific is emerging as a high-growth market supported by economic development and changing consumption habits, while North America and Europe demonstrate maturity with strong demand for premium offerings. Other regions are gradually gaining traction despite structural challenges, creating new avenues for long-term expansion within the yogurt market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $144.3 Billion |

| Forecast Value | $245 Billion |

| CAGR | 5.4% |

The flavoured yogurt segment accounted for 73.7% share in 2025 and is projected to grow at a CAGR of 5.6% from 2026 to 2035. This segment continues to perform strongly due to its wide appeal and continuous innovation in taste profiles. In contrast, unflavored yogurt maintains steady demand among consumers seeking simple and versatile options that align with health-conscious consumption and broader culinary usage.

The tubs segment generated USD 69.5 billion in 2025 and is forecast to reach USD 104 billion by 2035, registering a CAGR of 4.1%. This format remains the most widely adopted due to its practicality for larger consumption needs and cost-effective purchasing. Alternative packaging formats are also gaining traction as convenience and portability become increasingly important factors influencing buying decisions.

North America Yogurt Market is expected to grow at a CAGR of 3.6% during 2026 to 2035. The region reflects a well-established yet evolving landscape where consumer preferences emphasize nutritional value, product transparency, and premium quality. Demand continues to shift toward high-protein and functionally enhanced products, while innovation remains a central competitive factor. Expanding retail availability and a steady introduction of new product variations are reinforcing market growth, with increasing attention also being given to plant-based alternatives.

Key players in the Yogurt Market include Nestle S.A., Danone S.A., General Mills, Lactalis, China Mengniu, FrieslandCampina, Inner Mongolia Yili, Chobani, LLC, Meiji Holdings, and FAGE International. Companies operating in the Yogurt Market are implementing a range of strategies to strengthen their competitive position and expand their market share. A major focus is placed on continuous product innovation, particularly in developing functional and nutrient-enriched offerings that align with evolving consumer preferences. Businesses are investing in advanced manufacturing technologies to improve efficiency and maintain consistent product quality. Strategic partnerships and supply chain optimization are being prioritized to ensure reliable sourcing and cost control. Expansion into high-growth regions is another key approach, supported by localized product development to suit regional tastes. In addition, companies are enhancing their branding and digital presence to engage consumers more effectively, while mergers and acquisitions are being used to access new markets, technologies, and distribution networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Flavor Type

- 2.2.4 Packaging Type

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for probiotic-rich and gut health functional yogurt products

- 3.2.1.2 Increasing preference for convenient, ready-to-eat and drinkable yogurt formats globally

- 3.2.1.3 Expanding retail infrastructure and cold chain logistics improving product accessibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High perishability requiring continuous cold chain management increases operational costs

- 3.2.2.2 Growing competition from plant-based alternatives impacting traditional yogurt consumption trends

- 3.2.2.3 Volatility in raw milk prices affecting production costs and pricing stability

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for high-protein, low-fat, and functional yogurt innovations globally

- 3.2.3.2 Rapid expansion of online grocery platforms enabling broader consumer market reach

- 3.2.3.3 Increasing disposable incomes in emerging markets boosting dairy consumption demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Greek Yogurt

- 5.2.1 Full-Fat Greek Yogurt

- 5.2.2 Low-Fat Greek Yogurt

- 5.2.3 Fat-Free Greek Yogurt

- 5.3 Traditional/Stirred Yogurt

- 5.3.1 Full-Fat Traditional Yogurt

- 5.3.2 Low-Fat Traditional Yogurt

- 5.3.3 Fat-Free Traditional Yogurt

- 5.4 Set Yogurt

- 5.4.1 Fruit-on-Bottom Set Yogurt

- 5.4.2 Plain Set Yogurt

- 5.5 Yogurt Drinks

- 5.5.1 Dairy-Based Yogurt Drinks

- 5.5.2 Plant-Based Yogurt Drinks

- 5.6 Frozen Yogurt

- 5.6.1 Soft-Serve Frozen Yogurt

- 5.6.2 Packaged Frozen Yogurt

Chapter 6 Market Estimates and Forecast, By Flavor Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Unflavoured

- 6.2.1 Plain Traditional Yogurt

- 6.2.2 Plain Greek Yogurt

- 6.2.3 Plain Plant-Based Yogurt

- 6.3 Flavoured

- 6.3.1 Fruit Flavoured

- 6.3.2 Vanilla Flavoured

- 6.3.3 Chocolate Flavoured

- 6.3.4 Other Flavours

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Tubs

- 7.2.1 Single-Serve Tubs

- 7.2.2 Family-Size Tubs

- 7.3 Pouches

- 7.3.1 Squeezable Pouches

- 7.3.2 Stand-Up Pouches

- 7.4 Cartons

- 7.4.1 Tetra Pack Cartons

- 7.4.2 Gable Top Cartons

- 7.5 Others

- 7.5.1 Bottles

- 7.5.2 Cups

- 7.5.3 Multi-Pack Formats

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Hypermarkets & Supermarkets

- 8.2.2 Specialty Stores

- 8.2.3 Convenience Stores

- 8.2.4 Others

- 8.3 Online

- 8.3.1 Brand Website

- 8.3.2 E-commerce Platform

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Danone S.A.

- 10.2 Lactalis

- 10.3 Nestle S.A.

- 10.4 China Mengniu

- 10.5 Inner Mongolia Yili

- 10.6 FrieslandCampina

- 10.7 Chobani, LLC

- 10.8 FAGE International

- 10.9 Meiji Holdings

- 10.10 General Mills

全球有機優格市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球脫脂優格市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球有機優格市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球脫脂優格市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 低脂優格市場報告:趨勢、預測與競爭分析(至2035年)優格市場報告:趨勢、預測與競爭分析(至2035年)

低脂優格市場報告:趨勢、預測與競爭分析(至2035年)優格市場報告:趨勢、預測與競爭分析(至2035年) 優格市場:依產品類型、包裝、通路和地區分類全球益生菌優格市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球風味優格市場規模、佔有率、趨勢和成長分析報告(2026-2034)

優格市場:依產品類型、包裝、通路和地區分類全球益生菌優格市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球風味優格市場規模、佔有率、趨勢和成長分析報告(2026-2034) 優格粉市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、包裝、最終用途、地區和競爭格局分類,2021-2031年A2優格市場:依產品類型、包裝類型、通路和地區分類優格機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、產品類型、銷售通路、地區和競爭格局分類,2021-2031年預測

優格粉市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、包裝、最終用途、地區和競爭格局分類,2021-2031年A2優格市場:依產品類型、包裝類型、通路和地區分類優格機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、產品類型、銷售通路、地區和競爭格局分類,2021-2031年預測