|

市場調查報告書

商品編碼

2027630

遊艇租賃市場機會、成長要素、產業趨勢分析及2026-2035年預測。Yacht Rental Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球遊艇租賃市場預計到 2025 年將價值 95 億美元,預計到 2035 年將以 6.7% 的複合年成長率成長至 180 億美元。

該市場是更廣泛的休閒、海洋和海洋旅遊業的一部分,目標客戶是尋求奢華體驗和個人化服務的消費者。遊艇租賃包括帆船、動力遊艇和超級遊艇的短期包租,用於私人用途、公司度假和各種活動。高淨值人口的成長和可支配收入的增加正日益推動市場發展,提升了對高階包租服務的需求。全球擁有超過13,000艘遊艇,該產業的成長與船隊組成、營運效率、消費者偏好和區域航行條件密切相關。全球高淨值人口以每年超過4%的速度成長,進一步促進了市場擴張,帶來了長期的收入潛力,並激勵營運商提升船隊品質和服務水準。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 95億美元 |

| 預測金額 | 180億美元 |

| 複合年成長率 | 6.7% |

預計到2025年,配備船員的遊艇租賃市場將佔據70%的市場佔有率,並透過提供全包式全方位服務,創造67億美元的收入。配備船員的遊艇租賃通常包括專業的船長、輪機長、廚師和接待人員,讓客戶無需操心任何操作細節,即可享受輕鬆奢華的體驗。無論是首次租賃還是回頭客,消費者都越來越重視便利性、優質服務、注重細節以及流暢無阻的體驗。這些全包式套餐確保了客戶的高度滿意度和回頭客,使配備船員的遊艇租賃成為遊艇租賃服務的基石。

憑藉速度、多功能性和豪華設施,動力遊艇市場預計將佔據81.8%的市場佔有率,到2025年市場規模將達到78億美元。這些遊艇配備強大的推進系統,使租賃者能夠有效率地進行長途航行,這在需求旺盛的巡航區域尤其有利。動力遊艇寬敞的內部空間和甲板、設備齊全的客艙、休息室、穩定器和娛樂設施,吸引追求舒適和高階體驗的消費者。其奢華、便利性和易於操作的特點,共同推動了旺季的需求,使動力遊艇成為整個行業收入的重要貢獻者。

美國遊艇租賃市場預計到2025年將達到15億美元,並在2026年至2035年間以7.6%的複合年成長率成長。美國擁有悠久的海洋旅遊傳統,並擁有蓬勃發展的休閒划船文化。美國遊艇產業透過創造就業機會、扶持小型企業和發展船舶製造業,為經濟成長做出了顯著貢獻。倡導團體和立法機構推動監管現代化、基礎建設和水路通行權的提升,進一步鞏固了遊艇租賃行業的發展。這些努力,加上休閒和豪華海洋旅遊參與度的不斷提高,正在鞏固北美遊艇租賃市場的成長勢頭。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 體驗式奢華旅行的需求日益成長。

- 高淨值人群(HNWI)數量增加

- 數位平台的擴展和預訂的便利性

- 企業團隊建立與獎勵旅遊需求

- 產業潛在風險與挑戰

- 高昂的營運和維護成本

- 需求的季節性波動

- 市場機遇

- 亞太地區和中東新興市場

- 永續環保的遊艇創新

- 會員制和訂閱模式的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國 -美國海岸警衛隊隊(USCG)

- 加拿大 - 加拿大海岸防衛隊 (CCG)

- 歐洲

- 德國 - 聯邦海事和水文局 (BSH)

- 義大利 - 港務局 - 海岸防衛隊

- 亞太地區

- 澳洲 - 澳洲海事安全局 (AMSA)

- 新加坡 - 新加坡海事及港務管理局 (MPA)

- 拉丁美洲

- 巴西 - 港口和海岸管理局 (DPC)

- 墨西哥 - 商船總局

- 中東和非洲

- 阿拉伯聯合大公國 - 杜拜海事城管理局 (DMCA)

- 南非 - 南非海事安全局 (SAMSA)

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- GPS導航系統

- 數位預訂平台

- 飛行中安全和通訊系統

- 新興技術

- 電動和混合動力推進系統

- 自主導航與控制系統

- 目前技術

- 專利趨勢(基於初步調查)

- 成本細分分析

- 購置和折舊免稅額費用

- 營運費用和燃料成本

- 船員薪資和培訓成本

- 維護、修理和整修

- 保險和監理合規成本

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 碼頭和港口基礎設施分析

- 全球碼頭容量和泊位可用性

- 港口基礎建設投資趨勢

- 監管要求和環境合規性

- 新興目的地和基礎建設發展

- 消費者行為與預訂模式

- 季節性預訂趨勢和高峰需求期

- 客戶獲取管道和數位轉換率

- 回頭客率和忠誠度計畫的有效性

- 按包機類型分類的客戶概況和消費趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估價與預測:以包機類型分類,2022-2035年

- 裸船租賃

- 包租帶船員

- 包租小木屋

- 會員制/公寓所有權章程

第6章 市場估價與預測:依遊艇分類,2022-2035年

- 豪華遊艇

- 帆船

- 雙體船

- 巨型/超級遊艇

- 格雷特

第7章 市場估算與預測:2022-2035年各型號遊艇長度

- 小型帆船(40英尺以下)

- 中型遊艇(40-80英尺)

- 大型遊艇(80-120英尺)

- 超級遊艇(超過120英尺)

第8章 市場估算與預測:依預訂週期分類,2022-2035年

- 按小時及按天計費的包機服務

- 每週包機

- 長期包機

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 休閒度假

- 企業活動

- 特別活動

- 探險/運動釣魚

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 克羅埃西亞

- 土耳其

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 菲律賓

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Burgess

- Northrop & Johnson

- Fraser Yachts

- Camper & Nicholsons

- IYC

- Edmiston

- Y.CO

- The Moorings

- Sunsail

- Dream Yacht Charter

- Nicholson Yachts

- Boatbookings

- 本地公司

- CharterWorld

- Yacht Charter Fleet

- TMM Yacht Charters

- Xclusive Yachts

- Navigare Yachting

- 新興企業

- CKIM

- Sydney by Sail

- Interparus

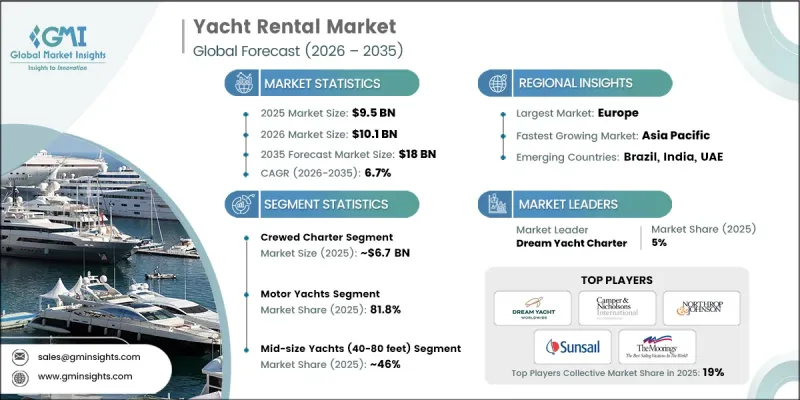

The Global Yacht Rental Market was valued at USD 9.5 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 18 billion by 2035.

The market is part of the broader leisure marine and maritime tourism sector, catering to consumers seeking luxury experiences and personalized services. Yacht rentals include short-term charters of sailing yachts, motor yachts, and superyachts for private use, corporate retreats, and events. The market is increasingly driven by high net worth individuals (HNWIs) and rising disposable incomes, fueling demand for premium charter services. With over thirteen thousand fleets available globally, the industry's growth is closely linked to fleet composition, operational efficiency, consumer preferences, and regional sailing conditions. Market expansion is further supported by the increasing global HNWI population, which grows by more than 4% annually, offering long-term revenue potential and encouraging operators to enhance fleet quality and service offerings.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.5 Billion |

| Forecast Value | $18 Billion |

| CAGR | 6.7% |

The crewed charter segment accounted for 70% share in 2025, generating USD 6.7 billion owing to the all-inclusive, full-service experience it provides. Crewed charters typically offer professional skippers, engineers, chefs, and hospitality personnel, allowing clients to enjoy hassle-free luxury without operational concerns. Consumers increasingly seek seamless, "frictionless" experiences, whether they are first-time renters or repeat clients, valuing convenience, premium service, and attention to detail. The all-inclusive nature of these packages ensures high customer satisfaction and repeat business, making crewed charters a cornerstone of yacht rental offerings.

The motor yachts segment captured 81.8% share in 2025, valued at USD 7.8 billion, due to their speed, versatility, and luxury amenities. These yachts provide powerful propulsion systems, enabling charterers to cover large distances efficiently, which is particularly advantageous in high-demand cruising areas. Motor yachts offer larger internal and deck spaces, well-equipped cabins, lounges, stabilizers, and entertainment facilities, appealing to consumers seeking comfort and premium experiences. Their combination of luxury, convenience, and operational ease drives demand during peak seasons and establishes motor yachts as major contributors to overall industry revenue.

U.S. Yacht Rental Market was valued at USD 1.5 billion in 2025 and is expected to grow at a CAGR of 7.6% between 2026 and 2035. The country has a long-standing maritime tourism tradition, supported by a robust recreational boating culture. The U.S. boating industry contributes significantly to economic growth, generating employment, supporting small businesses, and fostering marine manufacturing. Advocacy organizations and legislative support promoting modernized regulations, infrastructure development, and broader waterway access further enhance the yacht rental sector. These initiatives, combined with growing participation in recreational and luxury marine tourism, strengthen the market's growth trajectory in North America.

Leading companies in the Yacht Rental Industry include IYC, Camper & Nicholsons, Sunsail, Fraser Yachts, Burgess, Northrop & Johnson, CharterWorld, Dream Yacht Charter, Edmiston, and The Moorings. Companies in the Yacht Rental Market reinforce their presence by offering premium, personalized charter experiences, emphasizing all-inclusive and crewed services that remove operational complexity for clients. Fleet diversification, including high-end motor yachts and superyachts, ensures they meet demand across luxury, adventure, and corporate segments. Strategic partnerships with hospitality providers and event organizers expand service offerings. Firms invest in digital platforms for seamless booking, real-time customer support, and interactive itineraries. Marketing campaigns highlight exclusive experiences and aspirational lifestyle branding. Continuous investment in fleet maintenance, safety, and eco-friendly technologies enhances reputation and regulatory compliance. These strategies collectively drive customer loyalty, premium pricing potential, and long-term revenue growth in the competitive yacht rental sector.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Charter

- 2.2.3 Yacht

- 2.2.4 Yacht Length

- 2.2.5 Booking Duration

- 2.2.6 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for experiential luxury travel

- 3.2.1.2 Growth in high-net-worth individual (HNWI) population

- 3.2.1.3 Digital platform expansion & booking convenience

- 3.2.1.4 Corporate team-building & incentive travel demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operating & maintenance costs

- 3.2.2.2 Seasonal demand fluctuations

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets in Asia Pacific & Middle East

- 3.2.3.2 Sustainable & eco-friendly yacht innovations

- 3.2.3.3 Membership & subscription model growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - U.S. Coast Guard (USCG)

- 3.4.1.2 Canada - Canadian Coast Guard (CCG)

- 3.4.2 Europe

- 3.4.2.1 Germany - Federal Maritime and Hydrographic Agency (BSH)

- 3.4.2.2 Italy - Corps of the Port Captaincies - Coast Guard

- 3.4.3 Asia Pacific

- 3.4.3.1 Australia - Australian Maritime Safety Authority (AMSA)

- 3.4.3.2 Singapore - Maritime and Port Authority of Singapore (MPA)

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Directorate of Ports and Coasts (DPC)

- 3.4.4.2 Mexico - Direccion General de Marina Mercante

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Dubai Maritime City Authority (DMCA)

- 3.4.5.2 South Africa - South African Maritime Safety Authority (SAMSA)

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 GPS Navigation Systems

- 3.8.1.2 Digital Booking Platforms

- 3.8.1.3 Onboard Safety & Communication Systems

- 3.8.2 Emerging technologies

- 3.8.2.1 Electric & Hybrid Propulsion Systems

- 3.8.2.2 Autonomous Navigation & Pilot Systems

- 3.8.1 Current technologies

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Cost breakdown analysis

- 3.10.1 Acquisition & depreciation costs

- 3.10.2 Operating & fuel expenses

- 3.10.3 Crew salaries & training costs

- 3.10.4 Maintenance, repairs & refits

- 3.10.5 Insurance & regulatory compliance costs

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Marina & port infrastructure analysis

- 3.12.1 Global marina capacity & berth availability

- 3.12.2 Port infrastructure investment trends

- 3.12.3 Regulatory requirements & environmental compliance

- 3.12.4 Emerging destination & infrastructure development

- 3.13 Consumer behavior & booking patterns

- 3.13.1 Seasonal booking trends & peak demand periods

- 3.13.2 Customer acquisition channels & digital conversion rates

- 3.13.3 Repeat customer rates & loyalty program effectiveness

- 3.13.4 Demographic profile & spending patterns by charter type

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Charter, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Bareboat Charter

- 5.3 Crewed Charter

- 5.4 Cabin Charter

- 5.5 Membership/Fractional Ownership Charter

Chapter 6 Market Estimates & Forecast, By Yacht, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Motor Yachts

- 6.3 Sailing Yachts

- 6.4 Catamarans

- 6.5 Mega/Superyachts

- 6.6 Gulets

Chapter 7 Market Estimates & Forecast, By Yacht Length, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Small Yachts (Up to 40 feet)

- 7.3 Mid-Size Yachts (40-80 feet)

- 7.4 Large Yachts (80-120 feet)

- 7.5 Superyachts (Above 120 feet)

Chapter 8 Market Estimates & Forecast, By Booking Duration, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Hourly/Day Charters

- 8.3 Weekly Charters

- 8.4 Extended Charters

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Leisure/Vacation

- 9.3 Corporate/Events

- 9.4 Special Occasions

- 9.5 Adventure/Sports & Fishing

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Croatia

- 10.3.7 Turkey

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Philippines

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Burgess

- 11.1.2 Northrop & Johnson

- 11.1.3 Fraser Yachts

- 11.1.4 Camper & Nicholsons

- 11.1.5 IYC

- 11.1.6 Edmiston

- 11.1.7 Y.CO

- 11.1.8 The Moorings

- 11.1.9 Sunsail

- 11.1.10 Dream Yacht Charter

- 11.1.11 Nicholson Yachts

- 11.1.12 Boatbookings

- 11.2 Regional players

- 11.2.1 CharterWorld

- 11.2.2 Yacht Charter Fleet

- 11.2.3 TMM Yacht Charters

- 11.2.4 Xclusive Yachts

- 11.2.5 Navigare Yachting

- 11.3 Emerging players

- 11.3.1 CKIM

- 11.3.2 Sydney by Sail

- 11.3.3 Interparus