|

市場調查報告書

商品編碼

2027629

磁磚切割機市場機會、成長要素、產業趨勢分析及2026-2035年預測。Sand Tile Saw Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

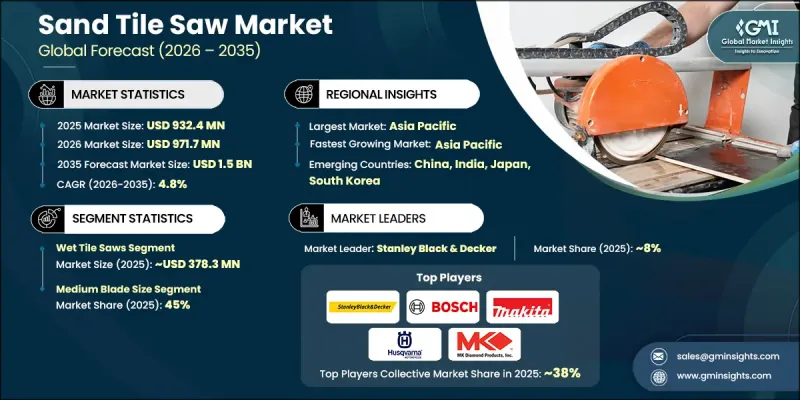

預計到 2025 年,全球磁磚切割機市場價值將達到 9.324 億美元,年複合成長率為 4.8%,到 2035 年將達到 15 億美元。

快速的都市化和住宅建設產業的蓬勃發展,在全球範圍內催生了對瓷磚切割機的巨大需求。隨著都市化的推進,人們不斷需要新的空間來建造住宅、公寓和辦公大樓,磁磚鋪貼也因此成為室內設計中不可或缺的元素。人們在地板、防濺板和浴室翻新等方面投入大量資金。瓷磚切割機能夠對陶瓷、瓷磚甚至石材進行精準且美觀的切割。開發中國家中產階級的壯大,也帶動了住宅翻新維修投資的增加。現代建築方法強調高品質的裝潢效果,而這需要專業的磁磚鋪設服務。除了住宅翻新的增加,DIY熱潮的興起也促使人們購買自己的瓷磚切割機。開發中國家房地產建設的成長,使得瓷磚切割機的需求持續強勁。人們正在尋找堅固耐用、高效節能的瓷磚切割機,以最大限度地減少浪費。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 9.324億美元 |

| 預測金額 | 15億美元 |

| 複合年成長率 | 4.8% |

預計到2025年,濕式磁磚切割機市場規模將達到3.783億美元,並在2026年至2035年間以5.1%的複合年成長率成長。濕式瓷磚切割機憑藉其卓越的切割性能、抑塵功能和刀片冷卻能力,佔據了市場主導地位。濕式磁磚切割機利用水來潤滑刀片並清除碎屑,從而實現更乾淨的切割效果並延長刀片壽命。專業安裝人員更傾向於使用濕式瓷磚切割機來精確切割瓷磚、陶瓷和天然石材。水冷功能可防止刀片過熱,即使切割難加工的材料也能實現連續切割。抑塵功能提高了工作場所的安全性,並符合有關二氧化矽暴露的健康法規。商業建築的成長、對專業瓷磚安裝需求的不斷增加以及對切割品質的日益重視,都在推動濕式瓷磚切割機的普及。在精度、安全性和生產效率方面的技術優勢,使濕式瓷磚切割機成為市場的重要組成部分。

預計到2025年,中型鋸片市佔率將達到45%,並在2026年至2035年間以4.9%的複合年成長率成長。中型鋸片之所以能引領市場,是因為其在住宅和商業瓷磚切割應用上的多功能性。 10至14吋的鋸片可滿足大多數標準磁磚尺寸的需求,同時保持便攜性和設備重量適中。專業安裝人員非常欣賞中型鋸子在切割能力和現場操作靈活性之間的平衡。此尺寸範圍的鋸片適用於住宅和商業安裝中常用的陶瓷、瓷磚和天然石材。中型鋸可提供足夠的切割深度,滿足標準地板材料和牆磚安裝的需求。對能夠處理各種專案類型的多功能設備的需求不斷成長,推動了人們對中型鋸片的青睞。切割能力、便攜性和廣泛的適用性相結合,使中型鋸片成為重要的市場區隔。

美國瓷磚切割機市場預計到2025年將達到2.174億美元,並在2035年之前以5.2%的複合年成長率成長。該地區市場擴張的驅動力包括活躍的建設活動、不斷成長的房屋翻新支出以及人們對住宅維修解決方案日益成長的興趣。成熟的分銷管道和對先進工具的強勁需求持續推動著市場需求,專業用戶和普通消費者都為市場的持續成長做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 快速的都市化和住宅建設的擴張

- 商業建築和基礎設施開發

- DIY住宅維修和改造的趨勢日益成長

- 陷阱與挑戰

- 透過替代切割技術展開競爭

- 建築週期中的經濟敏感度和波動性

- 機會

- 無線和可攜式系統的技術創新

- 對永續和環保建材的需求日益成長

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 價格波動與材料類型和應用有關

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 區域貿易趨勢和跨境流動

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變製造流程。

- 生成式人工智慧的應用案例(設計最佳化、預測性維護)

- 風險、限制和監管考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 濕式磁磚切割機

- 乾式瓷磚切割機

- 可攜式瓷磚切割機

- 固定式磁磚切割機

第6章 市場估計與預測:依葉片尺寸分類,2022-2035年

- 小號(10吋或更小)

- 中號(10-14吋)

- 大號(超過 14 吋)

第7章 市場估計與預測:依產量分類,2022-2035年

- 2馬力或以下

- 2-5馬力

- 超過5馬力

第8章 市場估算與預測:依動力來源,2022-2035年

- 電的

- 電池供電

- 氣體類型

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 工業的

第10章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- Bosch

- DeWalt

- Dremel

- Felker(Target brand)

- Husqvarna

- Lackmond Products

- Makita

- Metabo

- MK Diamond

- QEP

- RIDGID

- Rubi Tools

- Skil

- Stanley Black & Decker

- WEN

The Global Sand Tile Saw Market was valued at USD 932.4 million in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 1.5 billion in 2035.

Rapidly increasing rates of urbanization, along with the increasing rate of growth of the residential construction industry, are creating a demand for sand tile saws globally. The increasing rates of urbanization are creating a constant need to find new spaces to build homes, apartments, and offices, where tile work is an essential part of interior design. People are investing in tile work for floors, backsplashes, bathroom remodelling, etc. Sand tile saws help make precise, clean cuts in ceramic, porcelain, and even stone. The increasing number of people in the middle class in developing countries means a rise in investment in home remodelling and renovation. The modern way of constructing buildings focuses on quality finishes, which require professional tile work. The increasing rate of home remodeling, along with the rise of the DIY movement, encourages people to buy tile saws for their own purposes. The increasing rate of real estate construction in developing countries provides a constant demand for tile saws. People require strong, efficient tile saws to get the work done with minimal waste.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $932.4 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 4.8% |

The wet tile saws segment accounted for USD 378.3 million in 2025 and is anticipated to grow at a CAGR of 5.1% from 2026 to 2035. The wet tile saws segment dominates the market due to superior cutting performance, dust suppression, and blade cooling capabilities. Wet tile saws use water to lubricate the blade and remove cutting debris, resulting in cleaner cuts and longer blade life. Professional contractors prefer wet saws for precision cutting of porcelain, ceramic, and natural stone tiles. Water cooling prevents blade overheating and enables continuous cutting operations on demanding materials. Dust suppression benefits improve workplace safety and comply with health regulations regarding silica exposure. Growing commercial construction, professional tile installation demand, and emphasis on cutting quality drive the adoption of wet tile saws. The technology's advantages in precision, safety, and productivity position wet tile saws as the leading segment in the market

The medium blade size segment held 45% share in 2025 and is anticipated to grow at a CAGR of 4.9% from 2026 to 2035. The medium blade size segment leads the market due to versatility across residential and commercial tile cutting applications. Blades ranging from 10 to 14 inches accommodate most standard tile sizes while maintaining portability and manageable equipment weight. Professional contractors value medium-sized saws that balance cutting capacity with jobsite mobility. The blade size range handles ceramic, porcelain, and natural stone tiles commonly used in residential and commercial installations. Medium saws provide sufficient cutting depth for standard flooring and wall tile applications. Growing demand for versatile equipment that serves multiple project types drives preference for medium blade sizes. The combination of cutting capacity, portability, and broad application suitability positions medium blade saws as the dominant segment in the market.

United States Sand Tile Saw Market reached USD 217.4 million in 2025 and is expected to grow at a CAGR of 5.2% through 2035. Market expansion in the region is supported by strong construction activity, increased renovation spending, and growing interest in home improvement solutions. The presence of well-established distribution channels and a strong preference for advanced tools continue to drive demand, while both professional users and individual consumers contribute to sustained market growth.

Key companies operating in the Global Sand Tile Saw Market include Makita, Husqvarna, Bosch, Rubi Tools, QEP, MK Diamond, RIDGID, Stanley Black & Decker, Skil, WEN, Dremel, Metabo, Lackmond Products, Felker (Target brand), and DeWalt. Companies in the Sand Tile Saw Market are enhancing their competitive position by focusing on innovation, product efficiency, and strategic expansion. Manufacturers are introducing advanced cutting technologies that improve precision, durability, and user safety. Many players are investing in lightweight and portable designs to meet evolving customer preferences. Expanding distribution networks, including online and offline channels, is helping companies improve accessibility and reach a broader customer base. Strategic partnerships and collaborations are also being adopted to strengthen market presence. Additionally, companies are emphasizing after-sales support, training services, and product customization to build long-term relationships with users. Competitive pricing strategies and continuous product upgrades further enable companies to maintain strong positioning in a highly competitive market landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Blade size

- 2.2.3 Power

- 2.2.4 Power source

- 2.2.5 End user

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization and residential construction growth

- 3.2.1.2 Commercial construction and infrastructure development

- 3.2.1.3 Growing DIY home improvement and renovation trends

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Competition from alternative cutting technologies

- 3.2.2.2 Economic sensitivity and construction cycle volatility

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovation in cordless and portable systems

- 3.2.3.2 Growing demand for sustainable and eco-friendly building materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Pricing analysis (driven by primary research)

- 3.6.2 Historical price trend analysis (driven by primary research)

- 3.6.3 Price Variation by material type & application

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Regional trade dynamics & cross-border flow

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of manufacturing processes

- 3.11.2 GenAI uses cases (design optimization, predictive maintenance)

- 3.11.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Wet tile saws

- 5.3 Dry tile saws

- 5.4 Portable tile saws

- 5.5 Stationary tile saws

Chapter 6 Market Estimates & Forecast, By Blade Size, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (up to 10 inches)

- 6.3 Medium (10 to 14 inches)

- 6.4 Large (over 14 inches)

Chapter 7 Market Estimates & Forecast, By Power, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Upto 2 HP

- 7.3 2-5HP

- 7.4 Above 5 HP

Chapter 8 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Battery operated

- 8.4 Gas operated

Chapter 9 Market Estimates & Forecast, By End-use, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Bosch

- 12.2 DeWalt

- 12.3 Dremel

- 12.4 Felker (Target brand)

- 12.5 Husqvarna

- 12.6 Lackmond Products

- 12.7 Makita

- 12.8 Metabo

- 12.9 MK Diamond

- 12.10 QEP

- 12.11 RIDGID

- 12.12 Rubi Tools

- 12.13 Skil

- 12.14 Stanley Black & Decker

- 12.15 WEN