|

市場調查報告書

商品編碼

2027611

純素腸衣市場機會、成長要素、產業趨勢分析及2026-2035年預測Vegan Casing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

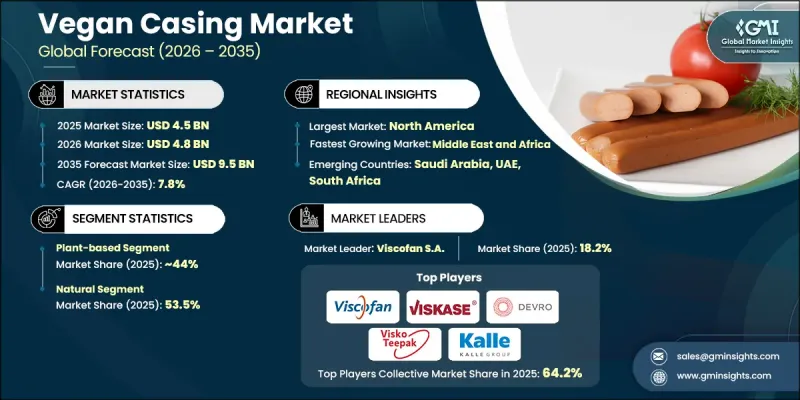

全球素食腸衣市場預計到 2025 年將價值 45 億美元,預計到 2035 年將以 7.8% 的複合年成長率成長至 95 億美元。

隨著消費者對植物來源香腸腸衣的需求不斷成長,市場正穩步擴張。傳統香腸腸衣通常由動物性材料製成。以纖維素、海藻酸鹽和澱粉等植物來源原料製成的純素腸衣,迎合了消費者對無動物成分和永續食品解決方案日益成長的偏好。出於健康意識、環保意識和倫理考量的驅動,人們逐漸轉向純素和素食生活方式,顯著影響市場成長。此外,植物來源食品產業的快速發展也催生了對能夠提升產品品質和性能的創新原料的強勁需求。永續性意識促使製造商採用環保的生產方法和可再生原料。隨著消費者對食品來源及其環境影響的了解不斷加深,市場正轉向「潔淨標示」和「負責任生產」的產品。這些因素,加上食品技術的進步,正使純素腸衣成為更廣泛的植物來源食品生態系中不可或缺的重要組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 45億美元 |

| 預測金額 | 95億美元 |

| 複合年成長率 | 7.8% |

預計到2025年,植物來源產品市佔率將達到44%,並在2035年之前維持7.5%的複合年成長率。由於消費者對肉類替代品和植物來源食品的需求不斷成長,該細分市場持續保持強勁成長勢頭。採用植物來源材料製成的腸衣在滿足食品應用所需功能的同時,也提供了永續且符合倫理的解決方案。它們能夠支持肉類替代品的創新,從而促進其在全球市場的普及,尤其是在人們的飲食偏好不斷向植物來源消費模式轉變的情況下。

到2025年,天然成分將佔53.5%的市場佔有率,這反映出消費者對成分潔淨標示、加工過程少的產品有著強烈的偏好。植物來源的天然成分作為合成材料的替代品,正變得越來越受歡迎。這些材料使製造商能夠開發出符合消費者對永續性、透明度和健康消費期望的產品。隨著食品技術的進步,天然成分在實現理想的質地、耐久性和性能標準方面發揮著至關重要的作用,使其成為持續開發高品質純素腸衣不可或缺的要素。

預計到2025年,北美純素腸衣市場規模將達到17億美元,並在2026年至2035年間以7.4%的複合年成長率成長。這一區域成長主要得益於人們對永續食品實踐的日益關注以及對更健康飲食選擇的偏好。對植物來源加工食品需求的不斷成長,促使生產商不斷創新並拓展產品線。此外,完善的零售基礎設施和分銷網路也為純素腸衣的普及提供了支持,從而推動了全部區域市場的穩步擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 消費者對植物來源食品的需求日益成長

- 人們日益關注環境和倫理問題

- 植物來源材料科學的技術進步

- 產業潛在風險與挑戰

- 與傳統套管相比,生產成本更高

- 可擴充性和生產能力限制。

- 市場機遇

- 亞太地區和拉丁美洲的新興市場

- 食品加工商與腸衣製造商之間的策略夥伴關係

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 植物來源

- 源自大豆蛋白

- 源自豌豆

- 小麥蛋白

- 源自馬鈴薯澱粉

- 其他植物蛋白

- 藻類來源的

- 纖維素衍生的

第6章 市場估計與預測:依來源分類,2022-2035年

- 自然的

- 合成

第7章 市場估價與預測:依產品分類,2022-2035年

- 新鮮的

- 加工產品

第8章 市場估算與預測:依類型分類,2022-2035年

- 預切外殼

- 捲材/片材

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 可食用腸衣

- 不可食用腸衣

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 香腸

- 熱狗

- 莎樂美腸

- 西班牙香腸

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- Devro plc

- Euroduna Food Ingredients GmbH

- Futamura Chemical Co. Ltd.

- Hybricol

- Kalle GmbH

- PROMAR Sp. z oo

- Ruitenberg Ingredients BV

- Soreal

- Viscofan SA

- 維斯卡公司

- ViskoTeepak

The Global Vegan Casing Market was valued at USD 4.5 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 9.5 billion by 2035.

The market is expanding steadily as demand rises for plant-based alternatives to conventional sausage casings, which have traditionally been derived from animal-based materials. Vegan casings are manufactured using plant-derived ingredients such as cellulose, alginate, and starch, aligning with the increasing consumer preference for cruelty-free and sustainable food solutions. The shift toward vegan and vegetarian lifestyles, driven by health awareness, environmental concerns, and ethical considerations, is significantly influencing market growth. In addition, the rapid evolution of the plant-based food industry is creating strong demand for innovative ingredients that enhance product quality and performance. Growing awareness of sustainability is encouraging manufacturers to adopt eco-friendly production methods and renewable raw materials. As consumers become more informed about food sourcing and environmental impact, the market is witnessing a transition toward clean-label and responsibly produced products. These factors, combined with advancements in food technology, are positioning vegan casings as a key component in the broader plant-based food ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.5 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 7.8% |

The plant-based segment accounted for 44% share in 2025 and is expected to grow at a CAGR of 7.5% through 2035. This segment continues to gain traction due to increasing demand for meat alternatives and plant-based food products. Casings developed from plant-derived materials offer a sustainable and ethical solution while maintaining the functional properties required for food applications. Their ability to support product innovation in meat alternatives is contributing to their growing adoption across global markets, particularly as dietary preferences continue to evolve toward plant-based consumption patterns.

The natural segment held a share of 53.5% in 2025, reflecting strong consumer preference for minimally processed and clean-label ingredients. Natural raw materials sourced from plant origins are becoming increasingly popular as alternatives to synthetic options. These materials enable manufacturers to develop products that align with consumer expectations for sustainability, transparency, and health-conscious consumption. As food technology advances, natural ingredients are playing a critical role in achieving desired texture, durability, and performance standards, making them essential for the continued development of high-quality vegan casings.

North America Vegan Casing Market was valued at USD 1.7 billion in 2025 and is anticipated to grow at a CAGR of 7.4% from 2026 to 2035. Growth in the region is being driven by increasing awareness of sustainable food practices and a rising preference for healthier dietary choices. The demand for plant-based processed food products is encouraging manufacturers to innovate and expand their product offerings. Additionally, strong retail infrastructure and distribution networks are supporting the widespread adoption of vegan casings, enabling consistent market expansion across the region.

Key companies operating in the Global Vegan Casing Market include Devro plc, Euroduna Food Ingredients GmbH, Futamura Chemical Co. Ltd., Hybricol, Kalle GmbH, and PROMAR Sp. z o.o., Ruitenberg Ingredients B.V., Soreal, Viscofan S.A., Viskase Companies Inc., and ViskoTeepak. Companies in the Global Vegan Casing Market are strengthening their competitive position through innovation, sustainability initiatives, and strategic collaborations. They are investing in research and development to create advanced plant-based materials that improve product performance, durability, and texture. Many players are focusing on sourcing renewable raw materials and implementing eco-friendly manufacturing processes to meet growing environmental expectations. Partnerships with food manufacturers are helping expand application areas and accelerate product adoption. In addition, companies are enhancing their distribution channels and expanding into emerging markets to increase their global presence. Customization of products to meet specific client requirements and continuous improvement in quality standards are further enabling companies to differentiate themselves and maintain long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Source

- 2.2.4 Product

- 2.2.5 Form

- 2.2.6 End use

- 2.2.7 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based food products

- 3.2.1.2 Growing awareness of environmental & ethical concerns

- 3.2.1.3 Technological advancements in plant-based material science

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs compared to traditional casings

- 3.2.2.2 Limited scalability & production capacity constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets in Asia Pacific & Latin America

- 3.2.3.2 Strategic partnerships between food processors & casing manufacturers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based

- 5.2.1 Soy protein-based

- 5.2.2 Pea protein-based

- 5.2.3 Wheat protein-based

- 5.2.4 Potato starch-based

- 5.2.5 Other plant proteins

- 5.3 Algae-based

- 5.4 Cellulose-based

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural

- 6.3 Synthetic

Chapter 7 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Fresh

- 7.3 Processed

Chapter 8 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pre-cut casings

- 8.3 Rolls/sheets

Chapter 9 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Edible casings

- 9.3 Non-edible casings

Chapter 10 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Sausages

- 10.3 Hot dogs

- 10.4 Salami

- 10.5 Chorizo

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Devro plc

- 12.2 Euroduna Food Ingredients GmbH

- 12.3 Futamura Chemical Co. Ltd.

- 12.4 Hybricol

- 12.5 Kalle GmbH

- 12.6 PROMAR Sp. z o.o.

- 12.7 Ruitenberg Ingredients B.V.

- 12.8 Soreal

- 12.9 Viscofan S.A.

- 12.10 Viskase Companies Inc.

- 12.11 ViskoTeepak