|

市場調查報告書

商品編碼

2027601

水冷式電動車充電電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測。Liquid-Cooled EV Charging Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

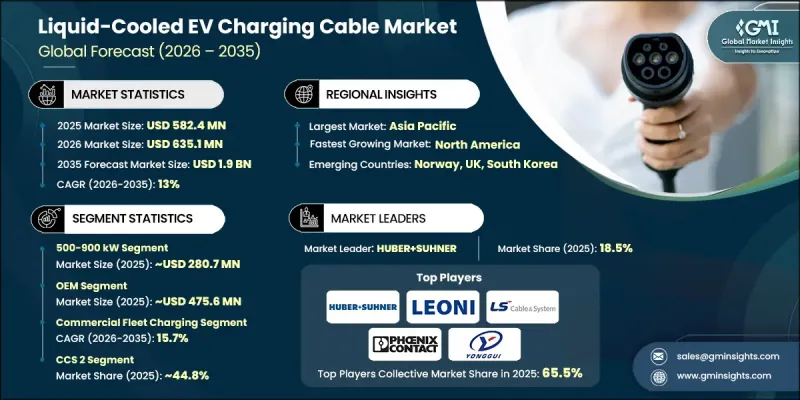

預計到 2025 年,全球水冷式電動車充電電纜市場規模將達到 5.824 億美元,年複合成長率為 13%,到 2035 年將達到 19 億美元。

市場擴張的驅動力來自於電動車的快速普及和對超快充電能力日益成長的需求。隨著充電技術向高功率發展,對能夠承受高負載電力的先進電纜系統的需求也隨之增加。液冷電纜專為應對這些高功率等級而設計,即使在快速充電過程中也能確保效率、安全性和穩定性。高容量充電基礎設施的擴展正在推動需求成長,尤其是在下一代充電系統旨在大幅縮短充電時間的情況下。同時,支持性的法規結構和政策舉措正在加速先進電動車基礎設施的建設。向高壓車輛架構的轉變進一步凸顯了這些電纜的重要性,因為它們能夠在保持熱穩定性的同時實現更快的能量傳輸。此外,乘用車和商用車領域日益成長的電氣化需求正在持續推動高性能充電解決方案的發展,而液冷電纜技術正逐漸成為未來電動車生態系統的關鍵組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 5.824億美元 |

| 預計金額 | 19億美元 |

| 複合年成長率 | 13% |

500-900kW功率段佔48.2%的市場佔有率,預計到2025年市場規模將達到2.807億美元。在預測期內,此功率段預計將實現最快成長,主要驅動力是市場對高容量充電系統的需求不斷成長,以滿足配備更大容量電池系統的先進電動車的能源需求。隨著人們對縮短充電時間的日益重視,高功率充電基礎設施的部署正在加速,其中液冷電纜在溫度控管和維持運作效率方面發揮著至關重要的作用。隨著電動車的普及,此功率段有望繼續成為整體市場成長的主要驅動力,因為它能夠滿足快速充電的需求。

預計到2025年,OEM廠商將佔據81.7%的市場佔有率,市場規模將達到4.756億美元。這一主導地位主要歸功於OEM廠商在設計和提供與其汽車平臺相匹配的充電解決方案方面發揮的關鍵作用。這些製造商正積極整合先進的充電技術,以確保最佳性能和用戶便利性。由於水冷式電纜能夠有效率地支援高功率充電,因此在這些系統中正得到越來越廣泛的應用。隨著對高性能電動車的需求持續成長,OEM廠商更加重視車輛開發與充電基礎設施的整合,從而增強了其市場影響力。

美國水冷式電動車充電線纜市場預計到2025年將達到1.133億美元,並在2026年至2035年間以14%的複合年成長率成長。美國強勁的政策環境,尤其是旨在促進電動車普及和擴大充電基礎設施的政策,為市場成長提供了有力支撐。用於部署快速充電網路的投資也顯著推動了市場發展。零排放出行方式的日益普及和電動車產量的不斷成長,進一步推動了對先進充電解決方案的需求。此外,商用車輛的電氣化程度不斷提高,也對能夠實現快速高效充電的高性能線纜產生了巨大需求,鞏固了美國作為水冷式電動車充電技術領先市場的地位。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對超快速充電和兆瓦級充電基礎設施的需求日益成長

- 擴大800V電動車平台架構的應用

- 需要加強高功率充電中的溫度控管

- 政府制定法規和獎勵以發展電動車充電基礎設施

- 產業潛在風險與挑戰

- 系統複雜性與特殊維護需求

- 冷卻液洩漏風險及環境問題

- 市場機遇

- 現有充電站維修升級的市場

- 重型卡車和商用車隊電氣化進展

- 開發用於長途運輸的兆瓦級充電系統(MCS)。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國 - SAE J3400

- 美國-J1772

- 美國 - NEVI 計畫要求

- 歐洲

- 歐盟(EU)- 歐盟泛歐交通運輸網(TEN-T)法規

- 歐盟 - 碳捕獲與封存指令

- 亞太地區

- 日本 - CHAdeMO 3.0

- 中國-GB/T

- 拉丁美洲

- 巴西——ANEEL法律規範

- 墨西哥 - 電動車充電設備實施舉措

- 中東和非洲

- 阿拉伯聯合大公國 - 國家電動車政策

- 阿拉伯聯合大公國 - 杜拜/阿布達比電動車充電網路法規

- 北美洲

- 投資與資金籌措分析

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 800V高壓電動車平台

- 兆瓦充電系統(MCS)

- 先進的溫度控管系統

- 新興技術

- 使用介電冷卻劑的充電電纜

- 超快速重型卡車充電解決方案

- 目前技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 專利趨勢(基於初步調查)

- 用例分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量和進出口額的趨勢

- 主要貿易走廊及關稅的影響

- 專利趨勢(基於初步調查)

- 成本細分分析

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的已安裝產能

- 設備運轉率和擴建計劃

- 永續性和環境影響

- 環境影響評估

- 社會影響和對社區的益處

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、局限性和監管考量

- 超快速充電網路快速擴張

- 幹線公路走廊的部署策略

- 適用於商業和車隊用途的超快速充電中心

- 官民合作關係(PPP)與投資模式

- 技術標準化和互通性

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依有線電視電力容量分類,2022-2035年

- 300~499 kW

- 500~900 kW

- 超過900千瓦

第6章 市場估算與預測:依電纜長度分類,2022-2035年

- 小於5米

- 6-10米

- 超過10米

第7章 市場估算與預測:依電纜直徑分類,2022-2035年

- 小於 30 毫米

- 30~50 mm

- 超過 50 毫米

第8章 市場估算與預測:依導體材料分類,2022-2035年

- 銅

- 鋁

第9章 市場估算與預測:依連接器類型分類,2022-2035年

- Type 1

- Type 2

- CCS1

- CCS2

- CHAdeMO

- 其他

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 公共充電站

- 商業車隊充電

- 住宅/個人充電

- 高速公路和長途充電網路

第11章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 挪威

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 菲律賓

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界公司

- Phoenix Contact

- HUBER+SUHNER

- LEONI

- Sinbon Electronics

- KemPower

- ABB

- LS Cable &System

- Southwire Company

- ITT Canon

- Colder Products Company

- Amphenol Energy

- Coroflex

- 當地公司

- OMG EV Cable

- MIDA Power

- Zhejiang Yonggui

- Suzhou Yihang

- Qingdao Penoda Electrical

- 新興企業

- BRUGG eConnect

- Teison Energy

- Caledonian Cables

The Global Liquid-Cooled EV Charging Cable Market was valued at USD 582.4 million in 2025 and is estimated to grow at a CAGR of 13% to reach USD 1.9 billion by 2035.

Market expansion is fueled by the accelerating adoption of electric vehicles and the rising requirement for ultra-fast charging capabilities. As charging technologies evolve toward higher power outputs, the need for advanced cable systems capable of handling substantial electrical loads continues to intensify. Liquid-cooled cables are engineered to support these elevated power levels, ensuring efficiency, safety, and consistent performance during high-speed charging sessions. Increasing deployment of high-capacity charging infrastructure is reinforcing demand, particularly as next-generation charging systems aim to significantly reduce charging times. In parallel, supportive regulatory frameworks and policy initiatives are encouraging the development of advanced EV infrastructure. The transition toward high-voltage vehicle architectures is further amplifying the importance of these cables, as they enable faster energy transfer while maintaining thermal stability. Additionally, the expansion of electrified transportation across passenger and commercial segments is creating sustained demand for high-performance charging solutions, positioning liquid-cooled cable technology as a critical component of future-ready EV ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $582.4 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 13% |

The 500-900 kW segment held a 48.2% share, generating USD 280.7 million in 2025. This segment is also projected to witness the fastest growth over the forecast period, supported by the increasing demand for high-capacity charging systems capable of meeting the energy needs of advanced electric vehicles equipped with larger battery systems. The growing emphasis on reducing charging duration has accelerated the deployment of high-power charging infrastructure, where liquid-cooled cables play a crucial role in managing heat and maintaining operational efficiency. As the electric vehicle landscape continues to expand, this segment is expected to remain a key contributor to overall market growth due to its ability to support rapid charging requirements.

The OEM segment accounted for 81.7% share in 2025 generating USD 475.6 million. Its dominance is primarily driven by the integral role of original equipment manufacturers in designing and delivering compatible charging solutions tailored to their vehicle platforms. These manufacturers are actively integrating advanced charging technologies to ensure optimal performance and user convenience. Liquid-cooled cables are increasingly being incorporated into these systems due to their capability to support high-power charging efficiently. As demand for high-performance electric vehicles continues to rise, OEMs are placing greater emphasis on aligning vehicle development with charging infrastructure, thereby strengthening their influence within the market.

U.S. Liquid-Cooled EV Charging Cable Market was valued at USD 113.3 million in 2025 and is anticipated to grow at a CAGR of 14% from 2026 to 2035. Growth in the United States is being supported by a strong policy environment focused on accelerating electric vehicle adoption and expanding charging infrastructure. Investments aimed at deploying high-speed charging networks are contributing significantly to market development. The increasing shift toward zero-emission mobility, along with the scaling production of electric vehicles, is further boosting the need for advanced charging solutions. Additionally, the rising electrification of commercial fleets is creating substantial demand for high-performance cables capable of supporting fast and efficient charging, reinforcing the country's position as a key market for liquid-cooled EV charging technologies.

Key companies operating in the Global Liquid-Cooled EV Charging Cable Market include ABB, Amphenol Energy, BRUGG eConnect, HUBER+SUHNER, LEONI, LS Cable & System, MIDA Power, Phoenix Contact, Sinbon Electronics, and Zhejiang Yonggui. Companies in the Global Liquid-Cooled EV Charging Cable Market are focusing on innovation, strategic partnerships, and infrastructure expansion to strengthen their market position. They are investing in advanced cooling technologies and high-performance materials to enhance cable efficiency and durability under extreme power conditions. Collaborations with automotive manufacturers and charging network providers are helping firms expand their reach and ensure compatibility with next-generation EV platforms. Many players are also scaling production capabilities to meet growing global demand while optimizing supply chains for cost efficiency. In addition, companies are targeting new geographic markets and aligning their offerings with evolving regulatory standards. Continuous research and development efforts, along with customization of solutions for specific applications, are enabling firms to differentiate themselves and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cable power capacity

- 2.2.3 Cable length

- 2.2.4 Cable diameter

- 2.2.5 Conductor material

- 2.2.6 Connector

- 2.2.7 Application

- 2.2.8 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for ultrafast & megawatt charging infrastructure

- 3.2.1.2 Growing adoption of 800V EV platform architectures

- 3.2.1.3 Need for enhanced thermal management in high-power charging

- 3.2.1.4 Government mandates & incentives for EV charging infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 System complexity & specialized maintenance requirements

- 3.2.2.2 Coolant leak risks & environmental concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit & upgrade market for existing charging stations

- 3.2.3.2 Increasing heavy-duty truck & commercial fleet electrification

- 3.2.3.3 Megawatt Charging System (MCS) development for long-haul transport

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US - SAE J3400

- 3.4.1.2 US - J1772

- 3.4.1.3 US - NEVI Program Requirements

- 3.4.2 Europe

- 3.4.2.1 European Union - EU TEN-T Regulations

- 3.4.2.2 European Union - CCS Mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan - CHAdeMO 3.0

- 3.4.3.2 China - GB/T

- 3.4.4 Latin America

- 3.4.4.1 Brazil - ANEEL EV Charging Regulatory Framework

- 3.4.4.2 Mexico - EVSE Deployment Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - National Electric Vehicle Policy

- 3.4.5.2 UAE - Dubai/Abu Dhabi EV Charging Network Regulations

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 800V High-Voltage EV Platforms

- 3.8.1.2 Megawatt Charging Systems (MCS)

- 3.8.1.3 Advanced Thermal Management Systems

- 3.8.2 Emerging technologies

- 3.8.2.1 Dielectric Coolant-Based Charging Cables

- 3.8.2.2 Ultra-Fast Heavy-Duty Truck Charging Solutions

- 3.8.1 Current technologies

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Use case analysis

- 3.12 Pricing analysis (Driven by Primary Research)

- 3.12.1 Historical price trend analysis

- 3.12.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.13 Trade data analysis (Driven by Paid Database)

- 3.13.1 Import/export volume & value trends

- 3.13.2 Key trade corridors & tariff impact

- 3.14 Patent landscape (Driven by Primary Research)

- 3.15 Cost breakdown analysis

- 3.16 Capacity & Production Landscape (Driven by Primary Research)

- 3.16.1 Installed Capacity by Region & Key Producer

- 3.16.2 Capacity Utilization Rates & Expansion Pipelines

- 3.17 Sustainability and environmental impact

- 3.17.1 Environmental impact assessment

- 3.17.2 Social impact & community benefits

- 3.17.3 Governance & corporate responsibility

- 3.17.4 Sustainable finance & investment trends

- 3.18 Impact of AI and Generative AI on the market

- 3.18.1 AI-driven disruption of existing business models

- 3.18.2 GenAI use cases & adoption roadmap by segment

- 3.18.3 Risks, limitations & regulatory considerations

- 3.19 Rapid expansion of ultra-fast charging networks

- 3.19.1 Highway corridor deployment strategies

- 3.19.2 Commercial and fleet-oriented ultra-fast hubs

- 3.19.3 Public-private partnerships (PPPs) and investment models

- 3.19.4 Technological standardization and interoperability

- 3.20 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.20.1 Base Case - Key macro & industry variables driving CAGR

- 3.20.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.20.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Cable Power Capacity, 2022 - 2035 ($ Million, Units)

- 5.1 Key trends

- 5.2 300-499 kW

- 5.3 500-900 kW

- 5.4 Above 900 kW

Chapter 6 Market Estimates and Forecast, By Cable Length, 2022 - 2035 ($ Million, Units)

- 6.1 Key trends

- 6.2 Upto 5 meters

- 6.3 6-10 meters

- 6.4 Above 10 meters

Chapter 7 Market Estimates and Forecast, By Cable Diameter, 2022 - 2035 ($ Million, Units)

- 7.1 Key trends

- 7.2 Below 30 mm

- 7.3 30-50 mm

- 7.4 Above 50 mm

Chapter 8 Market Estimates and Forecast, By Conductor Material, 2022 - 2035 ($ Million, Units)

- 8.1 Key trends

- 8.2 Copper

- 8.3 Aluminium

Chapter 9 Market Estimates and Forecast, By Connector, 2022 - 2035 ($ Million, Units)

- 9.1 Key trends

- 9.2 Type 1

- 9.3 Type 2

- 9.4 CCS1

- 9.5 CCS2

- 9.6 CHAdeMO

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million, Units)

- 10.1 Key trends

- 10.2 Public Charging Stations

- 10.3 Commercial Fleet Charging

- 10.4 Residential / Private Charging

- 10.5 Highway and Long-Distance Charging Networks

Chapter 11 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Million, Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Million, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Netherlands

- 12.3.8 Norway

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Philippines

- 12.4.9 Vietnam

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Phoenix Contact

- 13.1.2 HUBER+SUHNER

- 13.1.3 LEONI

- 13.1.4 Sinbon Electronics

- 13.1.5 KemPower

- 13.1.6 ABB

- 13.1.7 LS Cable & System

- 13.1.8 Southwire Company

- 13.1.9 ITT Canon

- 13.1.10 Colder Products Company

- 13.1.11 Amphenol Energy

- 13.1.12 Coroflex

- 13.2 Regional players

- 13.2.1 OMG EV Cable

- 13.2.2 MIDA Power

- 13.2.3 Zhejiang Yonggui

- 13.2.4 Suzhou Yihang

- 13.2.5 Qingdao Penoda Electrical

- 13.3 Emerging players

- 13.3.1 BRUGG eConnect

- 13.3.2 Teison Energy

- 13.3.3 Caledonian Cables

電動車充電線纜市場-2026-2032年全球市場預測

電動車充電線纜市場-2026-2032年全球市場預測 電動車充電線市場分析及預測(至2035年):按類型、產品、技術、組件、應用、材料類型、最終用戶、功能、安裝類型、設備分類

電動車充電線市場分析及預測(至2035年):按類型、產品、技術、組件、應用、材料類型、最終用戶、功能、安裝類型、設備分類 電動車充電線市場預測至2034年-全球分析(按充電等級、充電模式、線材類型、線材形狀、護套材料、輸出功率、安裝配置、車輛類型、電源、銷售管道、應用和地區分類)

電動車充電線市場預測至2034年-全球分析(按充電等級、充電模式、線材類型、線材形狀、護套材料、輸出功率、安裝配置、車輛類型、電源、銷售管道、應用和地區分類) 電動車充電線市場規模、佔有率和成長分析:按電纜類型、充電線類型、連接器類型、直徑、材質、長度和地區分類-2026-2033年產業預測

電動車充電線市場規模、佔有率和成長分析:按電纜類型、充電線類型、連接器類型、直徑、材質、長度和地區分類-2026-2033年產業預測 2026年全球電動車充電線市場報告

2026年全球電動車充電線市場報告 電動車充電線市場機會、成長要素、產業趨勢分析及2026-2035年預測

電動車充電線市場機會、成長要素、產業趨勢分析及2026-2035年預測 下一代電動車充電線市場:策略性洞察與預測(2026-2031)全球電動車充電線市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

下一代電動車充電線市場:策略性洞察與預測(2026-2031)全球電動車充電線市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 全球液冷式電動車充電電纜市場:按電纜能量、電纜長度、電纜直徑、應用、覆材、冷卻劑和地區分類的2032年預測2026年全球USB-C充電線市場報告

全球液冷式電動車充電電纜市場:按電纜能量、電纜長度、電纜直徑、應用、覆材、冷卻劑和地區分類的2032年預測2026年全球USB-C充電線市場報告