|

市場調查報告書

商品編碼

2027594

工業噴墨印表機市場機會、成長要素、產業趨勢分析及2026-2035年預測。Industrial Inkjet Printers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

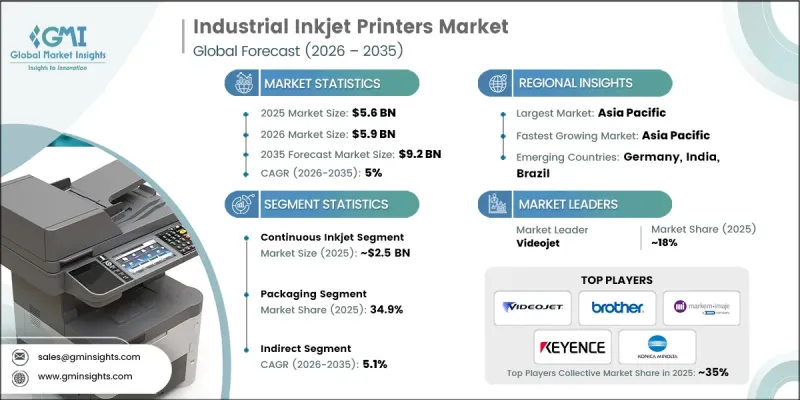

2025年全球工業噴墨印表機市場價值為56億美元,預計到2035年將以5%的複合年成長率成長至92億美元。

包裝、紡織和製藥行業的製造商正在推動可變數據列印技術的發展,以滿足不斷變化的業務需求。這些印表機能夠在多種承印物上高解析度列印批號、條碼、日期和序號,無需對設備進行大規模改造即可柔軟性處理小批量生產。工業噴墨系統因其成本效益、運作效率以及與永續生產實踐的兼容性而備受關注,這些實踐能夠減少廢棄物和能源消耗。印字頭技術的進步、創新的墨水配方以及智慧製造解決方案的整合顯著提高了列印品質。高解析度列印能力使製造商能夠滿足監管標準、增強產品可追溯性並實現卓越的市場差異化,噴墨技術已成為現代工業生產的關鍵驅動力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 56億美元 |

| 預測金額 | 92億美元 |

| 複合年成長率 | 5% |

預計到2025年,連續噴墨(CIJ)市場規模將達到25億美元,並在2026年至2035年間以5.3%的複合年成長率成長。 CIJ技術因其高速、非接觸式列印功能而被廣泛採用,能夠列印批號、有效期限和條碼等動態資訊。其高可靠性使其能夠以極低的維護成本實現連續運作,因此非常適合對生產效率和效率要求高的行業,例如食品飲料、製藥、汽車和一般製造業。

到2025年,包裝產業將佔據34.9%的市場。工業噴墨印表機是包裝流程中不可或缺的設備,可提供批號列印、日期列印、條碼列印和追溯等關鍵功能。它們可在多種材料上列印,包括瓦楞紙板、塑膠、金屬和薄膜。憑藉其精準性、適應性和可靠性,這些印表機在對準確性和合規性要求極高的現代包裝流程中不可或缺。

美國工業噴墨印表機市場預計到2025年將達到7億美元,並在2035年之前以5.6%的複合年成長率成長。美國先進的製造業基礎設施和自動化領域的領先地位正在推動電子、製藥和食品加工行業採用噴墨系統。這些印表機支援編碼、標記和標籤流程,同時確保生產效率穩定,最大限度地減少停機時間,並與現有生產線無縫整合。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響價值鏈的因素

- 零件供應商

- 工業噴墨印表機製造商

- 系統整合商和分銷商

- 終端用戶製造工廠

- 售後服務和維護提供者

- 每個階段增加的價值

- 影響產業的因素

- 促進因素

- 對可追溯性和防偽解決方案的需求日益成長

- 關於產品標籤的嚴格監管要求

- 電子商務的成長正在推動包裝和物流領域對程式設計的需求。

- 市場陷阱

- 工業系統需要大量的初始資本投資

- 非多孔基材上油墨附著力的挑戰

- 機會

- 新興市場的工業化

- 智慧包裝的整合

- 藥品序列化管理條例

- 開發永續和環保油墨

- 促進因素

- 成長潛力分析

- 監理情勢

- 食品安全現代化法案(FSMA)

- FDA 21 CFR 第 11 部分 - 藥品生產標準

- 歐盟食品資訊條例(歐盟)第1169號 2011

- 條碼和序列化的GS1標準

- 環境法規

- 關鍵市場趨勢與轉型

- 科技與創新趨勢

- 印字頭技術的進步

- 油墨配方創新

- 可變資料列印和序列化能力

- 與工業4.0的整合

- 高速列印技術的發展

- 2025年價格分析

- 按地區

- 對過去價格趨勢的分析(基於初步研究)

- 根據球員類型(高階/超值/成本加成)制定的定價策略(基於初步研究)

- 區域價格波動

- 原物料成本對價格的影響

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

- 供應鏈分析

- 印字頭供應集中

- 油墨供應鏈結構

- 區域採購模式

- 供應鏈脆弱性與風險緩解策略

- 貿易資料分析(基於付費資料庫)(HS編碼:84433250)

- 進出口數量和價值趨勢(基於初步調查)(2019-2024 年)

- 主要貿易路線及關稅的影響(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 利用人工智慧演算法進行預測性維護

- 即時品管和缺陷檢測

- 人工智慧最佳化油墨配方和基材匹配

- 自動化工作流程和與生產線的整合

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的運作產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依技術分類,2022-2035年

- 連續噴墨

- 點播串流媒體

- UV噴墨

- 其他

第6章 市場估計與預測:依最終用途產業分類,2022-2035年

- 食品/飲料

- 瓶裝和罐頭飲料

- 加工食品

- 生鮮食品的標籤

- 化學

- 工業化學品容器的標記

- 農藥包裝

- 特種化學品的標籤

- 製藥

- 處方藥包裝

- 非處方藥市場

- 醫療設備的標記

- 包裝

- 個人護理和化妝品

- 其他(汽車等)

第7章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第9章:公司簡介

- Brother Industries

- Canon

- Domino Printing Sciences

- Durst Phototechnik

- Electronics For Imaging

- Epson

- Fujifilm

- Hitachi Industrial Equipment Systems

- HP

- Keyence

- Konica Minolta

- Leibinger Group

- Markem-Imaje

- Mitsubishi Heavy Industries Printing &Packaging Machinery

- Videojet

The Global Industrial Inkjet Printers Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 9.2 billion by 2035.

Demand is driven by manufacturers across the packaging, textiles, and pharmaceutical industries who are increasingly using variable data printing to meet evolving business requirements. These printers allow for high-resolution printing of batch codes, barcodes, dates, and serial numbers on multiple substrates, offering flexibility for short production runs without extensive retooling. Industrial inkjet systems are gaining traction due to their cost-effectiveness, operational efficiency, and alignment with sustainable manufacturing practices, which reduce waste and energy consumption. Technological advancements in printheads, innovative ink formulations, and the integration of smart manufacturing solutions have significantly improved print quality. High-resolution printing capabilities now enable manufacturers to meet regulatory standards, enhance product traceability, and achieve superior marketing differentiation, making inkjet technology a key enabler of modern industrial production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $9.2 Billion |

| CAGR | 5% |

The continuous inkjet (CIJ) segment generated USD 2.5 billion in 2025 and is expected to grow at a CAGR of 5.3% between 2026 and 2035. CIJ technology is widely adopted for its high-speed, non-contact printing ability, supporting dynamic information such as batch numbers, expiration dates, and barcodes. Its reliability in continuous operations with minimal maintenance makes it ideal for industries that demand high productivity and efficiency, including food and beverage, pharmaceuticals, automotive, and general manufacturing.

The packaging segment held an 34.9% share in 2025. Industrial inkjet printers are integral to packaging operations, providing essential functions such as batch coding, date marking, barcoding, and traceability. They can print on a variety of substrates including cardboard, plastic, metal, and film. The combination of precision, adaptability, and reliability has made these printers indispensable for modern packaging processes that demand accuracy and regulatory compliance.

U.S. Industrial Inkjet Printers Market reached USD 0.7 billion in 2025 and is expected to grow at a CAGR of 5.6% through 2035. The country's advanced manufacturing infrastructure and leadership in automation drive the adoption of inkjet systems across electronics, pharmaceuticals, and food processing industries. These printers support coding, marking, and labeling processes while ensuring consistent productivity, minimizing downtime, and integrating seamlessly with existing production lines.

Key players in the Global Industrial Inkjet Printers Market include Epson, HP, Domino Printing Sciences, Fujifilm, Konica Minolta, Videojet, Hitachi Industrial Equipment Systems, Canon, Markem-Imaje, Brother Industries, Durst Phototechnik, Leibinger Group, Mitsubishi Heavy Industries Printing & Packaging Machinery, and Electronics For Imaging. Companies in the Industrial Inkjet Printers Market are strengthening their position through product innovation, developing high-resolution and high-speed printing systems suitable for diverse industrial applications. They are expanding their portfolios with specialized inks and substrates to meet regulatory and environmental standards. Strategic partnerships and collaborations enhance distribution networks and provide localized technical support, while investment in research and development ensures the integration of AI and smart manufacturing capabilities. Firms are also focusing on cost efficiency and sustainability to attract environmentally conscious clients and improve operational productivity, solidifying their market presence globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Research Trail & confidence scoring

- 1.7.1 Research trail components

- 1.7.2 Scoring components

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Component suppliers

- 3.1.3 Industrial inkjet printer manufacturers

- 3.1.4 System integrators & distributors

- 3.1.5 End-user manufacturing facilities

- 3.1.6 After-sales service & maintenance providers

- 3.1.7 Value addition at each stage

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for traceability & anti-counterfeiting solutions

- 3.2.1.2 Stringent regulatory requirements for product marking

- 3.2.1.3 E-commerce growth driving packaging & logistics coding demand

- 3.2.2 Market pitfalls

- 3.2.2.1 High initial capital investment for industrial-grade systems

- 3.2.2.2 Ink adhesion challenges on non-porous substrates

- 3.2.3 Opportunities

- 3.2.3.1 Emerging markets industrialization

- 3.2.3.2 Smart packaging integration

- 3.2.3.3 Pharmaceutical serialization mandates

- 3.2.3.4 Sustainable & eco-friendly ink development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Food Safety Modernization Act (FSMA)

- 3.4.2 FDA 21 CFR Part 11 - pharmaceutical marking standards

- 3.4.3 EU Food Information Regulation (EU) No. 1169/2011

- 3.4.4 GS1 standards for barcoding & serialization

- 3.4.5 Environmental regulations

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Printhead technology advancements

- 3.6.2 Ink formulation innovations

- 3.6.3 Variable data printing & serialization capabilities

- 3.6.4 Industry 4.0 integration

- 3.6.5 High-speed printing technology evolution

- 3.7 Pricing analysis, 2025

- 3.7.1 By region

- 3.7.2 Historical price trend analysis (driven by primary research)

- 3.7.3 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7.4 Regional price variation

- 3.7.5 Impact of raw material costs on pricing

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTLE analysis

- 3.11 Supply chain analysis

- 3.11.1 Printhead supply concentration

- 3.11.2 Ink supply chain structure

- 3.11.3 Geographic sourcing patterns

- 3.11.4 Supply chain vulnerabilities & mitigation strategies

- 3.12 Trade Data Analysis (Driven by paid database) (HS code- 84433250)

- 3.12.1 Import/Export Volume & Value Trends (Driven by Primary Research) (2019-2024)

- 3.12.2 Key trade corridors & tariff impact (driven by primary research)

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.2.1 Predictive maintenance using ai algorithms

- 3.13.2.2 Real-time quality control & defect detection

- 3.13.2.3 AI-optimized ink formulation & substrate matching

- 3.13.2.4 Automated workflow & production line integration

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (driven by primary research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipeline

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Continuous inkjet

- 5.3 Drop on demand

- 5.4 UV inkjet

- 5.5 Other

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.2.1 Beverage bottling & canning

- 6.2.2 Packaged food

- 6.2.3 Fresh produce labeling

- 6.3 Chemical

- 6.3.1 Industrial chemical container marking

- 6.3.2 Agrochemical packaging

- 6.3.3 Specialty chemical labeling

- 6.4 Pharmaceutical

- 6.4.1 Prescription drug packaging

- 6.4.2 OTC medication marking

- 6.4.3 Medical device marking

- 6.5 Packaging

- 6.6 Personal care & cosmetics

- 6.7 Others (automotive, etc.)

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Brother Industries

- 9.2 Canon

- 9.3 Domino Printing Sciences

- 9.4 Durst Phototechnik

- 9.5 Electronics For Imaging

- 9.6 Epson

- 9.7 Fujifilm

- 9.8 Hitachi Industrial Equipment Systems

- 9.9 HP

- 9.10 Keyence

- 9.11 Konica Minolta

- 9.12 Leibinger Group

- 9.13 Markem-Imaje

- 9.14 Mitsubishi Heavy Industries Printing & Packaging Machinery

- 9.15 Videojet

工業噴墨印表機市場:依列印技術、墨水類型、解析度、材料、列印架構、應用和最終用戶產業分類-2026-2032年全球市場預測工業數位印刷機市場:依印刷機類型、印刷技術、油墨類型、操作模式、印刷寬度、應用和銷售管道,全球預測,2026-2032年攜帶式噴墨印表機市場:按技術、墨水類型、應用、最終用戶和分銷管道分類,全球預測,2026-2032年

工業噴墨印表機市場:依列印技術、墨水類型、解析度、材料、列印架構、應用和最終用戶產業分類-2026-2032年全球市場預測工業數位印刷機市場:依印刷機類型、印刷技術、油墨類型、操作模式、印刷寬度、應用和銷售管道,全球預測,2026-2032年攜帶式噴墨印表機市場:按技術、墨水類型、應用、最終用戶和分銷管道分類,全球預測,2026-2032年 2026-2034年全球工業噴墨印表機市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球工業噴墨印表機市場規模、佔有率、趨勢和成長分析報告 工業印表機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

工業印表機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 工業噴墨印表機市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、行業和地理位置

工業噴墨印表機市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、行業和地理位置 2030 年工業噴墨印表機市場預測:按機器類型、包裝類型、技術、分銷管道、應用、最終用戶和地區進行的全球分析

2030 年工業噴墨印表機市場預測:按機器類型、包裝類型、技術、分銷管道、應用、最終用戶和地區進行的全球分析