|

市場調查報告書

商品編碼

2027562

第四方物流 (4PL) 市場機會、成長要素、產業趨勢分析及 2026-2035 年預測Fourth-Party Logistics (4PL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球物流(4PL) 市值為 862 億美元,預計到 2035 年將以 6.7% 的複合年成長率成長至 1637 億美元。

市場擴張的驅動力來自貿易量的成長、全球商業的整合以及國際供應鏈日益複雜化。企業越來越需要能夠簡化協調、提高營運效率並增強多方相關人員視覺性的綜合物流解決方案。第四方物流 (4PL) 供應商不僅執行單一物流操作,而且作為策略合作夥伴,代表客戶管理整個供應鏈。透過整合技術平台、多個物流合作夥伴和營運流程,4PL 公司協助企業降低複雜性、最佳化流程,並將責任集中到一個管理組織下。對數位轉型、預測分析和供應鏈韌性的日益關注,以及為拓展地域而進行的合資和收購趨勢,進一步推動了 4PL 解決方案在全球範圍內的應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 862億美元 |

| 預測金額 | 1637億美元 |

| 複合年成長率 | 6.7% |

供應鏈最佳化領域目前佔據29.9%的市場佔有率,預計2025年市場規模將達到258億美元。隨著企業日益關注端到端效率,供應鏈最佳化正成為第四方物流(4PL)服務交付的基礎。該服務整合了承運商、倉儲解決方案和技術平台,旨在簡化營運、提升敏捷性並增強對複雜全球供應鏈的應對力。企業依賴供應鏈最佳化來維持盈利、降低成本,並在瞬息萬變的市場環境中確保營運的穩定性。

預計到2025年,解決方案整合商將佔據47.2%的市場。解決方案整合商作為中央協調者,整合多個第三方物流供應商、技術系統和流程工作流程,以實現一致且高效的營運。他們能夠管理端到端物流、最佳化資源並跨區域提供統一服務,因此對於尋求降低成本、最佳化營運管理和提升供應鏈可視性的公司而言,解決方案整合商至關重要。推動此細分市場成長的因素包括:全球供應鏈日益複雜化、數位轉型措施的推進,以及對即時監控和預測分析日益成長的需求。

美國第四方物流 (4PL) 市場預計到 2025 年將達到 278 億美元,並在 2026 年至 2035 年間以 7.2% 的複合年成長率成長。美國先進的物流基礎設施和多模態能力正在推動整合式 4PL 解決方案的普及。聯邦政府推行的旨在增強供應鏈韌性、透明度和永續性的政策,鼓勵企業採用綜合物流管理模式。貿易政策的優先事項強調安全且多元化的供應鏈,這反過來又促使企業採用 4PL 策略,以降低地緣政治和全球經濟壓力的中斷風險。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子商務的成長和全通路零售的擴張

- 全球供應鏈和跨境貿易日益複雜化。

- 對端到端供應鏈可視性和整合性的需求日益成長

- 注重成本最佳化與營運效率

- 產業潛在風險與挑戰

- 失去對物流營運的直接管理權

- 對單一外部服務供應商的高度依賴

- 市場機遇

- 新興市場擴張伴隨著貿易量增加

- 對綠色和永續物流解決方案的需求日益成長

- 產業專用的第四方物流解決方案的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國聯邦海事委員會

- 加拿大邊境服務局

- 歐洲

- 英國-英國稅務海關總署

- 德國聯邦貨運服務

- 亞太地區

- 中國 - 中華人民共和國交通運輸部

- 印度對外貿易總局

- 拉丁美洲

- 巴西 - 國家陸上運輸局

- 墨西哥 - 基礎設施、通訊和運輸部

- 中東和非洲

- 阿拉伯聯合大公國聯邦交通管理局

- 南非 - 南非運輸部

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 運輸管理系統(TMS)

- 倉庫管理系統(WMS)

- 企業資源規劃(ERP)

- 即時追蹤和遠端資訊處理

- 新興技術

- 人工智慧和機器學習(AI/ML)

- 供應鏈中的區塊鏈

- 數位雙胞胎

- 目前技術

- 專利趨勢(基於初步調查)

- 電子商務對第四方物流市場的影響

- 直接面對消費者(D2C)物流的成長

- 最後一公里配送的挑戰與解決方案

- 與電子商務平台和市場的整合

- 對即時可視化和追蹤的需求

- 對訂單履行速度和庫存管理的影響

- 全球貿易協定和地緣政治趨勢的影響

- 自由貿易協定(FTA)的影響

- 關稅和海關法規的變化

- 政治不穩定和製裁

- 區域貿易集團與跨境物流

- 策略採購與多元化決策

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依解法分類,2022-2035年

- 供應鏈最佳化

- 運輸管理

- 航空

- 船運

- 鐵路和公路

- 庫存管理

- 倉庫管理

- 訂單履行

- 物流管理

第6章 市場估算與預測:依商業模式分類,2022-2035年

- 協同效應 Plus 組織

- 解決方案整合商

- 產業創新者

第7章 市場估計與預測:依公司規模分類,2022-2035年

- 小型企業

- 大公司

第8章 市場估算與預測:依產業分類,2022-2035年

- 零售與電子商務

- 食品/飲料

- 衛生保健

- 車

- 製造業

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 瑞典

- 捷克共和國

- 波蘭

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 新加坡

- 越南

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- DHL

- CH Robinson

- UPS Supply

- XPO Logistics

- DB Schenker

- Kuehne+Nagel

- CEVA Logistics

- Geodis

- Nippon Express

- FedEx

- 大型區域公司

- Rhenus

- Incora

- Allyn International

- Denholm Good Logistics

- Gefco

- Logistics Plus

- Yusen Logistics

- 新興企業

- De Rijke

- X2 UK

- SmartWay Logistics

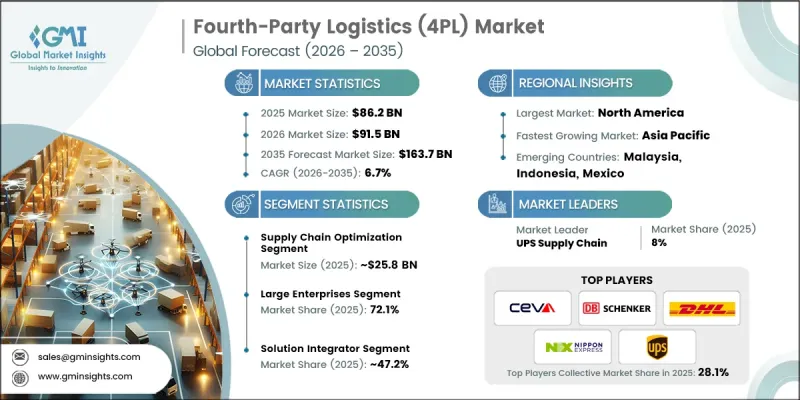

The Global Fourth-Party Logistics Market was valued at USD 86.2 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 163.7 billion by 2035.

The market expansion is fueled by the rising intricacy of international supply chains, driven by growing trade volumes and global commerce integration. Businesses increasingly require comprehensive logistics solutions that simplify coordination, improve operational efficiency, and enhance visibility across multiple stakeholders. Fourth-party logistics providers serve as strategic partners, managing entire supply chains on behalf of clients rather than merely executing isolated logistics tasks. By integrating technology platforms, multiple logistics partners, and operational workflows, 4PL companies enable enterprises to reduce complexity, optimize processes, and consolidate accountability under a single management entity. Rising interest in digital transformation, predictive analytics, and supply chain resilience, along with the trend of forming joint ventures and acquisitions for geographic expansion, further supports the adoption of 4PL solutions worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $86.2 Billion |

| Forecast Value | $163.7 Billion |

| CAGR | 6.7% |

The supply chain optimization segment held a 29.9% share, generating USD 25.8 billion in 2025. Businesses are increasingly focusing on end-to-end efficiency, making supply chain optimization a cornerstone of 4PL service delivery. This service integrates carriers, warehousing solutions, and technology platforms to streamline operations, enhance agility, and improve responsiveness across complex global supply chains. Companies rely on supply chain optimization to maintain profitability, reduce costs, and achieve operational consistency amid volatile market conditions.

The solution integrator segment held a 47.2% share in 2025. Solution integrators act as central orchestrators by combining multiple third-party logistics providers, technology systems, and process workflows into cohesive, efficient operations. Their ability to manage end-to-end logistics, optimize resources, and provide uniform services across regions makes them essential for companies pursuing cost savings, operational control, and improved supply chain visibility. Growth in this segment is driven by increasing global supply chain complexity, digital transformation initiatives, and the rising demand for real-time monitoring and predictive analytics.

U.S. Fourth-Party Logistics Market was valued at USD 27.8 billion in 2025 and is estimated to grow at a CAGR of 7.2% from 2026 to 2035. The country's sophisticated logistics infrastructure and multi-modal transport capabilities favor the adoption of integrated 4PL solutions. Federal policies promoting supply chain resilience, transparency, and sustainability encourage enterprises to implement comprehensive logistics management models. Trade policy priorities emphasize secure, diversified supply chains, prompting businesses to adopt 4PL strategies that mitigate disruption risks from geopolitical and global economic pressures.

Leading companies operating in the Global Fourth-Party Logistics Market include DB Schenker, CEVA Logistics, FedEx Logistics, UPS Supply Chain, DHL, C.H. Robinson, Geodis, Kuehne + Nagel, XPO Logistics, and Nippon Express. Market players strengthen their presence and expand their foothold through strategic initiatives such as forming global partnerships, joint ventures, and acquisitions to enter new regions. Companies invest heavily in technology, including real-time tracking, predictive analytics, AI-based route optimization, and warehouse automation, to enhance operational efficiency and customer value. They focus on offering end-to-end solutions that integrate multiple logistics partners, optimizing resource allocation while maintaining high service standards. Expanding digital platforms, enhancing client-specific solutions, and providing centralized management dashboards improve visibility and accountability. Firms also emphasize sustainability and compliance, adopting environmentally responsible practices to attract socially conscious customers and maintain competitive differentiation in the Global Fourth-Party Logistics Market

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Operational model

- 2.2.4 Organization size

- 2.2.5 Industry

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of e-commerce & omnichannel retail expansion

- 3.2.1.2 Increasing complexity of global supply chains & cross-border trade

- 3.2.1.3 Rising demand for end-to-end supply chain visibility & integration

- 3.2.1.4 Focus on cost optimization & operational efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Loss of direct control over logistics operations

- 3.2.2.2 High dependency on single external service provider

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing trade volumes

- 3.2.3.2 Increasing demand for green & sustainable logistics solutions

- 3.2.3.3 Growth in industry-specific 4PL solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Federal Maritime Commission

- 3.4.1.2 Canada - Canada Border Services Agency

- 3.4.2 Europe

- 3.4.2.1 UK - HM Revenue and Customs

- 3.4.2.2 Germany - Federal Office for Goods Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Ministry of Transport of the People's Republic of China

- 3.4.3.2 India - Directorate General of Foreign Trade

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Agencia Nacional de Transportes Terrestres

- 3.4.4.2 Mexico - Secretaria de Infraestructura, Comunicaciones y Transportes

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Federal Transport Authority

- 3.4.5.2 South Africa - South African Department of Transport

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Transportation Management Systems (TMS)

- 3.8.1.2 Warehouse Management Systems (WMS)

- 3.8.1.3 Enterprise Resource Planning (ERP)

- 3.8.1.4 Real-Time Tracking & Telematics

- 3.8.2 Emerging technologies

- 3.8.2.1 Artificial Intelligence & Machine Learning (AI/ML)

- 3.8.2.2 Blockchain for Supply Chain

- 3.8.2.3 Digital Twins

- 3.8.1 Current technologies

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Impact of e-commerce on the 4PL market

- 3.10.1 Growth of Direct-to-Consumer (D2C) logistics

- 3.10.2 Last-mile delivery challenges & solutions

- 3.10.3 Integration with e-commerce platforms & marketplaces

- 3.10.4 Demand for real-time visibility & tracking

- 3.10.5 Effect on order fulfillment speed & inventory management

- 3.11 Impact of global trade agreements & geopolitical developments

- 3.11.1 Influence of Free Trade Agreements (FTAs)

- 3.11.2 Tariff changes & customs regulations

- 3.11.3 Political instability & sanctions

- 3.11.4 Regional trade blocs & cross-border logistics

- 3.11.5 Strategic sourcing & diversification decisions

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Supply chain optimization

- 5.3 Transportation management

- 5.3.1 Air

- 5.3.2 Sea

- 5.3.3 Rail & Road

- 5.4 Inventory management

- 5.5 Warehouse management

- 5.6 Order fulfillment

- 5.7 Distribution management

Chapter 6 Market Estimates & Forecast, By Operational model, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Synergy plus organization

- 6.3 Solution integrator

- 6.4 Industry innovator

Chapter 7 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 SMEs

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Industry, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Retail & E-commerce

- 8.3 Food & Beverage

- 8.4 Healthcare

- 8.5 Automotive

- 8.6 Manufacturing

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Sweden

- 9.3.7 Czech Republic

- 9.3.8 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 DHL

- 10.1.2 C.H. Robinson

- 10.1.3 UPS Supply

- 10.1.4 XPO Logistics

- 10.1.5 DB Schenker

- 10.1.6 Kuehne + Nagel

- 10.1.7 CEVA Logistics

- 10.1.8 Geodis

- 10.1.9 Nippon Express

- 10.1.10 FedEx

- 10.2 Regional players

- 10.2.1 Rhenus

- 10.2.2 Incora

- 10.2.3 Allyn International

- 10.2.4 Denholm Good Logistics

- 10.2.5 Gefco

- 10.2.6 Logistics Plus

- 10.2.7 Yusen Logistics

- 10.3 Emerging players

- 10.3.1 De Rijke

- 10.3.2 X2 UK

- 10.3.3 SmartWay Logistics

2026年全球多模態物流市場報告2026年全球第四方物流(4PL)市場報告

2026年全球多模態物流市場報告2026年全球第四方物流(4PL)市場報告 物流市場:依服務類型、合約類型、營運能力、產業和組織規模分類-2026-2032年全球預測

物流市場:依服務類型、合約類型、營運能力、產業和組織規模分類-2026-2032年全球預測 4PL(Fourth Party Logistics)的美國市場:依類型、最終用戶、模式、地區、機會及預測,2018-2032

4PL(Fourth Party Logistics)的美國市場:依類型、最終用戶、模式、地區、機會及預測,2018-2032 第四方物流市場-全球產業規模、佔有率、趨勢、機會和預測(按模式、類型、應用、地區和競爭細分,2020-2030 年)

第四方物流市場-全球產業規模、佔有率、趨勢、機會和預測(按模式、類型、應用、地區和競爭細分,2020-2030 年) 4P物流市場分析與2034年預測:類型、產品、服務、技術、應用、組件、部署、最終用戶、功能、解決方案

4P物流市場分析與2034年預測:類型、產品、服務、技術、應用、組件、部署、最終用戶、功能、解決方案 拉丁美洲 4PL(第四方物流)-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)4PL (第四方物流) 市場評估:類型·終端用戶·方式·各地各國的機會及預測 (2017-2031年)印度的4PL(第四方物流)市場:各類型,各終端用戶,模式別,各地區,機會,預測,2018年~2032年

拉丁美洲 4PL(第四方物流)-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)4PL (第四方物流) 市場評估:類型·終端用戶·方式·各地各國的機會及預測 (2017-2031年)印度的4PL(第四方物流)市場:各類型,各終端用戶,模式別,各地區,機會,預測,2018年~2032年 物流(4PL) 全球市場

物流(4PL) 全球市場