|

市場調查報告書

商品編碼

2027556

凱爾特海鹽市場機會、成長要素、產業趨勢分析及2026-2035年預測Celtic Salt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

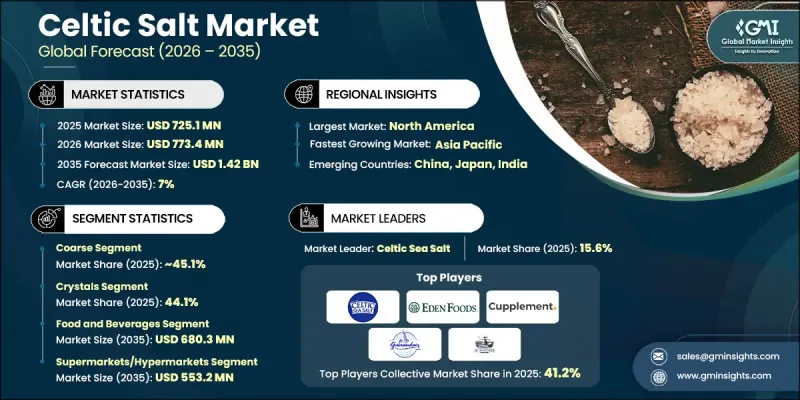

據估計,到 2025 年,全球凱爾特海鹽市場價值將達到 7.251 億美元,年複合成長率為 7%,到 2035 年將達到 14.2 億美元。

市場擴張源自於消費者對天然、加工最少的食品而非精製食品日益成長的偏好。凱爾特海鹽因其富含鈣、鎂、鉀等礦物質而備受推崇,深受注重健康、追求「潔淨標示」產品的消費者青睞。人們對有機食品和全食物日益成長的興趣進一步提升了凱爾特海鹽的受歡迎程度。除了烹飪用途外,富含礦物質的鹽在美容和個人護理領域的需求也在成長。在這個領域,消費者擴大將天然成分融入家庭水療、護膚和整體健康養生實踐中。這種對健康、養生和天然成分日益成長的關注,為市場持續成長創造了機會。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 7.251億美元 |

| 預測金額 | 14.2億美元 |

| 複合年成長率 | 7% |

預計到2025年,粗粒凱爾特海鹽的市佔率將達到45.1%,並在2035年之前以5.2%的複合年成長率成長。其傳統的採集方式和廣泛的烹飪用途使其成為許多家庭的首選。粗粒保留了天然水分和礦物質,在烹飪過程中能夠提升食物的風味和口感。

預計營養補充品市場在預測期內將以7.3%的複合年成長率成長。古老的凱爾特海鹽作為一種天然礦物質補充劑進行銷售,有助於維持電解質平衡、補充水分和促進整體細胞健康,這進一步提升了其在健康養生領域的重要性。

預計2026年至2035年間,北美凱爾特海鹽市場將以6.4%的複合年成長率成長。由於人們對天然、富含礦物質的食品成分的認知不斷提高,北美已成為凱爾特海鹽的主要市場。美國和加拿大的健康意識日益增強的消費者正擴大用未經精煉、富含礦物質的替代品取代傳統的食鹽。有機產品和潔淨標示產品的日益普及以及美食的興起,都推動了這一成長。此外,健康和天然化妝品行業的擴張也促進了需求,凱爾特海鹽擴大被添加到具有療效的沐浴產品、磨砂膏和其他自我護理產品中。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 消費者越來越偏好天然、富含礦物質的食鹽。

- 消費者越來越注重健康和潔淨標示的食品。

- 在化妝品和個人保健產品中的應用不斷擴展

- 產業潛在風險與挑戰

- 與傳統鹽相比,生產和收穫成本更高

- 新興市場消費者意識較低

- 與喜馬拉雅粉紅鹽和其他特殊鹽的競爭。

- 市場機遇

- 線上零售和高階美食平台的成長

- 對天然營養補充品的需求日益成長

- 對優質和手工食品原料的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 粗粒/灰色(Selgri)

- 傳統未洗的

- 乾燥的粗粒

- 細顆粒/粉末

- 調味/浸泡

第6章 市場估計與預測:依類型分類,2022-2035年

- 水晶

- 粉末

- 薄片

- 液體/鹽水

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 食品/飲料

- 烹飪/家常菜

- 餐飲服務業/商用

- 食品製造

- 化妝品和個人護理

- 營養補充品

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 超級市場/大賣場

- 線上零售

- 專賣店

- 直銷

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Eden Foods

- Cupplement BV

- 82 Minerals

- Le Marinier

- Le Guerandais

- Celtic Sea Salt

- Elite Brand Supply

- Celt Salt

- Celtic Salt

- VIVA LA GAIA

- Dr. Celtic

The Global Celtic salt market was valued at USD 725.1 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 1.42 billion by 2035.

The market expansion is driven by increasing consumer preference for natural and minimally processed ingredients over refined alternatives. Celtic sea salt is favored for its rich mineral content, including calcium, magnesium, and potassium, which appeals to health-conscious buyers seeking products with clean labels. The rising interest in organic and whole-food diets has further propelled the adoption of Celtic salt. Beyond culinary use, mineral-rich salts are also in demand in the beauty and personal care sectors, where consumers increasingly incorporate natural ingredients into home spa treatments, skincare routines, and holistic wellness practices. This growing focus on health, wellness, and natural ingredients is creating continuous opportunities for market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $725.1 Million |

| Forecast Value | $1.42 Billion |

| CAGR | 7% |

The coarse Celtic salt accounted for 45.1% share in 2025 and is expected to grow at a CAGR of 5.2% through 2035. Its traditional harvesting process and widespread use in cooking make it the preferred form for many households. Coarse grains retain natural moisture and minerals, enhancing both flavor and texture during food preparation.

The dietary supplement segment is projected to grow at a CAGR of 7.3% over the forecast period. Ancient Celtic salts are marketed as natural mineral supplements to support electrolyte balance, hydration, and overall cellular health, further increasing their relevance in wellness-oriented applications.

North American Celtic Salt Market is anticipated to grow at a CAGR of 6.4% during 2026 to 2035. Increasing awareness of natural, mineral-rich food ingredients has made North America a key market for Celtic salt. Health-conscious consumers in the US and Canada are increasingly substituting traditional table salt with unrefined, mineral-rich alternatives. Growth is supported by the rising popularity of organic and clean-label products, as well as a surge in gourmet cooking. In addition, the expansion of the wellness and natural cosmetics sectors is contributing to demand, as Celtic salts are increasingly included in therapeutic bath products, scrubs, and other self-care formulations.

Prominent players in the Global Celtic Salt Market include Eden Foods, Celtic Sea Salt, Le Guerandais, Le Marinier, 82 Minerals, VIVA LA GAIA, Celt Salt, Cupplement B.V., Elite Brand Supply, Dr. Celtic, and Celtic Salt. Companies in the Celtic salt market are leveraging strategies such as expanding production capacities to meet growing consumer demand and investing in sustainable harvesting practices to appeal to eco-conscious buyers. Strategic partnerships and distribution agreements enable firms to increase market reach and penetrate emerging regions. Innovation in packaging and product formats, such as ready-to-use culinary blends and wellness-focused formulations, strengthens brand differentiation. Companies also focus on marketing campaigns highlighting natural purity, mineral content, and clean-label benefits to educate consumers. Additionally, investments in research and development allow for quality enhancement, certification, and premium positioning, helping firms secure a competitive foothold in the global Celtic salt market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer preference for natural and mineral-rich salts

- 3.2.1.2 Growth of health-conscious and clean-label food trends

- 3.2.1.3 Expanding applications in cosmetics and personal care products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and harvesting costs compared to conventional salt

- 3.2.2.2 Limited consumer awareness in emerging markets

- 3.2.2.3 Competition from Himalayan pink salt and other specialty salts

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of online retail and specialty gourmet food platforms

- 3.2.3.2 Increasing demand for natural dietary supplements

- 3.2.3.3 Rising demand for premium and artisanal food ingredients

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Coarse/Grey (Sel Gris)

- 5.2.1 Traditional Unwashed

- 5.2.2 Dried Coarse

- 5.3 Fine/Ground

- 5.4 Flavored/Infused

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Crystals

- 6.3 Powder

- 6.4 Flakes

- 6.5 Liquid/Brine

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and Beverages

- 7.2.1 Culinary/Home Cooking

- 7.2.2 Food Service/Professional

- 7.2.3 Food Manufacturing

- 7.3 Cosmetics and Personal Care

- 7.4 Dietary Supplements

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets/Hypermarkets

- 8.3 Online Retail

- 8.4 Specialty Stores

- 8.5 Direct Sales

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Eden Foods

- 10.2 Cupplement B.V.

- 10.3 82 Minerals

- 10.4 Le Marinier

- 10.5 Le Guerandais

- 10.6 Celtic Sea Salt

- 10.7 Elite Brand Supply

- 10.8 Celt Salt

- 10.9 Celtic Salt

- 10.10 VIVA LA GAIA

- 10.11 Dr. Celtic

竹鹽市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、分銷管道、地區和競爭格局分類,2021-2031年

竹鹽市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、分銷管道、地區和競爭格局分類,2021-2031年 海鹽市場規模、佔有率和成長分析:按類型、粒度、應用、包裝類型、通路、最終用戶和地區分類-2026-2033年產業預測

海鹽市場規模、佔有率和成長分析:按類型、粒度、應用、包裝類型、通路、最終用戶和地區分類-2026-2033年產業預測 乳化鹽市場規模、佔有率和成長分析:按類型、性質、應用和地區分類-2026-2033年產業預測

乳化鹽市場規模、佔有率和成長分析:按類型、性質、應用和地區分類-2026-2033年產業預測 全球鹽市場:市場規模、份額、成長率、產業分析、類型、應用及區域分析,未來預測(2026-2034)

全球鹽市場:市場規模、份額、成長率、產業分析、類型、應用及區域分析,未來預測(2026-2034) 食鹽市場規模、佔有率及成長分析(按類型、來源、應用和地區分類)-2026-2033年產業預測食鹽(TS)市場:2025-2030年預測

食鹽市場規模、佔有率及成長分析(按類型、來源、應用和地區分類)-2026-2033年產業預測食鹽(TS)市場:2025-2030年預測 凱爾特鹽的世界市場Chipotle鹽的全球市場全球強化鹽市場全球精品鹽市場

凱爾特鹽的世界市場Chipotle鹽的全球市場全球強化鹽市場全球精品鹽市場