|

市場調查報告書

商品編碼

2027548

罐裝葡萄酒市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Canned Wine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

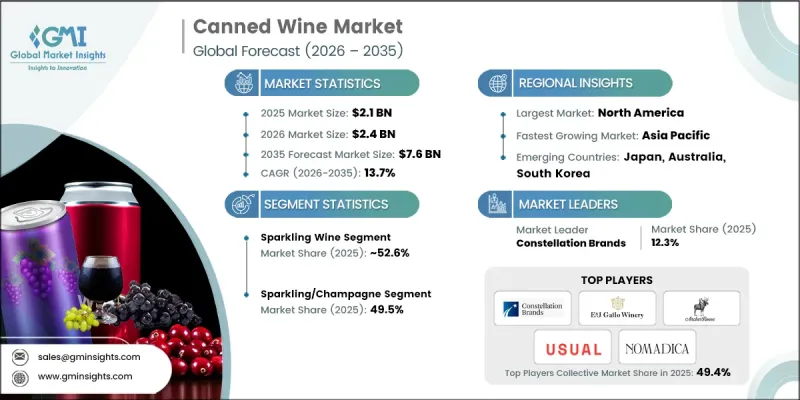

據估計,2025 年全球罐裝葡萄酒市場價值為 21 億美元,並將以 13.7% 的複合年成長率成長,到 2035 年達到 76 億美元。

罐裝葡萄酒作為便捷的便攜包裝解決方案,正日益受到歡迎,尤其是在戶外和社交活動中。參加野餐、節日慶典、露營旅行和體育賽事的消費者越來越青睞罐裝葡萄酒,因為它們輕鬆易攜,且處理方便。與易碎的玻璃瓶不同,罐裝葡萄酒在保證便利性的同時,也兼具耐用性,其單份包裝設計讓消費者無需購買整瓶即可品嚐葡萄酒。永續性也是一個關鍵因素。根據美國環保署 (EPA) 的數據顯示,鋁罐的回收率約為 50%,使其成為更環保的選擇。隨著消費者接受度的提高,市場正在迅速擴張,起泡酒、桃紅葡萄酒、紅葡萄酒、白葡萄酒和葡萄酒雞尾酒等產品的豐富選擇,使企業能夠滿足不同消費者的喜好和活動需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 21億美元 |

| 預測金額 | 76億美元 |

| 複合年成長率 | 13.7% |

預計到2025年,氣泡酒市佔率將達到52.6%,並在2035年之前以14.1%的複合年成長率成長。雖然紅酒和白酒因其便攜性而日益受到歡迎,但普羅塞克和香檳等氣泡酒仍然是慶祝場合的首選。創新的包裝設計使這些產品在正式和休閒場合都能輕鬆享用,從而提升了其市場支持。

到2025年,氣泡酒/香檳將佔據49.5%的市場。雖然紅酒和白酒仍將是罐裝葡萄酒銷售的主要驅動力,但桃紅葡萄酒作為一種時尚清爽的選擇,正受到年輕消費者的青睞。氣泡酒用途廣泛,從慶祝活動到休閒聚會都能享用,這進一步鞏固了其市場主導地位。

預計到2025年,北美罐裝葡萄酒市場規模將達到11億美元,並在2026年至2035年間以12.2%的複合年成長率成長。都市區消費者越來越傾向於在戶外活動時飲用罐裝葡萄酒,而具有環保意識的消費者則在尋找永續且便利的選擇。對優質口味和創新品嚐體驗的需求正在推動市場擴張,而老酒商也不斷鞏固其市場地位。美國和加拿大的市場成長均得益於消費者對便攜環保包裝解決方案的偏好。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 對便捷易攜的葡萄酒包裝的需求日益成長。

- 拓展戶外休閒與活動文化

- 注重永續發展的人們喜歡鋁而不是玻璃。

- 產業潛在風險與挑戰

- 人們對罐裝高級葡萄酒的認知障礙

- 與瓶裝葡萄酒相比,它的保存期限較短。

- 市場機遇

- 進入葡萄酒文化正在蓬勃發展的新興市場

- 優質化罐裝葡萄酒產品系列組合的檔次

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 無氣泡葡萄酒

- 紅葡萄酒

- 白葡萄酒

- 玫瑰紅葡萄酒

- 氣泡酒

- 香檳酒

- 普羅塞克

- 其他

- 加烈葡萄酒

- 雪莉酒

- 港口

- 苦艾酒

- 其他

第6章 市場估價與預測:按顏色分類的葡萄酒,2022-2035年

- 紅葡萄酒

- 白葡萄酒

- 玫瑰紅葡萄酒

- 氣泡酒/香檳

第7章 市場估計與預測:依酒精濃度分類,2022-2035年

- 低酒精酒精濃度%)

- 中等酒精濃度(10-14%)

- 高酒精酒精濃度%)

第8章 市場估價與預測:依包裝類型分類,2022-2035年

- 單份罐裝

- 每罐多份

第9章 市場估算與預測:依產品類型分類,2022-2035年

- 傳統的

- 有機的

第10章 市場估價與預測:依通路分類,2022-2035年

- On-Trade

- Off-Trade

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- Concha y Toro

- Bodega Santa Julia

- Usual Wines

- House Wine

- Nomadica

- Maker Wine

- SANS Wine Co

- Off Track Wines

- Marisco

- Villa Maria

- Giesen

- Rosadito

- Archer Roose

- Constellation Brands

- E. & J. Gallo

The Global Canned Wine Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 13.7% to reach USD 7.6 billion by 2035.

Canned wine has gained traction as a convenient and portable packaging solution, especially for outdoor and social events. Consumers attending picnics, festivals, camping trips, and sports events increasingly prefer cans for their lightweight design, ease of transport, and simple disposal. Unlike fragile glass bottles, cans provide durability without sacrificing convenience, while single-serving portions allow consumers to sample wines without committing to a full bottle. Sustainability also plays a role, as aluminum cans achieve approximately a 50% recycling rate according to the U.S. Environmental Protection Agency, making them a more environmentally friendly option. The market has expanded rapidly with consumer acceptance, offering products that include sparkling wines, rose, red, white wines, and wine cocktails, enabling companies to cater to diverse tastes and event requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 13.7% |

The sparkling wine segment held 52.6% share in 2025 and is expected to grow at a CAGR of 14.1% through 2035. While red and white still wines are growing in popularity due to portability, sparkling varieties such as prosecco and champagne dominate celebrations. These products are increasingly favored because innovative packaging allows them to be more accessible for both formal and casual occasions.

In 2025, the sparkling/champagne segment accounted for 49.5% share. Red and white wines continue to be major contributors to canned wine sales, while rose is gaining traction among younger consumers who see it as a stylish and refreshing option. The versatility of sparkling wines for celebratory and informal settings strengthens their dominance in the market.

North America Canned Wine Market was valued at USD 1.1 billion in 2025 and is expected to grow at a CAGR of 12.2% from 2026 to 2035. Urban consumers increasingly prefer canned wine for outdoor activities, while eco-conscious buyers seek sustainable and convenient options. Demand for premium flavors and innovative taste experiences supports market expansion, with existing brands consolidating their positions. Both the U.S. and Canada are experiencing growth driven by the preference for portable, environmentally responsible packaging solutions.

Key players in the Global Canned Wine Market include Usual Wines, SANS Wine Co, House Wine, Nomadica, Villa Maria, Concha y Toro, Giesen, Maker Wine, Off Track Wines, Bodega Santa Julia, Rosadito, Archer Roose, Marisco, E. & J. Gallo, and Constellation Brands. Global Canned Wine Market are focusing on strategies such as expanding product portfolios to include sparkling, rose, and wine cocktail options to appeal to a broader consumer base. Firms are investing in innovative packaging designs that improve portability, sustainability, and consumer convenience. Strategic partnerships with distributors, retailers, and event organizers enable wider market reach. Marketing efforts emphasize eco-friendly credentials and premium flavor experiences, creating brand differentiation. Companies are also adopting direct-to-consumer models, digital promotion, and limited-edition releases to enhance engagement, boost sales, and strengthen market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Wine color

- 2.2.4 Alcohol content

- 2.2.5 Packaging

- 2.2.6 Production type

- 2.2.7 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenient & portable wine packaging

- 3.2.1.2 Growing outdoor recreation & event culture

- 3.2.1.3 Sustainability preferences favoring aluminum over glass

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Premium wine perception barriers for canned format

- 3.2.2.2 Limited shelf life compared to bottled wine

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing wine culture

- 3.2.3.2 Premiumization of canned wine portfolio

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Million Litres)

- 5.1 Key trends

- 5.2 Still wine

- 5.2.1 Red wine

- 5.2.2 White wine

- 5.2.3 Rose wine

- 5.3 Sparkling wine

- 5.3.1 Champagne

- 5.3.2 Prosecco

- 5.3.3 Others

- 5.4 Fortified wine

- 5.4.1 Sherry

- 5.4.2 Port

- 5.4.3 Vermouth

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Wine Color, 2022-2035 (USD Billion) (Million Litres)

- 6.1 Key trends

- 6.2 Red wine

- 6.3 White wine

- 6.4 Rose wine

- 6.5 Sparkling/champagne

Chapter 7 Market Estimates and Forecast, By Alcohol Content, 2022-2035 (USD Billion) (Million Litres)

- 7.1 Key trends

- 7.2 Low alcohol (< 10% ABV)

- 7.3 Medium alcohol (10-14% ABV)

- 7.4 High alcohol (>14% ABV)

Chapter 8 Market Estimates and Forecast, By Packaging, 2022-2035 (USD Billion) (Million Litres)

- 8.1 Key trends

- 8.2 Single-serve cans

- 8.3 Multi-serve cans

Chapter 9 Market Estimates and Forecast, By Production Type 2022-2035 (USD Billion) (Million Litres)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Organic

Chapter 10 Market Estimates and Forecast, By Distribution Channel 2022-2035 (USD Billion) (Million Litres)

- 10.1 Key trends

- 10.2 On-Trade

- 10.3 Off-Trade

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Litres)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Concha y Toro

- 12.2 Bodega Santa Julia

- 12.3 Usual Wines

- 12.4 House Wine

- 12.5 Nomadica

- 12.6 Maker Wine

- 12.7 SANS Wine Co

- 12.8 Off Track Wines

- 12.9 Marisco

- 12.10 Villa Maria

- 12.11 Giesen

- 12.12 Rosadito

- 12.13 Archer Roose

- 12.14 Constellation Brands

- 12.15 E. & J. Gallo