|

市場調查報告書

商品編碼

2027530

檯燈市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Desk Lamp Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

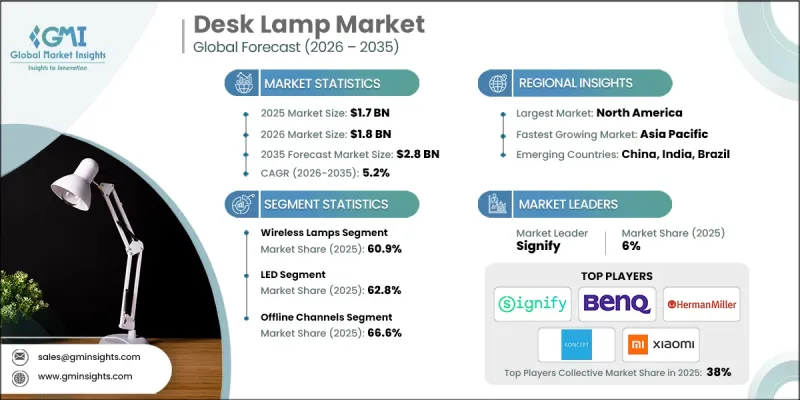

全球檯燈市場預計到 2025 年價值 17 億美元,預計到 2035 年將以 5.2% 的複合年成長率成長至 28 億美元。

市場擴張的驅動力來自先進檯燈技術的普及、無線照明解決方案的日益普及以及人們對符合人體工學的工作空間設計的日益關注。消費者對節能LED照明的需求不斷成長,促使製造商將創新功能融入產品,以適應現代工作環境。在北美和亞太地區,高階機型和智慧檯燈越來越受歡迎,這得益於遠距辦公的趨勢以及對可自訂、護眼照明的需求。此外,電子商務和D2C(直接面對消費者)管道的興起,使老牌企業和新參與企業都能有效率地滿足全球需求。為了滿足不斷變化的環境法規和消費者期望,製造商也在採用永續的生產方式,例如使用可回收材料和節能製程。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 17億美元 |

| 預測金額 | 28億美元 |

| 複合年成長率 | 5.2% |

無線檯燈市佔率高達60.9%,預計2025年市場規模將達10.3億美元。推動這一市場成長的主要因素是消費者對便攜性、安裝柔軟性和現代設計的偏好。可充電電池供電的檯燈無需電源插座,使用者可依需求自由放置。鋰離子電池技術的進步使得檯燈能夠連續使用8至12小時,進一步提升了其便利性和普及性。

到2025年,線下銷售通路將佔市場佔有率的66.6%,市場規模將達到11.2億美元。傳統零售通路仍保持主導地位,因為消費者更傾向於親身感受燈具的設計、做工和光照效果。家具店、辦公用品零售商、家居建材商店和燈具專賣店能夠為消費者提供即時的產品體驗、親身試用和即時購買管道。

美國檯燈市場佔76.1%的市場佔有率,預計2025年市場規模將達5億美元。美國市場的成長主要得益於遠距辦公的普及、人們對符合人體工學的工作空間意識的提高以及消費者購買力的增強。北美消費者越來越傾向選擇功能先進、品質卓越的高階智慧檯燈。包括辦公用品連鎖店、家居建材商店和線上平台在內的完善零售體系,為住宅和小規模企業提供了豐富的產品選擇和詳細的規格說明。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 成長促進因素

- 對LED和節能照明解決方案的需求日益成長

- 遠距辦公和在家工作的趨勢

- 無線和智慧照明技術的創新

- 產業潛在風險與挑戰

- 低成本製造商之間的激烈競爭

- 不同市場的能源效率標準各不相同。

- 機會

- 電子商務與D2C通路的擴張

- 智慧家庭生態系統與永續發展舉措的融合

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 區域價格波動(基於初步調查)

- 監理情勢

- 波特的分析

- PESTEL 分析

- 交易數據分析

- 進出口數量和價值的變化趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 主要進口國和出口國(根據初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區與類型(現代貿易與傳統貿易)分類的通路滲透率(基於初步調查)

- 最後一公里基礎設施的不足和新分銷管道的變化(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章:檯燈市場估價與預測:按類型分類,2022-2035年

- 有線燈

- 無線燈

第6章 檯燈市場估價與預測:依技術分類,2022-2035年

- LED

- 螢光

- 鹵素

第7章 檯燈市場估價與預測:依產品類型分類,2022-2035年

- 檯燈

- 裝飾燈

第8章 檯燈市場估價與預測:依最終用途分類,2022-2035年

- 住宅

- 商業的

- 辦公室和共享辦公空間

- 教育機構

- 設計工作室

- 飯店及餐飲業

- 其他(銀行、醫院等)

第9章:檯燈市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 企業網站

- 離線

- 專賣店

- 百貨公司

- 家具店

- 其他(家居建材商店、電子產品量販店等)

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- ANGLEPOISE

- ArnsbergerLicht Inc

- Artemide SpA

- BenQ

- Flos SpA

- Herman Miller, Inc.

- Inter IKEA BV

- Koncept Inc.

- Newhouse Lighting

- Opple Lighting

- OttLite

- Pablo Designs

- Panasonic Holdings Corporation

- Signify

- Xiaomi

The Global Desk Lamp Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 2.8 billion by 2035.

Market expansion is driven by the rising adoption of advanced desk lamp technologies, the growing popularity of wireless lighting solutions, and increased focus on ergonomic workspace design. Consumers are increasingly seeking energy-efficient LED lighting options, prompting manufacturers to incorporate innovative features tailored to modern work environments. Premium and smart desk lamp models are gaining traction in regions like North America and Asia Pacific, fueled by remote work trends and demand for customizable, eye-friendly lighting. Additionally, the rise of e-commerce and direct-to-consumer sales channels has enabled both established brands and new entrants to tap into global demand efficiently. Manufacturers are also adopting sustainable production methods, including recyclable materials and energy-saving processes, aligning with evolving environmental regulations and consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.2% |

The wireless desk lamps segment held a 60.9% share, generating USD 1.03 billion in 2025. This segment is driven by consumer preference for portability, flexible placement, and modern design. Rechargeable battery-powered lamps eliminate reliance on power outlets, allowing users to position light wherever it is needed. Advances in lithium-ion battery technology enable 8-12 hours of continuous use, enhancing convenience and adoption.

The offline sales segment captured 66.6% share with USD 1.12 billion in 2025. Traditional retail continues to lead due to consumer preference for in-person evaluation of lamp design, build quality, and light output. Furniture stores, office supply retailers, home improvement centers, and specialty lighting shops provide instant product access, hands-on experience, and immediate purchase fulfillment.

U.S. Desk Lamp Market accounted for 76.1% share, generating USD 0.50 billion in 2025. Market growth in the U.S. is driven by strong remote work adoption, awareness of ergonomic workspaces, and high consumer purchasing power. North American consumers increasingly demand premium and smart desk lamps with advanced features and superior build quality. The extensive retail infrastructure, including office supply chains, home improvement stores, and online platforms, provides a wide product selection and detailed specifications, supporting both residential and small business purchases.

Key companies operating in the Global Desk Lamp Market include BenQ, Signify, ANGLEPOISE, Newhouse Lighting, Pablo Designs, Artemide S.p.A., Xiaomi, Inter IKEA B.V., Koncept Inc., Flos S.p.A., Herman Miller, Inc., ArnsbergerLicht Inc, OttLite, Panasonic Holdings Corporation, and Opple Lighting. Market players are strengthening their positions through innovation, product diversification, and global expansion. Companies focus on integrating smart features, energy-efficient LED technologies, and ergonomic designs to differentiate their offerings. Expanding distribution networks across offline retail, e-commerce, and direct-to-consumer channels enhances reach and accessibility. Strategic collaborations, licensing agreements, and localized manufacturing enable faster market penetration and cost efficiencies. Brands emphasize after-sales support, product warranties, and customer education to foster loyalty. Competitive pricing, seasonal promotions, and continuous product upgrades also help maintain market share and appeal to both residential and professional users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Product

- 2.2.5 End User

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for LED and energy-efficient lighting solutions

- 3.2.1.2 Rising remote work and home office trends

- 3.2.1.3 Innovation in wireless and smart lighting technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition from low-cost manufacturers

- 3.2.2.2 Varying energy efficiency standards across markets

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of e-commerce and direct-to-consumer channels

- 3.2.3.2 Integration of smart home ecosystems and sustainability initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.6.3 Regional Price Variations (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis

- 3.10.1 Import & Export Volume & Value Trends(Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact(Driven by Primary Research)

- 3.10.3 Top Importing & Exporting Countries (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Desk Lamp Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Unit)

- 5.1 Key trends

- 5.2 Wired Lamps

- 5.3 Wireless Lamps

Chapter 6 Desk Lamp Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Unit)

- 6.1 Key trends

- 6.2 LED

- 6.3 Fluorescent

- 6.4 Halogen

Chapter 7 Desk Lamp Market Estimates & Forecast, By Product, 2022 - 2035, (USD Billion) (Million Unit)

- 7.1 Key trends

- 7.2 Reading Lamps

- 7.3 Decorative Lamps

Chapter 8 Desk Lamp Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Unit)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office & Coworking Spaces

- 8.3.2 Educational Institutions

- 8.3.3 Design Studios

- 8.3.4 Hotels and Hospitality

- 8.3.5 Others (Banks, hospitals, etc.)

Chapter 9 Desk Lamp Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Unit)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-Commerce Sites

- 9.2.2 Company Website

- 9.3 Offline

- 9.3.1 Specialty Stores

- 9.3.2 Department Stores

- 9.3.3 Furniture Stores

- 9.3.4 Others (Home Improvement Stores, Electronics Retailers, etc.)

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Unit)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ANGLEPOISE

- 11.2 ArnsbergerLicht Inc

- 11.3 Artemide S.p.A.

- 11.4 BenQ

- 11.5 Flos S.p.A.

- 11.6 Herman Miller, Inc.

- 11.7 Inter IKEA B.V.

- 11.8 Koncept Inc.

- 11.9 Newhouse Lighting

- 11.10 Opple Lighting

- 11.11 OttLite

- 11.12 Pablo Designs

- 11.13 Panasonic Holdings Corporation

- 11.14 Signify

- 11.15 Xiaomi

2034年室內植物和園藝市場預測-按產品類型、植物尺寸、園藝類型、價格範圍、分銷管道、最終用戶和地區分類的全球分析

2034年室內植物和園藝市場預測-按產品類型、植物尺寸、園藝類型、價格範圍、分銷管道、最終用戶和地區分類的全球分析 室內植物市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、分銷管道、地區和競爭格局分類,2021-2031年室內植物產品和服務市場預測至2034年-按產品、服務類型、分銷管道、應用、最終用戶和地區分類的全球分析家居裝飾產品市場預測至2034年-按產品、材料、價格範圍、分銷管道、最終用戶和地區分類的全球分析室內植物解決方案市場預測至2034年-按產品、服務類型、通路、應用、最終用戶和地區分類的全球分析

室內植物市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、分銷管道、地區和競爭格局分類,2021-2031年室內植物產品和服務市場預測至2034年-按產品、服務類型、分銷管道、應用、最終用戶和地區分類的全球分析家居裝飾產品市場預測至2034年-按產品、材料、價格範圍、分銷管道、最終用戶和地區分類的全球分析室內植物解決方案市場預測至2034年-按產品、服務類型、通路、應用、最終用戶和地區分類的全球分析 風鈴市場:2026-2032年全球市場預測(依產品類型、材料、通路、應用及最終用戶分類)

風鈴市場:2026-2032年全球市場預測(依產品類型、材料、通路、應用及最終用戶分類) 風鈴市場規模、佔有率和成長分析:依材質、設計、尺寸、價格範圍、銷售管道和地區分類-2026-2033年產業預測鐵路室內裝潢產品市場(按產品類型、材料類型、安裝類型、最終用戶和銷售管道),全球預測(2026-2032年)

風鈴市場規模、佔有率和成長分析:依材質、設計、尺寸、價格範圍、銷售管道和地區分類-2026-2033年產業預測鐵路室內裝潢產品市場(按產品類型、材料類型、安裝類型、最終用戶和銷售管道),全球預測(2026-2032年) 全球鐵路運輸市場室內裝潢產品市場趨勢及展望(預測至2031年)城市叢林室內植物市場預測至2032年:按植物類型、分銷管道、應用、最終用戶和地區分類的全球分析

全球鐵路運輸市場室內裝潢產品市場趨勢及展望(預測至2031年)城市叢林室內植物市場預測至2032年:按植物類型、分銷管道、應用、最終用戶和地區分類的全球分析