|

市場調查報告書

商品編碼

2027526

電動曳引機市場機會、成長要素、產業趨勢分析及2026-2035年預測Electric Tractor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

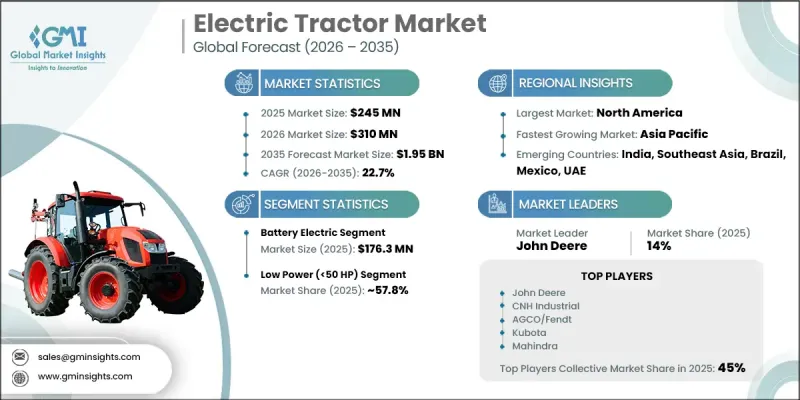

2025 年全球電動曳引機市場規模預計為 2.45 億美元,預計到 2035 年將達到 19.5 億美元,年複合成長率為 22.7%。

隨著農業領域向電氣化轉型不斷推進,市場呈現出強勁的成長勢頭,這主要得益於減少排放氣體、降低營運成本和提升長期永續性的需求。日益成長的監管壓力旨在遏制非道路農業機械的溫室排放排放,這顯著加速了主要農業地區對電動曳引機的採用。各國政府也透過補貼、稅收減免和低利率貸款等財政獎勵措施支持這項轉型,使農民更容易負擔得起電動曳引機。同時,電池系統和電力驅動系統的快速發展正在改變人們對電動曳引機性能的預期。更高的能量密度、更快的充電速度和更長的電池壽命,使得電動曳引機能夠實現更長的運作週期,並拓展其在農業領域的應用範圍。更低的電池成本進一步降低了初始投資成本,並降低了整體擁有成本。電力電子技術的進步也提高了扭力傳輸性能,使電動曳引機能夠勝任高難度的農業作業。與傳統的柴油曳引機相比,電動曳引機的機械部件更少,因此維護需求更低,運作效率更高。隨著技術的不斷成熟,電動曳引機正日益被視為實用、注重生產力的農業機械,而不是實驗性的替代方案。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2.45億美元 |

| 預計金額 | 19.5億美元 |

| 複合年成長率 | 22.7% |

預計到2025年,電池動力曳引機市場規模將達到1.763億美元。按動力系統分類,該市場包括電池動力曳引機、混合動力曳引機和燃料電池曳引機,每種曳引機都旨在滿足不同的作業需求。與其他配置相比,電池動力曳引機憑藉其更成熟的技術基礎和更成熟的商業化條件,佔據了市場主導地位。其簡化的架構降低了維護需求,減少了系統複雜性,並提高了擁有成本的可預測性。這些系統尤其適用於中短時農業作業,並且能夠很好地應對當前電池性能的局限性,尤其是在低功率和中功率的農業應用場景中。

低功率曳引機(定義為功率低於50馬力的曳引機)預計到2025年將佔據57.8%的市場佔有率。此類別的主導地位源自於其與電動驅動系統的高度親和性。低功率曳引機通常用於噴灑、犁地、運輸和農田管理等相對輕型的農業作業。這些作業週期短、扭力輸出適中,非常適合目前電池容量和充電基礎設施的限制。小規模農場、果園、葡萄園和零散農田的需求特別突出,因為在這些地區,機動性和精準性比高牽引力更為重要。較低的運作成本和簡化的充電要求進一步促進了對成本敏感的用戶對低功率曳引機的接受度。

預計2025年,美國電動曳引機市佔率將達到76%,市場規模將達8,130萬美元。美國之所以能主導地位,得益於其強大的農業機械生態系統、雄厚的投資能力以及對先進農業技術的早期應用。燃料成本上漲、勞動力短缺以及對提高營運效率的需求,正促使農民擴大採用電動曳引機。旨在推廣零排放設備的聯邦和州級獎勵計畫也加速了電動曳引機的普及,尤其是在那些制定了嚴格永續性目標的地區。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 環境法規和政策支持

- 技術進步和電池成本降低

- 營運成本和農業經濟效率

- 產業潛在風險與挑戰

- 較高的初始設定成本

- 充電基礎設施和營運限制

- 機會

- 與智慧農業和精密農業系統整合

- 來自小規模和特色農業領域的需求不斷成長

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 各地區價格波動

- 價格比較:電動曳引機 vs. 柴油曳引機

- 價格彈性和消費者價格敏感性

- 法律規範

- 農業機械排放標準與法規

- 政府補貼和獎勵計劃

- 安全和認證要求

- 進出口限制和貿易政策

- 農村電氣化政策

- 關於排碳權和永續性的監管要求

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 優先分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

- 貿易資料分析 - HS編碼:8701.24(新)(基於付費資料庫)

- 進出口數量和價值的變化趨勢

- 主要貿易走廊及關稅的影響

- 區域貿易流量分析

- HS編碼分類與貿易單據

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 精密農業(利用人工智慧進行田間最佳化)的整合

- 預測性維護與車隊管理的應用

- 風險、限制和監管考量

- 促進因素

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依實施方法分類,2022-2035年

- 電池式電動車

- 混合動力汽車

- 燃料電池汽車

第6章 市場估價與預測:依電池類型分類,2022-2035年

- 鋰離子

- 鉛酸電池

- 其他(所有固體、鈉離子等)

第7章 市場估計與預測:依產量分類,2022-2035年

- 低功率(低於50馬力)

- 中功率(50-100馬力)

- 高功率(超過100馬力)

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 農業

- 戶外工作

- 果園和葡萄園工作

- 畜牧業及酪農

- 其他

- 公共產業

- 景觀設計與場地管理

- 高爾夫球場和體育設施

- 地方政府與公共空間

- 工業的

- 建築工地作業

- 物料運輸及物流

- 地方政府服務和廢棄物管理

- 機場和港口營運

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AGCO Corporation

- Alke

- AutoNxt Automation Pvt. Ltd.

- Cellestial E-Mobility

- CLAAS

- CNH Industrial

- Deutz-Fahr(SDF Group)

- Escorts Kubota Limited

- Farmtrac(Escorts Group)

- John Deere(Deere & Company)

- Kubota Corporation

- Lely Group

- Mahindra & Mahindra

- Massey Ferguson Limited

- Monarch Tractor

- Motivo Engineering

- NAIO Technologies

- Solectrac

- Yanmar Holdings Co., Ltd.

- Ztractor

The Global Electric Tractor Market was valued at USD 245 million in 2025 and is estimated to grow at a CAGR of 22.7% to reach USD 1.95 billion by 2035.

The market is gaining strong momentum as agriculture increasingly shifts toward electrification to reduce emissions, lower operational costs, and improve long-term sustainability. Growing regulatory pressure to curb greenhouse gas emissions from off-road agricultural machinery is significantly accelerating adoption across key farming regions. Governments are also supporting this transition through financial incentives such as subsidies, tax benefits, and affordable financing programs, making electric tractors more commercially viable for farmers. At the same time, rapid advancements in battery systems and electric drivetrains are reshaping performance expectations. Improvements in energy density, charging speed, and battery lifespan are enabling longer operational cycles and broader use across farming applications. Declining battery costs are further reducing acquisition expenses and improving the total cost of ownership. Enhancements in power electronics are also improving torque delivery, allowing electric tractors to handle demanding agricultural workloads. With fewer mechanical components than conventional diesel models, these tractors require less maintenance and offer higher operational efficiency. As technology continues to mature, electric tractors are increasingly being recognized as practical, productivity-focused agricultural machines rather than experimental alternatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $245 Million |

| Forecast Value | $1.95 Billion |

| CAGR | 22.7% |

The battery electric tractors segment generated USD 176.3 million in 2025. Across propulsion types, the segment includes battery electric, hybrid electric, and fuel cell electric tractors, each designed to meet different operational needs. Battery electric models lead due to their more developed technology base and stronger commercial readiness compared to other configurations. Their simplified architecture supports lower maintenance requirements, reduced system complexity, and more predictable ownership costs. These systems are particularly effective for short- to medium-duration farming activities, aligning well with current battery performance limitations, especially in low- and mid-power agricultural use cases.

The low power segment, defined as tractors below 50 HP, held a share of 57.8% in 2025. This category leads due to its strong compatibility with electric drivetrain capabilities, as low-power tractors are typically used for lighter agricultural tasks such as spraying, cultivation, hauling, and field maintenance. These operations require shorter runtime cycles and moderate torque output, making them well-suited to current battery capacities and charging infrastructure constraints. Demand is particularly strong in small farms, orchards, vineyards, and fragmented landholdings where maneuverability and precision are more important than high pulling power. Lower purchase costs and simplified charging requirements further support widespread adoption among cost-sensitive users.

U.S. Electric Tractor Market accounted for 76% share in 2025, generating USD 81.3 million. The country's leadership position is supported by a strong agricultural machinery ecosystem, high investment capacity, and early adoption of advanced farming technologies. Farmers are increasingly turning toward electric tractors due to rising fuel expenses, labor shortages, and the need to improve operational efficiency. Supportive federal and state-level incentive programs aimed at promoting zero-emission equipment are also accelerating adoption, particularly in regions with stricter sustainability targets.

Major companies operating in the Global Electric Tractor Market include CNH Industrial, AGCO Corporation, John Deere (Deere & Company), Mahindra & Mahindra, Kubota Corporation, CLAAS, Massey Ferguson Limited, Yanmar Holdings Co., Ltd., Escorts Kubota Limited, Deutz-Fahr (SDF Group), Farmtrac (Escorts Group), Monarch Tractor, Solectrac, NAIO Technologies, AutoNxt Automation Pvt. Ltd., Cellestial E-Mobility, Alke, Lely Group, Motivo Engineering, and Ztractor. Companies in the Electric Tractor Market are focusing on strengthening competitiveness through continuous product innovation and advancement in battery and drivetrain technologies. Significant investments in R&D are enabling improvements in energy efficiency, torque performance, and charging speed. Manufacturers are also expanding production capabilities to scale output and reduce unit costs. Strategic collaborations with battery suppliers and technology firms help accelerate innovation cycles and improve supply chain stability. Many players are introducing flexible financing models and leasing options to increase affordability for farmers. Expansion into emerging agricultural markets is further supporting revenue diversification.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion type

- 2.2.3 Battery

- 2.2.4 Power

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Environmental regulations and policy support

- 3.2.1.2 Technological advancements and battery cost reduction

- 3.2.1.3 Operating cost efficiency and farm economics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial acquisition cost

- 3.2.2.2 Charging infrastructure and operational limitations

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart and precision farming systems

- 3.2.3.2 Growing demand from small and specialty farming segments

- 3.2.4 Growth potential analysis

- 3.2.5 Future market trends

- 3.2.6 Technology and innovation landscape

- 3.2.6.1 Current technological trends

- 3.2.6.2 Emerging technologies

- 3.2.7 Pricing Analysis (driven by primary research)

- 3.2.7.1 Historical price trend analysis

- 3.2.7.2 Regional Price Variations

- 3.2.7.3 Price Comparison: electric vs diesel tractors

- 3.2.7.4 Price elasticity & consumer sensitivity

- 3.2.8 Regulatory Framework

- 3.2.8.1 Emission standards & agricultural equipment regulations

- 3.2.8.2 Government subsidies & incentive programs

- 3.2.8.3 Safety & certification requirements

- 3.2.8.4 Import/export regulations & trade policies

- 3.2.8.5 Rural electrification policies

- 3.2.8.6 Carbon credit & sustainability mandates

- 3.2.9 Porter's five forces analysis

- 3.2.10 PESTEL analysis

- 3.2.11 Consumer behavior analysis

- 3.2.11.1 Purchasing patterns

- 3.2.11.2 Preference analysis

- 3.2.11.3 Regional variations in consumer behavior

- 3.2.11.4 Impact of e-commerce on buying decisions

- 3.2.12 Trade data analysis - HS Code: 8701.24 (new) (driven by paid database)

- 3.2.12.1 Import/export volume & value trends

- 3.2.12.2 Key trade corridors & tariff impact

- 3.2.12.3 Trade flow analysis by region

- 3.2.12.4 HS code classification & trade documentation

- 3.2.13 Impact of AI & Generative AI on the Market

- 3.2.13.1 AI-driven disruption of existing business models

- 3.2.13.2 GenAI use cases & adoption roadmap by segment

- 3.2.13.3 Precision agriculture integration (AI-enabled field optimization)

- 3.2.13.4 Predictive maintenance & fleet management applications

- 3.2.13.5 Risks, limitations & regulatory considerations

- 3.2.1 Growth drivers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Battery electric

- 5.3 Hybrid electric

- 5.4 Fuel cell electric

Chapter 6 Market Estimates and Forecast, By Battery, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 Lead-Acid

- 6.4 Others (solid-state, sodium-ion, etc.)

Chapter 7 Market Estimates and Forecast, By Power, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Low power (<50 HP)

- 7.3 Medium power (50-100 HP)

- 7.4 High power (>100 HP)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Agriculture

- 8.2.1 Field operations

- 8.2.2 Orchard & vineyard operations

- 8.2.3 Livestock & dairy farm applications

- 8.2.4 Others

- 8.3 Utility

- 8.3.1 Landscaping & grounds maintenance

- 8.3.2 Golf courses & sports fields

- 8.3.3 Municipal & public spaces

- 8.4 Industrial

- 8.4.1 Construction site operations

- 8.4.2 Material handling & logistics

- 8.4.3 Municipal services & waste management

- 8.4.4 Airport & port operations

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AGCO Corporation

- 11.2 Alke

- 11.3 AutoNxt Automation Pvt. Ltd.

- 11.4 Cellestial E-Mobility

- 11.5 CLAAS

- 11.6 CNH Industrial

- 11.7 Deutz-Fahr (SDF Group)

- 11.8 Escorts Kubota Limited

- 11.9 Farmtrac (Escorts Group)

- 11.10 John Deere (Deere & Company)

- 11.11 Kubota Corporation

- 11.12 Lely Group

- 11.13 Mahindra & Mahindra

- 11.14 Massey Ferguson Limited

- 11.15 Monarch Tractor

- 11.16 Motivo Engineering

- 11.17 NAIO Technologies

- 11.18 Solectrac

- 11.19 Yanmar Holdings Co., Ltd.

- 11.20 Ztractor

2026年全球電動曳引機市場報告

2026年全球電動曳引機市場報告 電動曳引機市場:2026-2032年全球市場預測(按曳引機類型、功率輸出、充電基礎設施、銷售管道和應用分類)農業電動曳引機市場:按馬力範圍、電池類型、曳引機類型、充電基礎設施和分銷管道分類,全球預測,2026-2032年

電動曳引機市場:2026-2032年全球市場預測(按曳引機類型、功率輸出、充電基礎設施、銷售管道和應用分類)農業電動曳引機市場:按馬力範圍、電池類型、曳引機類型、充電基礎設施和分銷管道分類,全球預測,2026-2032年 全球電動農業曳引機市場:市場規模、佔有率和趨勢分析(按類型、輸出功率、電池容量、電池類型、驅動系統、最終用途和地區分類),基於細分市場的預測(2026-2033 年)

全球電動農業曳引機市場:市場規模、佔有率和趨勢分析(按類型、輸出功率、電池容量、電池類型、驅動系統、最終用途和地區分類),基於細分市場的預測(2026-2033 年) 電動曳引機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球電動曳引機市場規模、佔有率、趨勢和成長分析報告:2026-2034年

電動曳引機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球電動曳引機市場規模、佔有率、趨勢和成長分析報告:2026-2034年 2032 年電動曳引機市場預測:按傳動系統、電池、動力、應用和地區分類的全球分析

2032 年電動曳引機市場預測:按傳動系統、電池、動力、應用和地區分類的全球分析 全球電動曳引機市場

全球電動曳引機市場 電動曳引機市場:推進力,電池,各輸出功率,各用途,各地區,機會,預測,2018年~2032年

電動曳引機市場:推進力,電池,各輸出功率,各用途,各地區,機會,預測,2018年~2032年 電動拖拉機市場:按類型、按推進系統、按電池容量、按輸出、按應用、按地區- 2031 年之前的世界預測

電動拖拉機市場:按類型、按推進系統、按電池容量、按輸出、按應用、按地區- 2031 年之前的世界預測