|

市場調查報告書

商品編碼

2027524

筆記型電腦市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Laptop Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

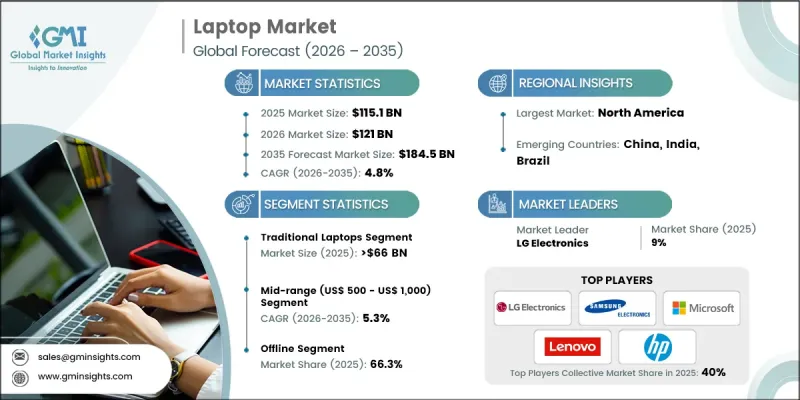

預計到 2025 年,全球筆記型電腦市場規模將達到 1,151 億美元,並以 4.8% 的複合年成長率成長,到 2035 年將達到 1,845 億美元。

市場擴張的驅動力來自遠端辦公模式的普及、混合式學習環境的興起以及對高效能、互聯可攜式運算設備日益成長的需求。消費者和企業都渴望擁有能夠流暢運行多任務、高速處理和高效電源管理的先進筆記型電腦。主要製造商之間的策略併購正在改變競爭格局,使他們能夠擴展產品系列併增強技術實力。這種行業重組正在加速包括標準筆記型電腦、二合一筆記型電腦、遊戲系統和可攜式機型在內的多個類別的創新。處理器技術、電池效率和整合軟體生態系統的持續進步進一步推動了市場需求。隨著數位轉型在整個行業中加速推進,筆記型電腦正成為生產力、通訊和娛樂的必備工具,其在不同用戶群中的重要性日益提升,並推動著市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 1151億美元 |

| 預測金額 | 1845億美元 |

| 複合年成長率 | 4.8% |

向智慧、高效能運算解決方案的轉變正在重新定義市場的產品預期。功能有限的傳統筆記型電腦正逐漸被配備人工智慧處理器、雲端整合和更長電池續航時間的先進系統所取代。這些創新使用戶能夠享受個人化的運算體驗、更強大的跨裝置連接以及針對各種任務最佳化的效能。筆記型電腦憑藉其便攜性、高效性和輕鬆處理複雜工作負載的能力,在專業人士、學生和遊戲玩家日益成長的需求推動下,仍然廣受歡迎。

傳統筆記型電腦市場預計到2025年將達到660億美元,到2035年將達到1003億美元。由於企業用戶、教育機構以及注重性價比、尋求可靠運算解決方案的消費者的穩定需求,該細分市場仍佔據主導地位。熟悉的設計、耐用性和廣泛的價格範圍是其持續成長的促進因素。儘管新型外形規格不斷湧現,傳統筆記型電腦仍然是滿足日常運算需求的實用之選,並保持其重要性。

預計到2025年,線下分銷管道將佔據66.3%的市場佔有率,並在2035年之前以4.5%的複合年成長率成長。實體店在購買過程中繼續發揮著至關重要的作用,它們提供親身體驗產品的機會、個人化支援以及即時供貨。這些優勢有助於消費者做出明智的購買決策,尤其是在評估產品做工、鍵盤手感和顯示性能等特性時。線下通路對於企業客戶和首次購買筆記型電腦的用戶尤其重要,有助於維持門市客流量和強勁的銷售業績。

預計到2025年,美國筆記型電腦市場規模將達到319億美元,繼續保持其作為該地區最穩定、成長最快的市場之一的地位。強勁的消費支出、數位技術的廣泛應用以及頻繁的技術升級正在推動市場的持續擴張。消費者對高階設備、遊戲筆記型電腦、專業系統和二合一筆記型電腦的需求依然強勁。成熟的零售網路和強大的電子商務生態系統進一步促進了市場成長,而消費者對先進運算解決方案日益成長的興趣也持續推動著創新和應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 成長促進因素

- 對遠距辦公和混合學習解決方案的需求日益成長

- 科技的快速發展

- 雲端運算和數位生態系統的擴展

- 產業潛在風險與挑戰

- 激烈的競爭壓力和對價格的敏感性

- 產品快速過時

- 機會

- 對DaaS(設備即服務)的需求日益成長

- 向人工智慧優先且互聯互通的生態系統轉型

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特的分析

- PESTEL 分析

- 貿易數據分析

- 進出口數量和價值的變化趨勢

- 主要貿易路線及關稅的影響

- 區域貿易政策的影響(中美貿易趨勢)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 預測分析在產品開發的應用

- 基礎設施和實施情況(基於初步調查)

- 按地區和購買者群體分類的採用率和滲透率(基於初步調查)

- 基礎設施投資的可擴展性限制和趨勢(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章:筆記型電腦市場估算與預測:依產品類型分類,2022-2035年

- 傳統筆記型電腦

- 二合一筆記型電腦

第6章:筆記型電腦市場估價與預測:依螢幕大小分類,2022-2035年

- 10.9 英吋或更小

- 11-14.9英寸

- 15-16.9 英寸

- 17吋或更大

第7章:筆記型電腦市場估算與預測:依價格區間分類,2022-2035年

- 經濟型(500美元以下)

- 中檔(500-1000美元)

- 高階(超過1000美元)

第8章 筆記型電腦市場估算與預測:依最終用途分類,2022-2035年

- 對於個人

- 商業的

- 對於企業

- 賭博

- 教育機構

- BFSI

- 其他(零售商店、創新工作室等)

- 工業的

第9章:筆記型電腦市場估算與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 企業網站

- 離線

- 多品牌商店

- 百貨公司

- 專賣店

- 其他零售店

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Acer

- Apple Inc.

- ASUSTeK Computer Inc.

- Dell Inc.

- Haier Inc.

- HP Inc.

- Huawei Device Co., Ltd.

- Lenovo

- LG Electronics

- Microsoft

- Micro-Star INT'L CO., LTD.

- Razer Inc.

- SAMSUNG

- SONY ELECTRONICS INC.

- Toshiba Corporation

The Global Laptop Market was valued at USD 115.1 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 184.5 billion by 2035.

Market expansion is driven by the increasing adoption of remote work models, hybrid learning environments, and the growing reliance on portable computing devices with enhanced performance and connectivity. Consumers and enterprises alike are seeking advanced laptops that deliver seamless multitasking, high-speed processing, and efficient power management. The competitive landscape is evolving through strategic mergers and acquisitions among leading manufacturers, enabling them to broaden product portfolios and strengthen technological capabilities. This consolidation is accelerating innovation across multiple categories, including standard laptops, convertible devices, gaming systems, and ultraportable models. Continuous advancements in processor technologies, battery efficiency, and integrated software ecosystems are further supporting demand. As digital transformation accelerates across industries, laptops are becoming essential tools for productivity, communication, and entertainment, reinforcing their importance across diverse user groups and driving long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $115.1 Billion |

| Forecast Value | $184.5 Billion |

| CAGR | 4.8% |

The shift toward intelligent and high-performance computing solutions is redefining product expectations in the market. Conventional laptops with limited capabilities are gradually being replaced by advanced systems featuring AI-enabled processors, cloud integration, and enhanced battery life. These innovations allow users to benefit from personalized computing experiences, improved connectivity across multiple devices, and optimized performance for various tasks. Increasing demand from professionals, students, and gaming enthusiasts continues to support adoption, as laptops offer portability, efficiency, and the ability to handle complex workloads with ease.

The traditional laptops segment generated USD 66 billion in 2025 and is projected to reach USD 100.3 billion by 2035. This segment remains dominant due to consistent demand from enterprise users, educational institutions, and cost-conscious consumers seeking reliable computing solutions. The familiar design, durability, and wide availability across different price points contribute to sustained growth. Traditional laptops continue to serve as a practical choice for everyday computing needs, ensuring their relevance despite the emergence of newer form factors.

The offline distribution segment accounted for 66.3% share in 2025 and is expected to grow at a CAGR of 4.5% through 2035. Physical retail outlets continue to play a crucial role in the purchasing process by offering hands-on product experiences, personalized assistance, and immediate product availability. These advantages help consumers make informed decisions, particularly when evaluating features such as build quality, keyboard comfort, and display performance. Offline channels remain especially important for enterprise buyers and first-time users, contributing to sustained foot traffic and strong sales performance.

United States Laptop Market reached USD 31.90 billion in 2025, maintaining its position as one of the most stable and high-growth markets in the region. Strong consumer spending, widespread digital adoption, and frequent technology upgrades support continued expansion. Demand for premium devices, gaming laptops, professional systems, and convertible models remains high. The presence of established retail networks and a robust e-commerce ecosystem further strengthens market growth, while increasing interest in advanced computing solutions continues to drive innovation and adoption.

Key players operating in the Global Laptop Market include Apple Inc. Dell Inc., HP Inc., Lenovo, Acer, ASUSTeK Computer Inc., Microsoft, Samsung, LG Electronics, Huawei Device Co., Ltd., Razer Inc., Micro-Star INT'L CO., LTD., Toshiba Corporation, Sony Electronics Inc., and Haier Inc. Companies in the Laptop Market are focusing on innovation, strategic partnerships, and product diversification to strengthen their competitive position. Significant investments in research and development are driving advancements in processor performance, battery efficiency, and AI-enabled features. Firms are expanding their product portfolios to cater to various consumer segments, including premium, gaming, and ultraportable categories. Strategic collaborations and mergers are helping companies enhance technological capabilities and global reach. Additionally, brands are leveraging digital marketing, e-commerce platforms, and strong retail networks to improve customer engagement and accessibility. Continuous focus on design, sustainability, and user experience further supports long-term growth and market differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Screen Size

- 2.2.4 Price Range

- 2.2.5 End User

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote work & hybrid learning solutions

- 3.2.1.2 Rapid technology advancements

- 3.2.1.3 Expansion of cloud computing & digital ecosystems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competitive pressure & price sensitivity

- 3.2.2.2 Fast product obsolescence

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for device-as-a-service

- 3.2.3.2 Shift toward AI-first and connected ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis

- 3.10.1 Import & Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.10.3 Regional Trade Policy Impact (US-China Trade Dynamics)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Predictive Analytics for Product Development

- 3.12 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.12.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.12.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Laptop Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Traditional Laptops

- 5.3 2-in-1 Laptops

Chapter 6 Laptop Market Estimates & Forecast, By Screen Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Up to 10.9 inch

- 6.3 11 to 14.9 inch

- 6.4 15 to 16.9 inch

- 6.5 Above 17 inches

Chapter 7 Laptop Market Estimates & Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Economy (Up to US$ 500)

- 7.3 Mid-range (US$ 500 - US$ 1,000)

- 7.4 High (Above US$ 1,000)

Chapter 8 Laptop Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

- 8.3.1 Corporate

- 8.3.2 Gaming

- 8.3.3 Educational Institutes

- 8.3.4 BFSI

- 8.3.5 Others (Retail stores, creative studios, etc.)

- 8.4 Industrial

Chapter 9 Laptop Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-Commerce Sites

- 9.2.2 Company Website

- 9.3 Offline

- 9.3.1 Multi-brand Stores

- 9.3.2 Departmental Stores

- 9.3.3 Specialty Stores

- 9.3.4 Other Retail Stores

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Acer

- 11.2 Apple Inc.

- 11.3 ASUSTeK Computer Inc.

- 11.4 Dell Inc.

- 11.5 Haier Inc.

- 11.6 HP Inc.

- 11.7 Huawei Device Co., Ltd.

- 11.8 Lenovo

- 11.9 LG Electronics

- 11.10 Microsoft

- 11.11 Micro-Star INT'L CO., LTD.

- 11.12 Razer Inc.

- 11.13 SAMSUNG

- 11.14 SONY ELECTRONICS INC.

- 11.15 Toshiba Corporation

筆記型電腦市場-2026-2032年全球市場預測遊戲筆記型電腦市場:2026-2032年全球市場預測(螢幕大小、記憶體容量、儲存類型、顯示解析度、更新率、外形規格、銷售管道和最終用戶分類)

筆記型電腦市場-2026-2032年全球市場預測遊戲筆記型電腦市場:2026-2032年全球市場預測(螢幕大小、記憶體容量、儲存類型、顯示解析度、更新率、外形規格、銷售管道和最終用戶分類) 人工智慧筆記型電腦市場:按產品類型和地區分類

人工智慧筆記型電腦市場:按產品類型和地區分類 筆記型電腦市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和功能分類

筆記型電腦市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和功能分類 筆記型電腦市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、螢幕大小、價格範圍、應用、分銷管道、地區和競爭格局分類),2021-2031年遊戲筆記型電腦市場 - 全球產業規模、佔有率、趨勢、機會、預測:按最終用戶、處理器、組件、地區和競爭格局分類,2021-2031年

筆記型電腦市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、螢幕大小、價格範圍、應用、分銷管道、地區和競爭格局分類),2021-2031年遊戲筆記型電腦市場 - 全球產業規模、佔有率、趨勢、機會、預測:按最終用戶、處理器、組件、地區和競爭格局分類,2021-2031年 日本筆記型電腦市場報告:按類型、螢幕大小、價格範圍、應用和地區分類(2026-2034年)

日本筆記型電腦市場報告:按類型、螢幕大小、價格範圍、應用和地區分類(2026-2034年) 筆記型電腦市場規模、佔有率和成長分析(按產品類型、螢幕大小、處理器類型、作業系統、價格分佈、最終用戶、分銷管道和地區分類)—2026-2033年行業預測

筆記型電腦市場規模、佔有率和成長分析(按產品類型、螢幕大小、處理器類型、作業系統、價格分佈、最終用戶、分銷管道和地區分類)—2026-2033年行業預測 Chromebook市場規模、佔有率和成長分析(按類型、產品類型、螢幕類型、處理器類型、儲存容量、應用和地區分類)-2026-2033年產業預測

Chromebook市場規模、佔有率和成長分析(按類型、產品類型、螢幕類型、處理器類型、儲存容量、應用和地區分類)-2026-2033年產業預測 遊戲筆記型電腦和桌上型電腦:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年)

遊戲筆記型電腦和桌上型電腦:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年)