|

市場調查報告書

商品編碼

2019237

人工草皮市場機會、成長要素、產業趨勢分析及2026-2035年預測Synthetic Turf Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

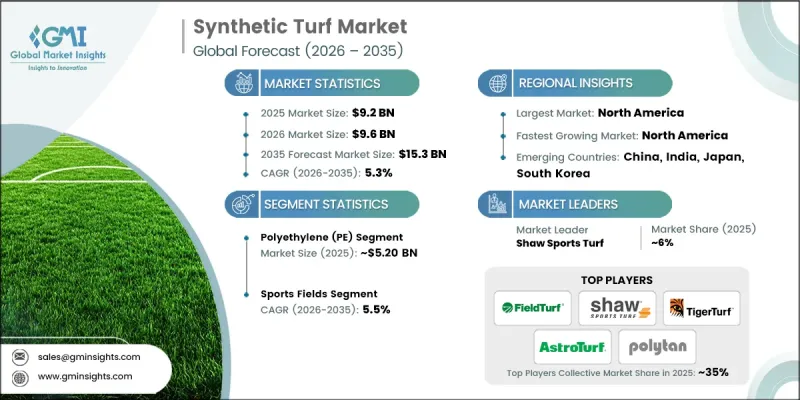

全球人造草坪市場預計到 2025 年將價值 92 億美元,預計到 2035 年將以 5.3% 的複合年成長率成長至 153 億美元。

為了促進體育活動和參與,政府和私人機構正增加對體育場館、訓練場地和社區體育設施的投資。人工草皮因其耐用性、可靠性和低維護成本而備受職業聯賽、中小學和大學的青睞。水資源短缺和氣候變遷等環境因素也加速了人工草皮的普及,因為它能減少用水量和維護成本。人造草坪用途人工草皮,可滿足多種運動項目的需求,加之材料技術的進步提高了運動員的安全、舒適度和運動表現,進一步增強了其吸引力。此外,人們對住宅和商業房地產景觀美化的日益關注也創造了新的市場機遇,因為人工草皮為城市空間和小規模戶外區域提供了一種美觀且無需維護的選擇。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 92億美元 |

| 預測金額 | 153億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,聚乙烯市場銷售額將達到52億美元,並在2035年之前以5.5%的複合年成長率成長。聚乙烯質地柔軟、耐用,外觀酷似天然草坪,使其成為運動場、休閒區和住宅應用的理想材料。其抗紫外線、保色性和在惡劣條件下的耐磨性進一步提升了其受歡迎程度,並確保了其長期性能。

預計到 2025 年,運動場地市佔率將達到 59%,並從 2026 年到 2035 年以 5.5% 的複合年成長率成長。專業球隊、學校和市政休閒設施的高需求正在推動人造草皮的普及,因為人工草皮能夠保證場地平整、延長比賽賽季並減少維護需求。

美國人造草坪市場預計到2025年將達到27.1億美元,到2035年將以5.7%的複合年成長率成長。市場需求主要來自體育組織、教育機構、住宅和商業設施。人工草皮的應用不僅支持體育項目、節水景觀設計,還能提升商業和住宅空間的美觀。此外,寵物草坪、遊樂場地面材料和屋頂鋪設等特殊應用也正在拓展市場成長潛力。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 增加對體育基礎設施和休閒設施的投資

- 水資源短缺日益嚴重,人們對環境永續性的擔憂也日益加劇。

- 住宅和商業景觀應用範圍的擴大

- 陷阱與挑戰

- 前期實施成本高

- 與微塑膠的釋放和處置相關的環境問題

- 機會

- 開發環保可回收的人工草皮材料

- 對寵物友善和特殊用途草坪的需求不斷成長。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢和價格分析(基於初步調查)

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 價格波動與材料類型和應用有關

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 區域貿易趨勢和跨境分銷

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的製造流程轉型

- 生成式人工智慧的應用案例(設計最佳化、預測性維護)

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的已安裝產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依材料分類,2022-2035年

- 聚乙烯(PE)

- 聚丙烯(PP)

- 尼龍

第6章 市場估價與預測:依填充材類型分類,2022-2035年

- 蛤殼橡膠

- 塗層砂

- 有機填充材

- 熱可塑性橡膠(TPE)

- 無填充材系統

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 運動場

- 足球

- 棒球

- 高爾夫(果嶺、發球檯)

- 其他運動(曲棍球、橄欖球等)

- 住宅景觀設計

- 商業景觀設計

- 其他(屋頂花園、寵物人工草皮等)

第8章 市場估算與預測:依銷售管道分類,2022-2035年

- 線上

- 離線

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- AstroTurf

- CCGrass

- EasyTurf

- FieldTurf

- ForeverLawn

- Global Syn-Turf

- Hellas Construction

- K9Grass

- Polytan

- Shaw Sports Turf

- Sprinturf

- SYNLawn

- Synthetic Turf International

- Tarkett Sports

- TigerTurf

The Global Synthetic Turf Market was valued at USD 9.2 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 15.3 billion by 2035.

Governments and private organizations are increasingly funding stadiums, training grounds, and community sports facilities to encourage physical activity and sports participation. Synthetic turf is favored in professional leagues, schools, and universities for its durability, reliability, and low-maintenance advantages. Environmental factors such as water scarcity and climate change are accelerating adoption, as synthetic surfaces reduce water usage and maintenance efforts. Its versatility for multiple sports, combined with advancements in materials enhancing player safety, comfort, and performance, has broadened its appeal. Additionally, growing interest in residential and commercial landscaping is creating new market opportunities, as synthetic turf offers a visually appealing, maintenance-free alternative for urban spaces and small outdoor areas.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.2 Billion |

| Forecast Value | $15.3 Billion |

| CAGR | 5.3% |

The polyethylene segment generated USD 5.20 billion in 2025 and is expected to grow at a CAGR of 5.5% through 2035. Its soft texture, durability, and grass-like appearance make polyethylene ideal for sports fields, recreational zones, and residential applications. UV resistance, color retention, and resilience under heavy use reinforce its popularity, ensuring long-lasting performance.

The sports fields segment accounted for 59% share in 2025, with a projected CAGR of 5.5% from 2026 to 2035. High demand from professional teams, schools, and municipal recreation facilities drives adoption, as synthetic turf ensures consistent surfaces, extended play seasons, and reduced maintenance requirements.

U.S. Synthetic Turf Market reached USD 2.71 billion in 2025, with a forecasted CAGR of 5.7% through 2035. Demand stems from sports organizations, educational institutions, residential customers, and commercial properties. Synthetic turf adoption supports athletic programs, water-efficient landscaping, and aesthetic enhancements in commercial and residential spaces, while specialty applications like pet turf, playground surfaces, and rooftop installations expand growth potential.

Key players in the Global Synthetic Turf Market include FieldTurf, SYNLawn, ForeverLawn, AstroTurf, Sprinturf, CCGrass, K9Grass, Tarkett Sports, EasyTurf, Shaw Sports Turf, Polytan, Synthetic Turf International, TigerTurf, Global Syn-Turf, and Hellas Construction. Companies in the Global Synthetic Turf Market strengthen their foothold through continuous product innovation, developing high-performance, durable, and visually appealing turf systems for diverse applications. Strategic partnerships with sports organizations, educational institutions, and landscaping contractors enhance distribution and brand visibility. Investment in R&D to improve UV resistance, player safety, and environmental sustainability drives competitive advantage. Expanding presence in emerging markets, offering customizable solutions, and providing installation and maintenance services reinforce customer loyalty. Additionally, digital marketing campaigns, direct-to-consumer sales channels, and collaborations with residential and commercial developers further consolidate market position and stimulate adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Infill Type

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing investment in sports infrastructure and recreational facilities

- 3.2.1.2 Rising water scarcity and environmental sustainability concerns

- 3.2.1.3 Expansion of residential and commercial landscaping applications

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial installation costs

- 3.2.2.2 Environmental concerns related to microplastic shedding and disposal

- 3.2.3 Opportunities

- 3.2.3.1 Development of eco-friendly and recyclable synthetic turf materials

- 3.2.3.2 Growing demand for pet-friendly and specialty turf applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends Pricing Analysis (Driven by Primary Research)

- 3.6.1 Pricing Analysis (Driven by Primary Research)

- 3.6.2 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.3 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.6.4 Price Variation by Material Type & Application

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 Regional Trade Dynamics & Cross-border Flow

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Manufacturing Processes

- 3.11.2 GenAI Use Cases (Design Optimization, Predictive Maintenance)

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Billions Square Feet)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.3 Polypropylene (PP)

- 5.4 Nylon

Chapter 6 Market Estimates & Forecast, By Infill Type, 2022 - 2035, (USD Billion) (Billions Square Feet)

- 6.1 Key trends

- 6.2 Crumb Rubber

- 6.3 Coated Sand

- 6.4 Organic Infill

- 6.5 Thermoplastic Elastomer (TPE)

- 6.6 Infill-Free Systems

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Billions Square Feet)

- 7.1 Key trends

- 7.2 Sports Fields

- 7.2.1 Soccer/Football

- 7.2.2 Baseball

- 7.2.3 Golf (putting greens, tee lines)

- 7.2.4 Others (Hockey, Rugby, Etc)

- 7.3 Residential Landscaping

- 7.4 Commercial Landscaping

- 7.5 Others (Rooftop Gardens, Pet Turf, Etc)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Billions Square Feet)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Billions Square Feet)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AstroTurf

- 10.2 CCGrass

- 10.3 EasyTurf

- 10.4 FieldTurf

- 10.5 ForeverLawn

- 10.6 Global Syn-Turf

- 10.7 Hellas Construction

- 10.8 K9Grass

- 10.9 Polytan

- 10.10 Shaw Sports Turf

- 10.11 Sprinturf

- 10.12 SYNLawn

- 10.13 Synthetic Turf International

- 10.14 Tarkett Sports

- 10.15 TigerTurf