|

市場調查報告書

商品編碼

2019235

汽車燃油供應幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。Automotive Fuel Feed Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

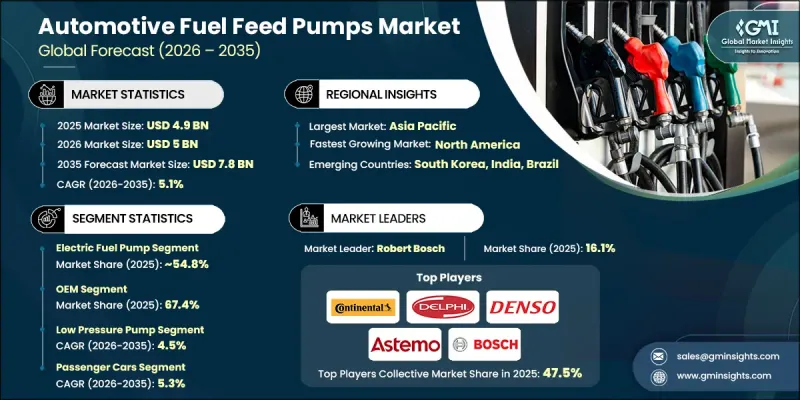

全球汽車燃油泵市場預計到 2025 年將價值 49 億美元,預計到 2035 年將以 5.1% 的複合年成長率成長至 78 億美元。

燃油泵在汽油和柴油系統中都發揮著至關重要的作用,確保燃油的精準輸送,因此,燃油泵市場的成長與內燃機汽車的持續生產和需求密切相關。開發中地區都市化的加速和中產階級的壯大推動了汽車保有量的成長,尤其是在成本敏感型市場,傳統燃油汽車仍然比替代技術更容易獲得。新興經濟體的汽車製造業持續擴張,對關鍵引擎零件的需求也持續成長。儘管移動出行解決方案的進步正在逐步改變汽車產業,但由於基礎設施的限制和成本因素,傳統動力傳動系統系統仍然佔據著重要地位。因此,燃油泵仍然是汽車價值鏈中不可或缺的組成部分,支撐著各種類型車輛的效率、性能和運作可靠性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 49億美元 |

| 預測金額 | 78億美元 |

| 複合年成長率 | 5.1% |

柴油引擎在全球交通運輸領域,尤其是在商用車領域,仍然發揮著至關重要的作用。儘管法規結構正在逐步變化,但在一些排放氣體法規相對寬鬆的地區,內燃機汽車預計仍將保持重要地位。在許多開發中國家,由於汽油和柴油汽車價格低廉且基礎設施落後,人們仍然依賴這些車輛。雖然一些地區正在加速向更清潔的出行方式轉型,但替代技術的應用仍在進行中,預計在整個預測期內,對傳統汽車系統的需求將保持強勁。

到2025年,電動燃油幫浦市佔率將達到54.8%,市場規模將達27億美元。這些燃油幫浦之所以廣受歡迎,是因為它們能夠維持穩定的燃油壓力並最佳化燃油輸送性能。這對於採用電子燃油噴射的現代化引擎系統而言至關重要。與機械燃油泵不同,電動燃油泵的運作不受引擎轉速的影響,有助於提高燃油效率、增強引擎性能並符合排放氣體法規。這些優勢使得電動燃油幫浦成為製造商的首選。

預計到2025年,OEM(整車製造商)市佔率將達到67.4%,市場規模將達33億美元。汽車生產的持續擴張進一步鞏固了這個細分市場,因為OEM廠商直接為新車組裝提供燃油幫浦。隨著對先進燃油供應系統的依賴性不斷增強,製造商越來越重視從認證供應商採購零件,以確保品質和性能標準。這一趨勢正在推動OEM主導的銷售管道擴張,這些管道透過與新車生產的持續整合,持續超越售後市場的需求。

美國汽車燃油泵市場預計到2025年將達到8.207億美元,並在2026年至2035年間以6.1%的複合年成長率成長。該地區的市場趨勢與內燃機汽車的生產和銷售密切相關。儘管替代動力技術的應用正在逐步增加,但傳統汽車仍佔據汽車總量的很大一部分。這種持續的市場佔有率支撐了汽油和柴油燃油泵的持續需求。北美仍然是領先的區域市場,其中美國佔據了整體需求的很大一部分。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球汽車產量和銷售成長

- 嚴格的排放氣體法規正在推動燃油噴射技術的應用。

- 車輛老化導致售後市場需求擴大

- 電動燃油幫浦系統的技術進步

- 產業潛在風險與挑戰

- 汽車產業的快速電氣化

- 先進高壓燃油幫高成本

- 市場機遇

- 在車輛擁有量不斷成長的新興市場,業務正在擴張。

- 開發一種多燃料相容的泵浦系統

- 已開發國家售後市場的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國 - 美國環保署 (EPA)

- 美國 - 加州空氣資源委員會 (CARB)

- 加拿大 - 加拿大運輸部

- 歐洲

- 德國 - 聯邦機動車輛管理局 (KBA)

- 英國- 車輛認證局 (VCA)

- 亞太地區

- 中國 - 工業及資訊化部(工信部)

- 印度汽車研究協會 (ARAI)

- 拉丁美洲

- 巴西 - 巴西環境與可再生自然資源研究所 (IBAMA)

- 墨西哥 - 環境與自然資源部 (SEMARNAT)

- 中東和非洲

- 沙烏地阿拉伯 - 沙烏地阿拉伯標準、計量和品質組織 (SASO)

- 南非 - 南非標準局 (SABS)

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 電動油箱燃油幫浦

- 機械燃油幫浦

- 變速燃油泵

- 新興技術

- 無刷電動燃油泵

- 電子控制智慧燃油泵

- 多燃料相容泵浦系統

- 目前技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 專利趨勢(基於初步調查)

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的裝置容量

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 成本細分分析

- 產品生命週期與升級週期

- 依生產年份和地區進行車輛更換週期分析。

- 零件相容性和客製化

- 電氣化對燃油供應幫浦的影響

- 對內燃機車(ICE)的需求下降

- 混合動力汽車燃料系統技術的演變

- 電動車零件更換頻率降低

- 案例研究

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依泵浦類型分類,2022-2035年

- 機械燃油幫浦

- 電動燃油幫浦

- 水箱內的電動泵

- 直列式電動泵

- 渦輪泵

第6章 市場估計與預測:依壓力程度分類,2022-2035年

- 低壓泵

- 高壓幫浦

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第8章 市場估算與預測:依燃料類型分類,2022-2035年

- 汽油

- 柴油引擎

- 替代燃料

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 波蘭

- 荷蘭

- 挪威

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Robert Bosch

- Denso

- Continental

- Delphi

- Walbro

- HELLA

- AC Delco(GM)

- TI Automotive

- Valeo

- 本地公司

- Mikuni

- Aisin

- Magneti Marelli

- GMB

- Hitachi Astemo

- Carter Fuel Systems

- 新興企業

- EKU

- Spectra Premium

- Holley

- Fuelab

- SHW

The Global Automotive Fuel Feed Pumps Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 7.8 billion by 2035.

Market growth remains closely tied to the continued production and demand for internal combustion engine vehicles, as fuel feed pumps play a critical role in ensuring precise fuel delivery in both gasoline and diesel systems. Rising urbanization and the expansion of middle-income populations across developing regions are contributing to increased vehicle ownership, particularly in cost-sensitive markets where conventional fuel-powered vehicles remain more accessible than alternative technologies. The automotive manufacturing sector continues to expand across emerging economies, creating sustained demand for essential engine components. While advancements in mobility solutions are gradually reshaping the industry, traditional powertrain systems continue to hold a strong presence due to infrastructure limitations and cost considerations. As a result, fuel feed pumps remain a vital component within the automotive value chain, supporting efficiency, performance, and operational reliability across a wide range of vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 5.1% |

Diesel-powered engines continue to play a significant role in global transportation, particularly within commercial vehicle segments. Despite gradual shifts in regulatory frameworks, internal combustion engine vehicles are expected to maintain relevance in several regions where emission regulations are less restrictive. Many developing economies continue to depend heavily on gasoline and diesel vehicles due to affordability and infrastructure readiness. Although certain regions are accelerating the transition toward cleaner mobility solutions, broader adoption of alternative technologies is still evolving, allowing conventional vehicle systems to sustain demand over the forecast period.

The electric fuel pump segment held a 54.8% share in 2025, generating USD 2.7 billion. These pumps are widely preferred due to their ability to maintain consistent fuel pressure and optimize delivery performance, which is essential for modern engine systems utilizing electronic fuel injection. Unlike mechanical variants, electric pumps operate independently of engine speed, contributing to improved efficiency, enhanced engine performance, and better alignment with emission requirements. These advantages have positioned electric fuel pumps as a preferred choice among manufacturers.

The OEM segment held a 67.4% share in 2025, generating USD 3.3 billion. Growth in vehicle production continues to strengthen this segment, as original equipment manufacturers supply fuel feed pumps directly for new vehicle assembly. Increasing reliance on advanced fuel delivery systems has led manufacturers to prioritize sourcing components from approved suppliers, ensuring quality and performance standards. This trend supports the expansion of OEM-driven sales channels, which continue to outperform aftermarket demand due to consistent integration in new vehicle production.

United States Automotive Fuel Feed Pumps Market reached USD 820.7 million in 2025 and is projected to grow at a CAGR of 6.1% from 2026 to 2035. Market performance in the region remains closely aligned with the production and sales of internal combustion engine vehicles. Although the adoption of alternative propulsion technologies is gradually increasing, conventional vehicles continue to represent a significant share of the overall fleet. This sustained presence supports ongoing demand for fuel feed pumps across both gasoline and diesel applications. North America remains a key regional market, with the United States contributing a substantial portion of overall demand.

Key companies operating in the Global Automotive Fuel Feed Pumps Market include Aisin, Carter Fuel Systems, Continental, Delphi, Denso, Hitachi Astemo, Magneti Marelli, Robert Bosch, TI Automotive (AVIC), and Walbro. Companies in the Automotive Fuel Feed Pumps Market are strengthening their competitive position through continuous product innovation, strategic collaborations, and expansion into high-growth regions. A key focus is being placed on developing advanced fuel delivery systems that enhance efficiency and meet evolving emission standards. Manufacturers are investing in research and development to improve durability, precision, and integration with modern engine technologies. Partnerships with automotive manufacturers are helping secure long-term supply agreements and strengthen distribution networks. Additionally, companies are optimizing production capabilities and supply chain operations to remain cost-competitive. Expanding product portfolios and targeting emerging markets are also critical strategies being adopted to capture new growth opportunities and reinforce market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Pump

- 2.2.3 Pressure

- 2.2.4 Vehicle

- 2.2.5 Fuel

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production & sales

- 3.2.1.2 Stringent emission norms driving fuel injection technology adoption

- 3.2.1.3 Growing aftermarket demand due to aging vehicle fleet

- 3.2.1.4 Technological advancements in electric fuel pump systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid electrification of automotive industry

- 3.2.2.2 High cost of advanced high-pressure fuel pumps

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing vehicle ownership

- 3.2.3.2 Development of multi-fuel compatible pump systems

- 3.2.3.3 Aftermarket growth in developed markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - U.S. Environmental Protection Agency (EPA)

- 3.4.1.2 U.S. - California Air Resources Board (CARB)

- 3.4.1.3 Canada - Transport Canada

- 3.4.2 Europe

- 3.4.2.1 Germany - Kraftfahrt-Bundesamt (KBA)

- 3.4.2.2 UK - Vehicle Certification Agency (VCA)

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.4.3.2 India - Automotive Research Association of India (ARAI)

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Instituto Brasileiro do Meio Ambiente e dos Recursos Naturais Renovaveis (IBAMA)

- 3.4.4.2 Mexico - Secretaria de Medio Ambiente y Recursos Naturales (SEMARNAT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Arabia - Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.2 South Africa - South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Electric In-Tank Fuel Pumps

- 3.8.1.2 Mechanical Fuel Pumps

- 3.8.1.3 Variable Speed Fuel Pumps

- 3.8.2 Emerging technologies

- 3.8.2.1 Brushless Electric Fuel Pumps

- 3.8.2.2 Smart Fuel Pumps with Electronic Control

- 3.8.2.3 Multi-Fuel Compatible Pump Systems

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Cost breakdown analysis

- 3.15 Product lifecycle & upgrade cycles

- 3.15.1 Replacement Cycle Analysis by Vehicle Age & Region

- 3.15.2 Part Compatibility and Customization

- 3.16 Impact of electrification on fuel feed pumps

- 3.16.1 reduction in internal combustion engine (ICE) vehicle demand

- 3.16.2 Evolving fuel system technology for hybrid vehicles

- 3.16.3 Declining replacement frequency for EV components

- 3.17 Case studies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Pump, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical fuel pump

- 5.3 Electric fuel pump

- 5.3.1 In-tank electric pumps

- 5.3.2 In-line electric pumps

- 5.4 Turbo pump

Chapter 6 Market Estimates & Forecast, By Pressure, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Low pressure pump

- 6.3 High-pressure pump

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Gasoline/Petrol

- 8.3 Diesel

- 8.4 Alternative fuels

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.3.8 Norway

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Robert Bosch

- 11.1.2 Denso

- 11.1.3 Continental

- 11.1.4 Delphi

- 11.1.5 Walbro

- 11.1.6 HELLA

- 11.1.7 AC Delco (GM)

- 11.1.8 TI Automotive

- 11.1.9 Valeo

- 11.2 Regional players

- 11.2.1 Mikuni

- 11.2.2 Aisin

- 11.2.3 Magneti Marelli

- 11.2.4 GMB

- 11.2.5 Hitachi Astemo

- 11.2.6 Carter Fuel Systems

- 11.3 Emerging players

- 11.3.1 EKU

- 11.3.2 Spectra Premium

- 11.3.3 Holley

- 11.3.4 Fuelab

- 11.3.5 SHW

全球汽車幫浦市場:按類型、技術、容量、應用、車輛類型、電動車類型、非公路用車輛類型、銷售管道和地區分類-預測至2035年

全球汽車幫浦市場:按類型、技術、容量、應用、車輛類型、電動車類型、非公路用車輛類型、銷售管道和地區分類-預測至2035年 汽車幫浦市場:按泵浦類型、車輛型號、燃料類型和銷售管道分類-2026-2032年全球市場預測

汽車幫浦市場:按泵浦類型、車輛型號、燃料類型和銷售管道分類-2026-2032年全球市場預測 汽車幫浦市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝方式分類

汽車幫浦市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝方式分類 汽車溫度控管系統幫浦市場:機會、成長促進因素、產業趨勢分析及預測(2026-2035)

汽車溫度控管系統幫浦市場:機會、成長促進因素、產業趨勢分析及預測(2026-2035) 乘用車泵市場-全球產業規模、佔有率、趨勢、機會與預測:按泵類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車空調壓力調節器市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、車輛類型、需求類別、地區和競爭對手分類,2021-2031年

乘用車泵市場-全球產業規模、佔有率、趨勢、機會與預測:按泵類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車空調壓力調節器市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、車輛類型、需求類別、地區和競爭對手分類,2021-2031年 汽車幫浦市場:按泵浦類型、銷售管道、技術、車輛類型和地區分類。

汽車幫浦市場:按泵浦類型、銷售管道、技術、車輛類型和地區分類。 2026年全球汽車幫浦市場報告汽車燃油輸送幫浦市場:按應用、幫浦類型、燃油類型、銷售管道和車輛類型分類-2026-2032年全球市場預測汽車燃油輸送幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。

2026年全球汽車幫浦市場報告汽車燃油輸送幫浦市場:按應用、幫浦類型、燃油類型、銷售管道和車輛類型分類-2026-2032年全球市場預測汽車燃油輸送幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。