|

市場調查報告書

商品編碼

2019064

汽車燃油輸送幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。Automotive Fuel Transfer Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

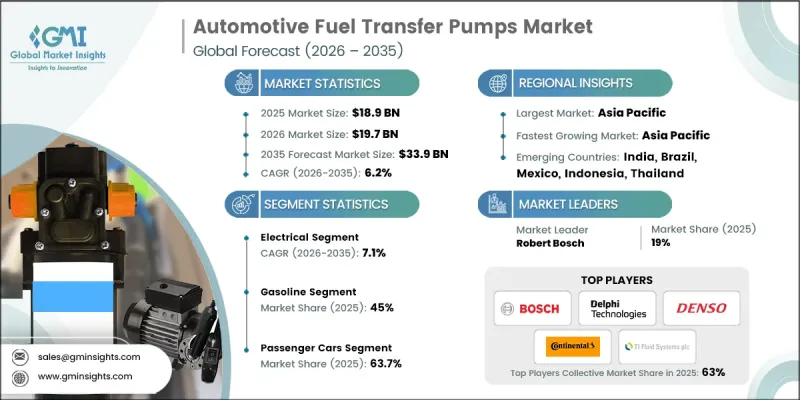

2025年全球汽車燃油輸送泵市場規模預計為189億美元,預計到2035年將以6.2%的複合年成長率成長至339億美元。

汽車燃油輸送泵市場的發展主要得益於人們對內燃機汽車的持續依賴,而高效的燃油輸送系統在這些車輛中仍然至關重要。乘用車和商用車產量的成長,使得原廠配套(OEM)和售後市場對燃油輸送幫浦的需求持續強勁。此外,物流和貨運行業的快速發展也推動了汽車燃油輸送泵市場的發展,全球商用車數量不斷成長。這些車輛需要耐用且高效的燃油系統來支援其長時間的運作。因此,對高性能燃油輸送幫浦的需求持續上升。同時,製造商正致力於提高系統的可靠性和運作效率,進一步促進了汽車燃油輸送泵市場在多個車型類別中的擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 189億美元 |

| 預測金額 | 339億美元 |

| 複合年成長率 | 6.2% |

全球汽車保有量的老舊化也對汽車燃油輸送泵市場造成了影響,推動了對替換零件的需求。隨著車輛老化,燃油系統關鍵部件的維護和更換需求持續成長。運作負荷和長期使用造成的磨損加劇進一步刺激了售後市場需求。在保有量高的地區,這種趨勢尤其明顯,因為較長的保養週期為燃油輸送幫浦的更換需求提供了穩定的基礎。

預計到2025年,電動車市佔率將達到58%,並在2026年至2035年間以7.1%的複合年成長率成長。現代汽車中電子燃油輸送系統的日益普及,對精確的流量控制和穩定的壓力要求極高,這推動了電動車市場的重要性日益提升。汽車燃油輸送幫浦市場正受惠於電動幫浦設計的進步,包括耐久性、耐磨性和重量的降低。這些進步不僅有助於滿足能源效率標準,還有助於提升車輛的整體性能。

預計到2025年,汽油車市佔率將達到45%,並在2035年之前以6.1%的複合年成長率成長。汽油車的持續普及支撐了這個市場主導地位,因為汽油車需要可靠的燃油輸送系統。汽車燃油輸送泵市場受益於強勁的產量和持續的替換需求,預計OEM和售後市場都將持續成長。

預計到2025年,美國汽車燃油輸送幫浦市場規模將達43億美元。美國市場正因消費者對配備耐用燃油系統和高性能車輛的強勁需求而不斷擴張。龐大的汽車保有量和較長的使用壽命週期支撐著這個市場,從而創造了穩定的更換需求。隨著燃油系統部件維護需求的持續成長,完善的服務網路和強大的售後市場生態系統正在推動市場進一步成長。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球汽車產量增加

- 商用和物流車輛數量不斷增加

- 汽車售後市場需求擴張

- 燃油噴射系統的應用日益普及

- 產業潛在風險與挑戰

- 快速過渡到電動車

- 燃油價格波動對車輛使用的影響

- 市場機遇

- 新興汽車市場的成長

- 高效率電動燃油幫浦的研製

- 擴大生質燃料和替代燃料汽車的使用

- 來自越野車和工業車輛的需求增加。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國環保署燃油系統法規

- 加州空氣資源委員會 (CARB) 標準

- 歐洲

- 歐6/歐7排放氣體法規

- ECE R67/R110燃油系統法規

- 亞太地區

- 中國第六階段排放氣體標準

- 日本JIS燃油系統標準/JARI指南

- 拉丁美洲

- 巴西 PROCONVE

- ABNT NBR 燃油系統標準

- 中東和非洲

- 阿拉伯聯合大公國ESMA燃油系統與排放標準

- 南非標準局燃油系統法規

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 成本細分分析

- 專利分析(基於初步研究)

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、局限性和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依類型分類,2022-2035年

- 機械的

- 電

第6章 市場估算與預測:依燃料類型分類,2022-2035年

- 汽油

- 柴油引擎

- 乙醇/生質燃料

- LPG/CNG

- 其他替代燃料

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- LCV

- MCV

- 重型商用車(HCV)

- 摩托車

第8章 市場估算與預測:依銷售管道分類,2022-2035年

- OEM(Original Equipment Manufacturer)

- 售後市場

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Aisin Seiki

- Continental Automotive

- Delphi Technologies

- Denso

- Hitachi Astemo

- Magnetti Marelli

- Mitsubishi Electric

- Pierburg(Rheinmetall)

- Robert Bosch

- TI Fluid Systems

- 本地公司

- Airtex Pumps

- Carter Fuel Systems

- GMB

- Spectra Premium

- Stanadyne

- UFI Filters

- Walbro

- 新興企業

- Cummins Fuel Systems

- Edelbrock

- Holley Performance Products

The Global Automotive Fuel Transfer Pumps Market was valued at USD 18.9 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 33.9 billion by 2035.

The automotive fuel transfer pumps market is driven by the continued reliance on internal combustion engine vehicles, where efficient fuel delivery systems remain essential. Increasing production of passenger and commercial vehicles is creating sustained demand for fuel transfer pumps across original equipment and replacement channels. The automotive fuel transfer pumps market is also benefiting from the rapid growth of logistics and freight transportation, which is expanding the global fleet of commercial vehicles. These vehicles require durable and efficient fuel systems to support extended operational cycles. As a result, demand for high-performance fuel transfer pumps continues to rise. In addition, manufacturers are focusing on improving system reliability and operational efficiency, which is further supporting the expansion of the automotive fuel transfer pumps market across multiple vehicle categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.9 Billion |

| Forecast Value | $33.9 Billion |

| CAGR | 6.2% |

The automotive fuel transfer pumps market is also influenced by the increasing age of the global vehicle fleet, which is driving demand for replacement components. As vehicles accumulate higher usage over time, the need for maintenance and replacement of essential fuel system parts continues to grow. Exposure to operational stress and prolonged usage contributes to increased wear, further strengthening aftermarket demand. This trend is particularly significant in regions with large vehicle populations, where long-term usage cycles support consistent demand for replacement fuel transfer pumps.

The electric segment accounted for 58% share in 2025 and is expected to grow at a CAGR of 7.1% from 2026 to 2035. This segment is gaining prominence as modern vehicles increasingly incorporate electronic fuel delivery systems that require precise flow control and consistent pressure. The automotive fuel transfer pumps market is benefiting from advancements in electric pump design, including improvements in durability, resistance to wear, and lightweight construction. These developments are supporting compliance with efficiency standards while enhancing overall vehicle performance.

The gasoline segment held a 45% share in 2025 and is projected to grow at a CAGR of 6.1% through 2035. This dominance is supported by the widespread presence of gasoline-powered vehicles, which continue to require reliable fuel delivery systems. The automotive fuel transfer pumps market is sustained by strong production volumes and ongoing replacement demand, ensuring continued growth across both OEM and aftermarket segments.

U.S. Automotive Fuel Transfer Pumps Market reached USD 4.3 billion in 2025. The automotive fuel transfer pumps market in the United States is expanding due to strong demand for vehicles equipped with durable fuel systems and high operational performance. The market is supported by a large vehicle base and extended usage cycles, which contribute to consistent replacement demand. Well-established service networks and a strong aftermarket ecosystem are further driving growth, as maintenance requirements for fuel system components continue to rise over time.

Key players operating in the Global Automotive Fuel Transfer Pumps Market include Robert Bosch, Denso, Continental Automotive, Delphi Technologies, Aisin Seiki, Mitsubishi Electric, TI Fluid Systems, Carter Fuel Systems, and Pierburg (Rheinmetall). Companies in the Global Automotive Fuel Transfer Pumps Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Many players are investing in advanced pump technologies to improve efficiency, durability, and performance under demanding conditions. Collaborations with automotive manufacturers are enabling better integration of fuel systems within modern vehicle architectures. Companies are also expanding production capacities to meet rising global demand while optimizing cost structures. In addition, a strong focus on aftermarket services and distribution networks is helping companies capture long-term revenue opportunities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Vehicle

- 2.2.4 Fuel

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing commercial vehicle and logistics fleet

- 3.2.1.3 Expansion of automotive aftermarket demand

- 3.2.1.4 Increasing fuel injection system adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid shift toward electric vehicles

- 3.2.2.2 Fuel price volatility affecting vehicle usage

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging automotive markets

- 3.2.3.2 Development of high-efficiency electric fuel pumps

- 3.2.3.3 Expansion of biofuel and alternative fuel vehicles

- 3.2.3.4 Increasing demand from off-road and industrial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 EPA Fuel System Regulations

- 3.4.1.2 CARB (California Air Resources Board) Standards

- 3.4.2 Europe

- 3.4.2.1 Euro 6 / Euro 7 Emission Standards

- 3.4.2.2 ECE R67 / R110 Fuel System Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China VI Emission Standards

- 3.4.3.2 Japan JIS Fuel System Standards / JARI Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil PROCONVE

- 3.4.4.2 ABNT NBR Fuel System Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE ESMA Fuel System & Emission Standards

- 3.4.5.2 South Africa SABS Fuel System Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by primary research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Mn, Million Units)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Electrical

Chapter 6 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Ethanol/Biofuels

- 6.5 LPG/CNG

- 6.6 Other Alternative Fuels

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Million Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two-wheelers

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 OEM (Original Equipment Manufacturer)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Aisin Seiki

- 10.1.2 Continental Automotive

- 10.1.3 Delphi Technologies

- 10.1.4 Denso

- 10.1.5 Hitachi Astemo

- 10.1.6 Magnetti Marelli

- 10.1.7 Mitsubishi Electric

- 10.1.8 Pierburg (Rheinmetall)

- 10.1.9 Robert Bosch

- 10.1.10 TI Fluid Systems

- 10.2 Regional players

- 10.2.1 Airtex Pumps

- 10.2.2 Carter Fuel Systems

- 10.2.3 GMB

- 10.2.4 Spectra Premium

- 10.2.5 Stanadyne

- 10.2.6 UFI Filters

- 10.2.7 Walbro

- 10.3 Emerging players

- 10.3.1 Cummins Fuel Systems

- 10.3.2 Edelbrock

- 10.3.3 Holley Performance Products

全球汽車幫浦市場:按類型、技術、容量、應用、車輛類型、電動車類型、非公路用車輛類型、銷售管道和地區分類-預測至2035年

全球汽車幫浦市場:按類型、技術、容量、應用、車輛類型、電動車類型、非公路用車輛類型、銷售管道和地區分類-預測至2035年 汽車幫浦市場:按泵浦類型、車輛型號、燃料類型和銷售管道分類-2026-2032年全球市場預測

汽車幫浦市場:按泵浦類型、車輛型號、燃料類型和銷售管道分類-2026-2032年全球市場預測 汽車幫浦市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝方式分類

汽車幫浦市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝方式分類 汽車溫度控管系統幫浦市場:機會、成長促進因素、產業趨勢分析及預測(2026-2035)

汽車溫度控管系統幫浦市場:機會、成長促進因素、產業趨勢分析及預測(2026-2035) 乘用車泵市場-全球產業規模、佔有率、趨勢、機會與預測:按泵類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車空調壓力調節器市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、車輛類型、需求類別、地區和競爭對手分類,2021-2031年

乘用車泵市場-全球產業規模、佔有率、趨勢、機會與預測:按泵類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車空調壓力調節器市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、車輛類型、需求類別、地區和競爭對手分類,2021-2031年 汽車幫浦市場:按泵浦類型、銷售管道、技術、車輛類型和地區分類。

汽車幫浦市場:按泵浦類型、銷售管道、技術、車輛類型和地區分類。 2026年全球汽車幫浦市場報告汽車燃油供應幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。汽車燃油輸送幫浦市場:按應用、幫浦類型、燃油類型、銷售管道和車輛類型分類-2026-2032年全球市場預測

2026年全球汽車幫浦市場報告汽車燃油供應幫浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。汽車燃油輸送幫浦市場:按應用、幫浦類型、燃油類型、銷售管道和車輛類型分類-2026-2032年全球市場預測