|

市場調查報告書

商品編碼

2019233

藥品泡殼包裝市場機會、成長要素、產業趨勢分析及2026-2035年預測。Pharmaceutical Blister Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

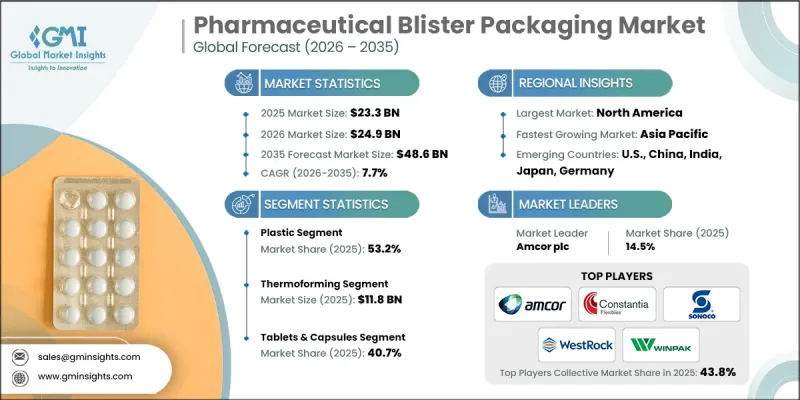

預計到 2025 年,全球藥品泡殼包裝市場價值將達到 233 億美元,年複合成長率為 7.7%,到 2035 年將達到 486 億美元。

市場成長主要受以下因素驅動:監管要求日益嚴格,強制要求使用防篡改和可追溯包裝;以及阻隔性材料在保護對水分和氧氣敏感的藥品方面的應用日益廣泛。已開發地區和新興地區的藥品產量不斷成長,這主要得益於慢性病患病率上升、人口老齡化以及醫療保健服務可及性的提高,從而進一步推動了市場需求。製藥公司擴大採用單劑量包裝,以提高患者用藥安全,同時遵守防偽法規,包括增強可追溯性和可靠的識別要求。這些趨勢正在加速整個製藥業對泡殼包裝解決方案的採用,從而提高產品保護、營運效率和供應鏈完整性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 233億美元 |

| 預測金額 | 486億美元 |

| 複合年成長率 | 7.7% |

預計到2025年,熱成型市場規模將達到118億美元,這主要得益於其能夠高效生產適用於片劑和膠囊的透明泡殼。熱成型技術具有可視性強、加工能力高以及與自動化包裝系統無縫整合等優點,因此在製藥生產設施中廣泛使用。

到2025年,藥品泡殼包裝市佔率將達到53.2%,反映出該領域對PVC和PET等塑膠的高度依賴。這些材料因其優異的成型性而備受青睞,能夠實現精確的腔體成型,從而容納片劑和膠囊。其卓越的透明度使內容物清晰可見,這對於品質控制和患者信任至關重要。此外,PVC和PET為大規模生產提供了經濟高效的解決方案,使製造商能夠在保持高產能的同時最大限度地降低材料成本。

預計到2025年,北美藥品泡殼包裝市佔率將達到34.7%。這一成長主要得益於大規模製藥製造地的普及、嚴格的監管標準以及醫院和零售藥局對單劑量包裝日益成長的需求。製藥公司和包裝供應商正投資於先進的自動化和永續的泡殼包裝解決方案,以提高營運效率、確保合規性並應對環境問題。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球藥品消費量增加

- 對單劑量給藥的病人安全包裝的需求日益成長

- 防篡改和可追溯性的監管要求

- 引進高速自動化包裝線

- 保護藥品中水分和氧氣屏障的必要性

- 產業潛在風險與挑戰

- 遵守嚴格規定的負擔

- 多層包裝回收困難

- 市場機遇

- 過渡到可回收的單一材料泡殼

- 智慧/序列化包裝創新

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依材料分類,2022-2035年

- 塑膠

- 鋁箔

- 紙

第6章 市場估計與預測:依技術分類,2022-2035年

- 冷成型

- 熱成型

- 熱封

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 片劑和膠囊

- 醫療設備

- 注射藥物

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Amcor plc

- Constantia Flexibles

- Sonoco Products Company

- WestRock Company

- Winpak Control Group

- 按地區分類的主要企業

- 北美洲

- AptarGroup, Inc.

- Rohrer Corporation

- Tekni-Plex, Inc.

- Dow

- 亞太地區

- ACG

- Caprihans India Limited

- Huhtamaki

- 歐洲

- Borealis AG

- Carcano Antonio SpA

- RENOLIT SE

- SUDPACK

- 北美洲

- 特殊玩家/干擾者

- Honeywell International Inc.

- Romaco Group

- Syensqo

- Tjoapack LLC

- VinylPlus

The Global Pharmaceutical Blister Packaging Market was valued at USD 23.3 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 48.6 billion in 2035.

Market growth is fueled by stringent regulatory mandates requiring tamper-evident and traceable packaging, coupled with heightened adoption of high-barrier materials to protect moisture- and oxygen-sensitive drugs. Expanding pharmaceutical production in developed and emerging regions, driven by the rising incidence of chronic diseases, aging populations, and enhanced healthcare access, is further boosting demand. Pharmaceutical manufacturers are increasingly leveraging unit-dose packaging to enhance patient safety while complying with anti-counterfeiting regulations, including enhanced traceability and secure identification requirements. These trends are accelerating the adoption of blister packaging solutions that improve product protection, operational efficiency, and supply chain integrity across the pharmaceutical sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.3 Billion |

| Forecast Value | $48.6 Billion |

| CAGR | 7.7% |

The thermoforming segment reached USD 11.8 billion in 2025, due to its efficiency in producing transparent blister cavities suitable for tablets and capsules. Thermoforming technology ensures visibility, high throughput, and seamless integration with automated packaging systems, supporting widespread adoption across pharmaceutical production facilities.

The pharmaceutical blister packaging segment accounted for 53.2% share in 2025, reflecting the widespread reliance on plastics such as PVC and PET. These materials are highly favored due to their excellent formability, allowing precise cavity shaping to hold tablets and capsules. Their superior clarity ensures that the contents are clearly visible, which is important for both quality inspection and patient assurance. PVC and PET also offer cost-effective solutions for large-scale production, enabling manufacturers to maintain high throughput while minimizing material expenses.

North America Pharmaceutical Blister Packaging Market accounted for 34.7% share in 2025. The region's growth is supported by its large pharmaceutical manufacturing base, strict regulatory standards, and increasing demand for unit-dose packaging in hospitals and retail pharmacies. Pharmaceutical companies and packaging suppliers are investing in advanced automation and sustainable blister packaging solutions to enhance operational efficiency, maintain regulatory compliance, and address environmental concerns.

Key players operating in the Global Pharmaceutical Blister Packaging Market include ACG, Amcor plc, AptarGroup, Inc., Borealis AG, Carcano Antonio S.p.A., Caprihans India Limited, Constantia Flexibles, Dow, Honeywell International Inc., Huhtamaki, RENOLIT SE, Rohrer Corporation, Romaco Group, Sonoco Products Company, SUDPACK, Syensqo, Tekni-Plex, Inc., Tjoapack LLC, VinylPlus, WestRock Company, and Winpak Control Group. Companies in the Global Pharmaceutical Blister Packaging Market are strengthening their presence through strategic innovation and operational enhancements. They are investing in R&D to develop high-barrier, eco-friendly, and sustainable materials that meet evolving regulatory requirements and consumer expectations. Collaborations with pharmaceutical manufacturers and technology providers enable tailored packaging solutions and seamless integration into automated production lines. Expansion into emerging markets and regional manufacturing facilities ensures improved supply chain access and cost efficiency. Additionally, players focus on process automation, digital tracking, and serialization technologies to enhance product security, optimize operational throughput, and maintain competitive advantage in the global pharmaceutical packaging landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Technology trends

- 2.2.3 End-use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global pharmaceutical consumption rates

- 3.2.1.2 Increasing demand for unit-dose patient safety packaging

- 3.2.1.3 Regulatory mandates for tamper-evidence and traceability

- 3.2.1.4 Adoption of high-speed automated packaging lines

- 3.2.1.5 Need for moisture/oxygen barrier protection for drugs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rigid regulatory compliance burden

- 3.2.2.2 Difficult recyclability of multilayer packs

- 3.2.3 Market opportunities

- 3.2.3.1 Shift to recyclable mono-material blisters

- 3.2.3.2 Smart/serialized packaging innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Aluminum Foil

- 5.4 Paper

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cold Forming

- 6.3 Thermoforming

- 6.4 Heat Seal

Chapter 7 Market Estimates and Forecast, By End-Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Tablets & Capsules

- 7.3 Medical Devices

- 7.4 Injectables

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor plc

- 9.1.2 Constantia Flexibles

- 9.1.3 Sonoco Products Company

- 9.1.4 WestRock Company

- 9.1.5 Winpak Control Group

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 AptarGroup, Inc.

- 9.2.1.2 Rohrer Corporation

- 9.2.1.3 Tekni-Plex, Inc.

- 9.2.1.4 Dow

- 9.2.2 Asia Pacific

- 9.2.2.1 ACG

- 9.2.2.2 Caprihans India Limited

- 9.2.2.3 Huhtamaki

- 9.2.3 Europe

- 9.2.3.1 Borealis AG

- 9.2.3.2 Carcano Antonio S.p.A.

- 9.2.3.3 RENOLIT SE

- 9.2.3.4 SUDPACK

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Honeywell International Inc.

- 9.3.2 Romaco Group

- 9.3.3 Syensqo

- 9.3.4 Tjoapack LLC

- 9.3.5 VinylPlus

藥品泡殼包裝市場:預測(至2034年)-按材料、產品類型、技術、劑型、應用類型、最終用戶和地區分類的全球分析

藥品泡殼包裝市場:預測(至2034年)-按材料、產品類型、技術、劑型、應用類型、最終用戶和地區分類的全球分析 醫用泡殼包裝市場規模、佔有率和趨勢分析報告:按材料、技術、類型、應用、地區和細分市場分類(2026-2033 年)

醫用泡殼包裝市場規模、佔有率和趨勢分析報告:按材料、技術、類型、應用、地區和細分市場分類(2026-2033 年) 全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球藥品泡殼包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測

藥品泡殼包裝市場規模、佔有率、成長分析(按產品類型、技術類型、材料類型、應用和地區分類)-2026-2033年產業預測泡罩包裝藥品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024年至2032年的預測 全球醫療保健泡殼包裝市場

全球醫療保健泡殼包裝市場 醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年

醫藥泡殼包裝市場規模、佔有率、成長分析(按類型、按材料、按最終用途、按技術和按地區)- 行業預測,2025 年至 2032 年 藥品泡殼包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

藥品泡殼包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030) 全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030

全球藥品泡殼包裝市場:按材料、技術、產品、應用、最終用戶、地區 - 趨勢分析、競爭格局、預測,2019-2030 醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年

醫療保健泡殼包裝市場:成長、未來前景、競爭分析,2024-2032年