|

市場調查報告書

商品編碼

2019217

工業鼠李醣脂市場機會、成長要素、產業趨勢分析及2026-2035年預測Industrial Rhamnolipid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

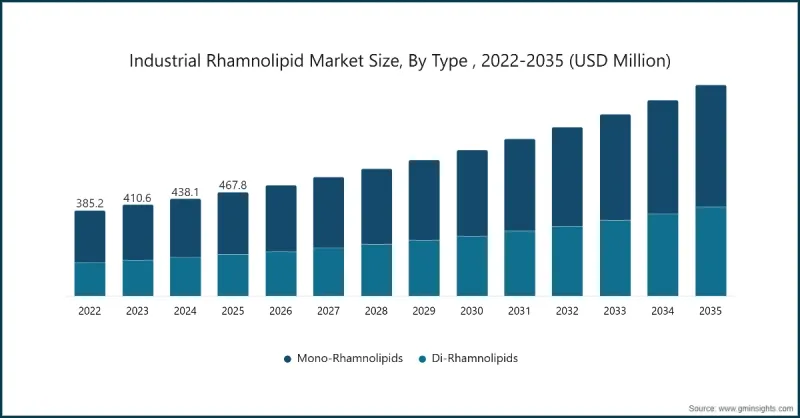

預計到 2025 年,全球工業鼠李醣脂市場價值將達到 4.678 億美元,年複合成長率為 8.4%,預計到 2035 年將達到 9.505 億美元。

工業鼠李醣脂最初是作為一種小眾的生物基界面活性劑出現,如今已發展成為多個工業領域不可或缺的成分。其功能性應用已擴展至提高製程效率、增強材料相容性以及確保能源生產、工業清洗、農業和環境修復等領域的運作可靠性。工業採購越來越傾向於選擇可再生、低毒性、環境永續且性能優異的原料。生物技術、發酵控制、菌株最佳化和後處理技術的進步提升了鼠李醣脂的性能,使其符合業界標準。其與配方的相容性、生物分解性和低環境持久性加速了其應用,尤其是在法規和永續性要求嚴格的地區,推動了成熟市場和新興市場的穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4.678億美元 |

| 預測金額 | 9.505億美元 |

| 複合年成長率 | 8.4% |

單層脂質佔60.4%的市場佔有率,預計到2035年將以7.8%的複合年成長率成長。其廣泛應用歸功於其優異的界面活性劑性能、溶解性和與配方的相容性。由於單層脂質具有降低表面張力的成本效益,因此廣泛應用於清潔、油田化學和環境修復等領域。儘管雙層脂質市場規模較小,但由於其卓越的乳化性能、在嚴苛條件下的穩定性以及長期的功能耐久性,正日益受到關注。

預計到2025年,液態製劑市佔率將達到70.6%,並在2026年至2035年間以8.1%的複合年成長率成長。液態鼠李醣脂因其易於操作、即時溶解以及能夠無縫整合到油田作業、工業清洗和環境處理等工藝流程中,而備受大規模工業應用的青睞。此外,其適用於連續加工、精確計量和靈活的配方開發等特性,也進一步提升了其在工業領域的普及度。

預計到2025年,北美工業鼠李醣脂市場將佔據28.4%的市場佔有率,在能源生產、工業清洗和環境保護等領域生物基界面活性劑的應用中發揮策略性作用。有利的市場環境、先進的工業基礎設施以及對永續解決方案的高接受度,正使該地區成為重要的成長中心。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 在石油和天然氣產業中擴大用於提高石油採收率(EOR)的應用

- 在化妝品和個人護理行業中不斷擴展的應用

- 對環保型和可生物分解界面活性劑的需求日益成長

- 產業潛在風險與挑戰

- 高昂的生產成本

- 鼠李醣脂生產所需原料供不應求

- 市場機遇

- 在生物修復和環境領域的應用

- 藥物和藥物傳輸系統的開發

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 單醣脂

- 迪拉姆諾脂

第6章 市場估計與預測:依類型分類,2022-2035年

- 液體

- 即用型

- 濃縮型

- 水懸浮液

- 粉末

- 噴霧乾燥

- 冷凍乾燥

- 大宗工業用途

第7章 市場估計與預測:依等級分類,2022-2035年

- 技術級(85-90%)

- 高純度等級(90-95%)

- 超高純度等級(95%以上)

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 石油和天然氣

- 農業

- 製藥和醫療保健

- 化妝品和個人護理

- 其他(紡織品、家用和工業清潔劑等)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Evonik Industries AG

- Stepan Company

- AGAE Technologies LLC

- Jeneil Biotech Inc

- Biotensidon GmbH

- GlycoSurf

- TensioGreen

- Zhejiang Silver Elephant Bio-engineering Co. Ltd

- Shaanxi Deguan Biotechnology Co. Ltd

- Holiferm Ltd

- CD BioGlyco

The Global Industrial Rhamnolipid Market was valued at USD 467.8 million in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 950.5 million by 2035.

Industrial rhamnolipids initially emerged as niche bio-based surfactants but have evolved into critical components across multiple industrial sectors. Their functional applications now extend to improving process efficiency, enhancing material compatibility, and ensuring operational reliability in areas such as energy production, industrial cleaning, agriculture, and environmental remediation. Industrial procurement is increasingly favoring inputs that deliver high performance while being renewable, minimally toxic, and environmentally sustainable. Advancements in biotechnology, fermentation control, strain optimization, and downstream processing have elevated rhamnolipid performance to meet industrial standards. The combination of formulation compatibility, biodegradability, and low environmental persistence has accelerated adoption, particularly in regions with stringent regulatory oversight and sustainability mandates, driving steady growth in both established and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $467.8 Million |

| Forecast Value | $950.5 Million |

| CAGR | 8.4% |

The mono-rhamnolipids segment held a 60.4% share and is expected to grow at a CAGR of 7.8% through 2035. Their widespread use is attributed to superior surface activity, solubility, and formulation compatibility. Industries leverage mono-rhamnolipids for applications including cleaning, oilfield chemistry, and environmental remediation due to their cost-effective performance in reducing interfacial tension. Di-rhamnolipids, though smaller in market size, are gaining traction for their superior emulsification properties, stability under extreme conditions, and long-term functional durability.

The liquid formulations segment held a 70.6% share in 2025 and is projected to grow at a CAGR of 8.1% from 2026 to 2035. Liquid rhamnolipids are preferred for large-scale industrial applications due to ease of handling, immediate solubility, and seamless integration into processes like oilfield operations, industrial cleaning, and environmental treatment. Their suitability for continuous processing, accurate dosing, and flexible formulation development reinforces their industrial popularity.

North America Industrial Rhamnolipid Market held a 28.4% share in 2025, driven by its strategic role in deploying bio-based surfactants across energy production, industrial cleaning, and environmental protection sectors. Favorable market conditions, advanced industrial infrastructure, and high adoption of sustainable solutions make the region a key growth hub.

Leading players in the Global Industrial Rhamnolipid Market include TensioGreen, GlycoSurf, Evonik Industries AG, Shaanxi Deguan Biotechnology Co. Ltd, Stepan Company, Holiferm Ltd, Biotensidon GmbH, CD BioGlyco, Zhejiang Silver Elephant Bioengineering Co. Ltd, Jeneil Biotech Inc, and AGAE Technologies LLC. Key strategies adopted by companies to strengthen their market presence include investing heavily in R&D to enhance rhamnolipid yield, purity, and functionality. Firms are optimizing fermentation and downstream processing for scalable, cost-effective production. Strategic partnerships with industrial users in energy, agriculture, and environmental remediation are expanding adoption. Companies are focusing on regulatory compliance, sustainable production practices, and eco-label certifications to differentiate their products. Expanding regional manufacturing capabilities and distribution networks ensures faster delivery and localized support. Additionally, marketing initiatives highlighting biodegradability, performance efficiency, and multi-sector versatility help build brand credibility and capture emerging market opportunities worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Grade

- 2.2.5 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising use in enhanced oil recovery (EOR) in the oil & gas industry

- 3.2.1.2 Growing applications in cosmetics and personal care industries

- 3.2.1.3 Rising demand for eco friendly & biodegradable surfactants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production cost

- 3.2.2.2 Limited availability of raw materials for rhamnolipid production

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in bioremediation & environmental applications

- 3.2.3.2 Pharmaceutical & drug delivery system development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Mono-Rhamnolipids

- 5.3 Di-Rhamnolipids

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid

- 6.2.1 Ready to Use

- 6.2.2 Concentrated

- 6.2.3 Aqueous Suspensions

- 6.3 Powder

- 6.3.1 Spray Dried

- 6.3.2 Freeze Dried

- 6.3.3 Bulk Industrial

Chapter 7 Market Estimates and Forecast, By Grade, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Technical Grade (85-90%)

- 7.3 High Purity Grade (90-95%)

- 7.4 Ultra-High Purity Grade (>95%)

Chapter 8 Market Estimates and Forecast, By End-User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Oil & Gas

- 8.3 Agriculture

- 8.4 Pharmaceuticals & Healthcare

- 8.5 Cosmetics & Personal Care

- 8.6 Others (Textiles, Household & Industrial Cleaners, etc)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Evonik Industries AG

- 10.2 Stepan Company

- 10.3 AGAE Technologies LLC

- 10.4 Jeneil Biotech Inc

- 10.5 Biotensidon GmbH

- 10.6 GlycoSurf

- 10.7 TensioGreen

- 10.8 Zhejiang Silver Elephant Bio-engineering Co. Ltd

- 10.9 Shaanxi Deguan Biotechnology Co. Ltd

- 10.10 Holiferm Ltd

- 10.11 CD BioGlyco

工業酵素市場:按類型、原料、配方、供應形式、等級、應用和分銷管道分類-2026-2032年全球市場預測

工業酵素市場:按類型、原料、配方、供應形式、等級、應用和分銷管道分類-2026-2032年全球市場預測 全球工業酵素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球工業酵素市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球工業酵素市場報告

2026年全球工業酵素市場報告 工業酵素市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場預測(2026-2033 年)

工業酵素市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場預測(2026-2033 年) 全球工業酵素市場,2026-2030年工業聚乙烯亞胺市場依形態、分子量、反應等級及應用分類-2026-2032年全球預測

全球工業酵素市場,2026-2030年工業聚乙烯亞胺市場依形態、分子量、反應等級及應用分類-2026-2032年全球預測 工業生物樹脂市場預測至2032年:按樹脂類型、原料、形態、加工方法、應用、最終用戶和地區分類的全球分析

工業生物樹脂市場預測至2032年:按樹脂類型、原料、形態、加工方法、應用、最終用戶和地區分類的全球分析 日本工業酵素市場報告(按產品、來源、應用和地區分類,2026-2034年)

日本工業酵素市場報告(按產品、來源、應用和地區分類,2026-2034年) 工業酵素市場規模、佔有率和成長分析(按酵素類型、配方、來源、應用和地區分類)-2026-2033年產業預測

工業酵素市場規模、佔有率和成長分析(按酵素類型、配方、來源、應用和地區分類)-2026-2033年產業預測 產業用酵素的全球市場(2026年~2036年)

產業用酵素的全球市場(2026年~2036年)