|

市場調查報告書

商品編碼

2019210

工業乾燥機市場機會、成長要素、產業趨勢分析及2026-2035年預測Industrial Dryers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

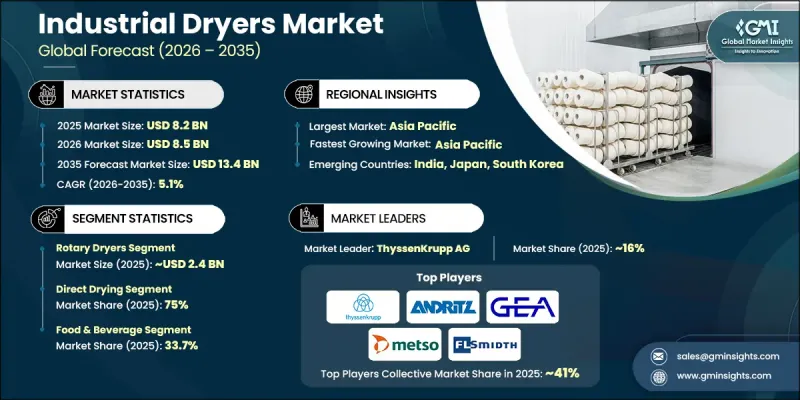

預計到 2025 年,全球工業乾燥機市場價值將達到 82 億美元,並預計以 5.1% 的複合年成長率成長,到 2035 年達到 134 億美元。

包裝食品和加工食品產量的增加推動了市場成長。製造商越來越需要先進的乾燥系統來去除水分、保持產品品質並延長保存期限。工業乾燥機對於零嘴零食、奶粉和速食食品至關重要,它能夠保持產品整體水分含量的一致性、保留質地並穩定原料。食品加工商和製造商正在投資節能可靠的乾燥解決方案,這些方案能夠處理大量、連續生產,同時確保衛生和穩定的產量。隨著對包裝食品和加工食品需求的成長,對能夠最佳化效率、最大限度減少停機時間並提供穩定結果的去除水分技術的需求也隨之增加。製造商優先考慮能夠維持產品安全標準並簡化操作的系統,這推動了全球最新工業乾燥機的應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 82億美元 |

| 預測金額 | 134億美元 |

| 複合年成長率 | 5.1% |

預計到2025年,迴轉式乾燥機市場規模將達到24億美元,並在2035年之前以6%的複合年成長率成長。迴轉式乾燥機憑藉其多功能性、高效性以及在食品、化學、礦物和生質能等眾多行業中處理散裝和顆粒狀物料的能力,在市場上佔據領先地位。旋轉滾筒結構與可控熱風或熱氣的結合,確保了均勻乾燥,即使在嚴苛的工業環境中也能實現連續運作和大量處理。迴轉式乾燥機的可靠性和穩健性能使其成為大規模生產的理想選擇。

預計到2025年,直接乾燥技術將佔據75%的市場佔有率,並在2035年之前以5%的複合年成長率成長。其簡便性、運作效率和成本效益正推動其在眾多產業中廣泛應用。直接乾燥機透過熱空氣或熱氣直接接觸物料,以快速且有效率地去除水分。與間接乾燥系統相比,直接乾燥機因其能耗更低、操作更簡便、設備更簡單而備受青睞,這些優勢鞏固了其強大的市場地位。

預計到2025年,中國工業乾燥機市場規模將達到10.3億美元,並在2035年之前以6.3%的複合年成長率成長。該市場成長的主要驅動力是化學、食品加工、製藥和紡織業的擴張。大型製造工廠對高效乾燥解決方案的強勁需求推動了旋轉式、流化床式、噴霧式和真空式乾燥機的應用。中國製造商正著力打造節能高效的乾燥機,以降低營運成本並維持產品品質的穩定性。精確的溫度控制、自動監控和先進的去除水分等創新正在提高生產效率並減少物料浪費,尤其是在對品質要求極高的製藥行業。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 食品加工和包裝食品生產的擴張

- 擴大製藥和化工製造活動

- 乾燥系統和製程自動化方面的技術進步

- 陷阱與挑戰

- 工業乾燥過程能耗高

- 先進的乾燥設備需要大量的資金投入。

- 機會

- 對節能和熱回收乾燥技術的需求日益成長

- 數位監控系統與自動化過程控制系統的整合

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 影響價格波動的區域因素

- 按最終用途行業分類的價格敏感度

- 總擁有成本分析

- 貿易數據分析(基於付費資料庫)

- 進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易路線及關稅的影響(基於付費資料庫)

- 按烘乾機類型貿易流量

- 區域進口依存度分析

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商裝置容量(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 旋轉式乾燥機

- 流體化床乾燥器

- 噴霧乾燥器

- 滾筒式烘乾機

- 冷凍乾燥機

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 直接乾燥

- 間接乾燥

第7章 市場估計與預測:依最終用途產業分類,2022-2035年

- 食品/飲料

- 化學

- 製藥

- 紙漿和紙漿

- 纖維

- 建造

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Akona Process Solutions

- ANDRITZ AG

- ANIVI Ingenieria SA

- Buhler Holding AG

- Carrier Vibrating Equipment, Inc.

- Durr CTS Inc.

- FLSmidth & Co. A/S

- GEA Group

- Lanly Company

- METSO

- Mitchell Dryers

- SPX Flow

- Ventilex BV

- Wuxi Modern Spray Drying Equipment Co., Ltd.

- YAMATO SANKO MFG. CO. LTD.

The Global Industrial Dryers Market was valued at USD 8.2 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 13.4 billion by 2035.

Growth in the market is being fueled by the rising production of packaged and processed foods, as manufacturers increasingly require advanced drying systems to remove moisture, preserve product quality, and extend shelf life. Industrial dryers are critical for ensuring consistent moisture content across products, maintaining texture, and stabilizing ingredients in snack foods, dairy powders, and instant food items. Food processors and manufacturers are investing in energy-efficient, reliable drying solutions that can handle high-volume continuous production while ensuring sanitation and uniform output. The rising demand for packaged and processed foods is creating a parallel need for moisture removal technologies that optimize efficiency, minimize downtime, and deliver consistent results. Manufacturers prioritize systems that maintain product safety standards and streamline operations, driving the adoption of modern industrial dryers globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.2 Billion |

| Forecast Value | $13.4 Billion |

| CAGR | 5.1% |

The rotary dryers segment generated USD 2.4 billion in 2025 and is expected to grow at a CAGR of 6% through 2035. Rotary dryers lead the market due to their versatility, efficiency, and ability to process bulk and granular materials across sectors, including food, chemicals, minerals, and biomass. Their rotating drum design, combined with controlled hot air or gas, ensures uniform drying, enabling continuous operation and high-volume capacity under harsh industrial conditions. The reliability and robust performance of rotary dryers make them a preferred choice for large-scale operations.

The direct drying technology segment held a 75% share in 2025 and is projected to grow at a CAGR of 5% through 2035. Its simplicity, operational efficiency, and cost-effectiveness drive its adoption across multiple industries. Direct dryers use hot air or gas in direct contact with materials, enabling rapid moisture removal with high thermal efficiency. They are favored for lower energy consumption, ease of operation, and reduced equipment complexity compared to indirect drying systems, supporting their strong market presence.

China Industrial Dryers Market captured USD 1.03 billion in 2025 and is expected to grow at a CAGR of 6.3% through 2035. The market is driven by expanding chemical, food processing, pharmaceutical, and textile industries. High demand for efficient drying solutions in large-scale manufacturing facilities is boosting the adoption of rotary, fluidized bed, spray, and vacuum dryers. Chinese manufacturers emphasize energy-efficient, high-capacity designs to lower operational costs and maintain consistent product quality. Technological innovations, including precise temperature controls, automated monitoring, and advanced moisture removal, enhance productivity and reduce material waste, particularly in the sensitive pharmaceutical sector.

Key players in the Global Industrial Dryers Market include ANDRITZ AG, Akona Process Solutions, ANIVI Ingenieria SA, Buhler Holding AG, Carrier Vibrating Equipment, Inc., Durr CTS Inc., FLSmidth & Co. A/S, GEA Group, Lanly Company, METSO, Mitchell Dryers, SPX Flow, Ventilex B.V., Wuxi Modern Spray Drying Equipment Co., Ltd., and YAMATO SANKO MFG. CO. LTD. Companies in the Global Industrial Dryers Market are strengthening their foothold by investing in energy-efficient and high-capacity drying technologies that minimize operational costs while maximizing throughput. They focus on developing automation-enabled and smart monitoring systems for precise moisture control, improving reliability and process consistency. Strategic partnerships with food, pharmaceutical, and chemical manufacturers expand market reach, while after-sales services and maintenance support enhance customer retention. Manufacturers are also prioritizing R&D to introduce flexible, modular, and scalable solutions that address diverse industry requirements, improving competitiveness and fostering long-term growth across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of food processing and packaged food production

- 3.2.1.2 Growing pharmaceutical and chemical manufacturing activities

- 3.2.1.3 Technological advancements in drying systems and process automation

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High energy consumption associated with industrial drying operations

- 3.2.2.2 High capital investment required for advanced drying equipment

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for energy-efficient and heat recovery drying technologies

- 3.2.3.2 Integration of digital monitoring and automated process control systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variation factors

- 3.9.4 Price sensitivity by end-use industry

- 3.9.5 Total cost of ownership analysis

- 3.10 Trade data analysis (driven by paid data base)

- 3.10.1 Import/export volume & value trends (driven by paid data base)

- 3.10.2 Key trade corridors & tariff impact (driven by paid data base)

- 3.10.3 Trade flow by dryer type

- 3.10.4 Regional import dependency analysis

- 3.11 Capacity & production landscape (driven by primary research)

- 3.11.1 Installed capacity by region & key producer (driven by primary research)

- 3.11.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Rotary Dryers

- 5.3 Fluidized Bed Dryers

- 5.4 Spray Dryers

- 5.5 Drum Dryers

- 5.6 Freeze Dryers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct Drying

- 6.3 Indirect Drying

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food & Beverage

- 7.3 Chemical

- 7.4 Pharmaceutical

- 7.5 Paper & Pulp

- 7.6 Textile

- 7.7 Construction

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Akona Process Solutions

- 10.2 ANDRITZ AG

- 10.3 ANIVI Ingenieria SA

- 10.4 Buhler Holding AG

- 10.5 Carrier Vibrating Equipment, Inc.

- 10.6 Durr CTS Inc.

- 10.7 FLSmidth & Co. A/S

- 10.8 GEA Group

- 10.9 Lanly Company

- 10.10 METSO

- 10.11 Mitchell Dryers

- 10.12 SPX Flow

- 10.13 Ventilex B.V.

- 10.14 Wuxi Modern Spray Drying Equipment Co., Ltd.

- 10.15 YAMATO SANKO MFG. CO. LTD.

滾筒式乾衣機市場機會、成長要素、產業趨勢分析及2026-2035年預測。

滾筒式乾衣機市場機會、成長要素、產業趨勢分析及2026-2035年預測。 工業乾燥機市場:按類型、能源來源、材料、傳熱方式及最終用途產業分類-2026-2032年全球市場預測

工業乾燥機市場:按類型、能源來源、材料、傳熱方式及最終用途產業分類-2026-2032年全球市場預測 歐洲滾筒式乾衣機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲滾筒式乾衣機:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 全球電動滾筒烘乾機市場亞太地區滾筒烘乾機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)英國滾筒烘乾機:市場佔有率分析、產業趨勢、統計與成長預測(2025-2030)電動式滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

全球電動滾筒烘乾機市場亞太地區滾筒烘乾機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)英國滾筒烘乾機:市場佔有率分析、產業趨勢、統計與成長預測(2025-2030)電動式滾筒烘乾機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 工業乾燥機市場:2024-2033年全球產業分析、規模、佔有率、成長、趨勢、預測

工業乾燥機市場:2024-2033年全球產業分析、規模、佔有率、成長、趨勢、預測 2024-2028年農產品工業乾燥機的全球市場

2024-2028年農產品工業乾燥機的全球市場