|

市場調查報告書

商品編碼

2019127

表面處理市場機會、成長要素、產業趨勢分析及2026-2035年預測。Surface Treatments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

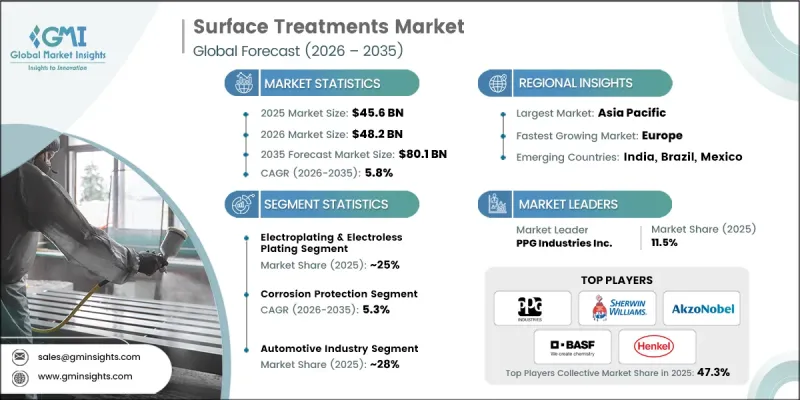

2025年全球表面處理市場規模預估為456億美元,預計2035年將以5.8%的複合年成長率成長至801億美元。

表面處理旨在改善金屬、聚合物和複合材料的功能和美觀特性,帶來許多好處,例如提高耐腐蝕性、耐磨性、附著力和外觀。這些技術能夠延長零件的使用壽命,即使在嚴苛的環境條件下也能保持可靠的效能。現代應用包括等離子處理、雷射紋理化和奈米塗層等先進工藝,以及塗層、密封劑和疏水層等,從而實現高度客製化和高性能。在航太、電子和汽車等高精度領域,對錶面處理的需求尤其旺盛,因為即使是微小的表面變化也會影響其功能。永續性也日益受到重視,水性、生物基和環保處理方法正逐漸成為建築、汽車和工業應用領域的標準做法。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 456億美元 |

| 預測金額 | 801億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,防腐蝕領域將佔據30%的市場佔有率,並在2035年之前以5.3%的複合年成長率成長。該領域的表面處理,例如塗層、電鍍和轉化膜,對於暴露於惡劣環境的汽車、船舶和工業應用至關重要。這些處理可以降低維護成本,同時延長零件的使用壽命。耐磨性同樣重要,尤其是在航太、國防和工業機械應用中,摩擦、機械應力和高速運轉需求表面具有極高的耐久性。這些處理可以確保運作可靠性和長期性能。

預計到2025年,汽車產業將佔據28%的市場佔有率,並預計在2035年以5.9%的複合年成長率成長。在汽車應用中,防腐蝕、耐磨和外觀提升至關重要。表面處理有助於延長車輛壽命,支援輕量化材料以提高能源效率,並增強美觀性。航太和國防領域也存在類似的需求,這些領域需要高性能塗層來承受極端溫度、摩擦和環境壓力。在這些高要求應用中常用的技術包括熱噴塗、物理氣相沉積(PVD)和雷射表面處理。

預計到2025年,北美表面處理市場佔有率將達到22%,這主要得益於行業的成熟、創新以及對永續解決方案日益成長的需求。美國在該地區處於領先地位,這得益於其先進的製造技術、高性能材料的廣泛應用以及強大的國內外表面處理服務商網路。大量的研發工作集中在航太、汽車、電子和醫療等領域,在這些領域,表面處理能夠提升產品的耐久性、耐腐蝕性和特殊功能。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對耐腐蝕性和耐磨性的需求

- 各方呼籲採取永續性和環保的解決方案

- 表面工程技術的進步

- 產業潛在風險與挑戰

- 先進表面技術高成本

- 環境和監管合規方面的挑戰

- 市場機遇

- 對輕量高性能材料的需求日益成長

- 新興市場的崛起與基礎建設發展

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依技術類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依技術分類,2022-2035年

- 電鍍和無電電鍍

- 陽極處理和化學轉化塗層

- 熱噴塗技術

- 物理氣相沉積(PVD)

- 化學氣相沉積(CVD)

- 等離子表面處理

- 雷射表面處理

- 新興技術

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 防腐蝕

- 提高耐磨性

- 裝飾性和美觀性飾面

- 電氣和電子特性

- 生物相容性和醫療應用

- 溫度控管

- 光學性能的改善

第7章 市場估計與預測:依最終用戶分類,2022-2035年

- 汽車產業

- 航太/國防

- 電子和半導體

- 工業機械和設備

- 醫療設備和醫療保健

- 能源和發電

- 建築/建築設計

- 船舶/海洋

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- PPG Industries Inc.

- The Sherwin-Williams Company

- AkzoNobel NV

- BASF SE(Surface Technologies Division)

- Henkel AG & Co. KGaA

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

The Global Surface Treatments Market was valued at USD 45.6 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 80.1 billion by 2035.

Surface treatments are designed to improve the functional and aesthetic properties of metals, polymers, and composites, offering benefits such as corrosion resistance, wear protection, adhesion, and enhanced appearance. These technologies extend component lifespans and maintain reliable performance under harsh environmental conditions. Modern applications include coatings, sealants, hydrophobic layers, and advanced processes such as plasma treatments, laser texturing, and nanocoatings, which provide high customization and performance. Demand is particularly strong in high-precision sectors such as aerospace, electronics, and automotive, where even minor surface variations can impact functionality. Sustainability is increasingly influencing adoption, with water-based, bio-sourced, and eco-friendly treatments becoming standard practice in construction, automotive, and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.6 Billion |

| Forecast Value | $80.1 Billion |

| CAGR | 5.8% |

The corrosion protection segment held a 30% share in 2025 and is projected to grow at a CAGR of 5.3% through 2035. Surface treatments in this segment, including coatings, plating, and conversion layers, are essential for automotive, marine, and industrial applications exposed to aggressive conditions. These treatments reduce maintenance costs while extending component lifetimes. Wear resistance is equally critical, particularly for aerospace, defense, and industrial machinery applications, where friction, mechanical stress, and high-speed operations demand durable surfaces. These treatments ensure operational reliability and long-term performance.

The automotive segment held a 28% share in 2025 and is expected to grow at a CAGR of 5.9% by 2035. Automotive applications rely heavily on corrosion protection, wear resistance, and aesthetic enhancements. Surface treatments help extend vehicle lifespan, support lightweight materials for energy efficiency, and improve visual appeal. Similar demands exist in aerospace and defense, where high-performance coatings must withstand extreme temperatures, friction, and environmental stress. Technologies commonly applied in such demanding applications include thermal spray, physical vapor deposition (PVD), and laser surface engineering.

North America Surface Treatments Market accounted for 22% share in 2025, driven by industrial maturity, innovation, and a growing emphasis on sustainable solutions. The U.S. leads the region, supported by advanced manufacturing, widespread use of high-performance materials, and a strong network of national and global surface treatment providers. Extensive research and development initiatives focus on aerospace, automotive, electronics, and healthcare applications, where surface treatments enhance durability, corrosion resistance, and specialized functionality.

Key players operating in the Global Surface Treatments Market include PPG Industries Inc., The Sherwin-Williams Company, AkzoNobel N.V., BASF SE (Surface Technologies Division), Henkel AG & Co. KGaA, Axalta Coating Systems Ltd., RPM International Inc., Jotun A/S, Kansai Paint Co., Ltd., and Nippon Paint Holdings Co., Ltd. Companies in the Surface Treatments Market are strengthening their presence through continuous innovation, strategic partnerships, and geographic expansion. They are investing in research and development to develop high-performance, eco-friendly coatings and advanced surface technologies. Product diversification allows firms to address industry-specific requirements across automotive, aerospace, electronics, and construction sectors. Businesses are also enhancing service capabilities, offering tailored solutions, maintenance support, and technical consulting to build long-term client relationships. Strategic collaborations with material suppliers and technology providers improve market reach and accelerate the adoption of advanced solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for corrosion and wear resistance

- 3.2.1.2 Pressure for sustainability and eco-friendly solutions

- 3.2.1.3 Advancements in surface engineering technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced surface technologies

- 3.2.2.2 Environmental and regulatory compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for lightweight and high-performance materials

- 3.2.3.2 Rise of emerging markets and infrastructure developments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Electroplating and electroless plating

- 5.3 Anodizing and chemical conversion coatings

- 5.4 Thermal spraying technologies

- 5.5 Physical vapor deposition (PVD)

- 5.6 Chemical vapor deposition (CVD)

- 5.7 Plasma surface treatment

- 5.8 Laser surface engineering

- 5.9 Emerging technologies

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Corrosion protection

- 6.3 Wear resistance enhancement

- 6.4 Decorative and aesthetic finishes

- 6.5 Electrical and electronic properties

- 6.6 Biocompatibility and medical applications

- 6.7 Thermal management

- 6.8 Optical properties enhancement

Chapter 7 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive industry

- 7.3 Aerospace and defense

- 7.4 Electronics and semiconductors

- 7.5 Industrial machinery and equipment

- 7.6 Medical devices and healthcare

- 7.7 Energy and power generation

- 7.8 Construction and architecture

- 7.9 Marine and offshore

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 PPG Industries Inc.

- 9.2 The Sherwin-Williams Company

- 9.3 AkzoNobel N.V.

- 9.4 BASF SE (Surface Technologies Division)

- 9.5 Henkel AG & Co. KGaA

- 9.6 Axalta Coating Systems Ltd.

- 9.7 RPM International Inc.

- 9.8 Jotun A/S

- 9.9 Kansai Paint Co., Ltd.

- 9.10 Nippon Paint Holdings Co., Ltd.

混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測

混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測 2026年全球混凝土表面加固劑市場報告化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年

2026年全球混凝土表面加固劑市場報告化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年 表面處理化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

表面處理化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球交通運輸路面材料市場規模、佔有率、趨勢和成長分析報告全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034)

2026-2034年全球交通運輸路面材料市場規模、佔有率、趨勢和成長分析報告全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034) 全球工業低摩擦表面材料市場:預測(至2034年)-按材料類型、塗層技術、功能、應用、最終用戶和地區進行分析2026年全球化學表面處理市場報告2026年全球成品生產線市場報告

全球工業低摩擦表面材料市場:預測(至2034年)-按材料類型、塗層技術、功能、應用、最終用戶和地區進行分析2026年全球化學表面處理市場報告2026年全球成品生產線市場報告