|

市場調查報告書

商品編碼

1934850

表面處理化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Surface Treatment Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

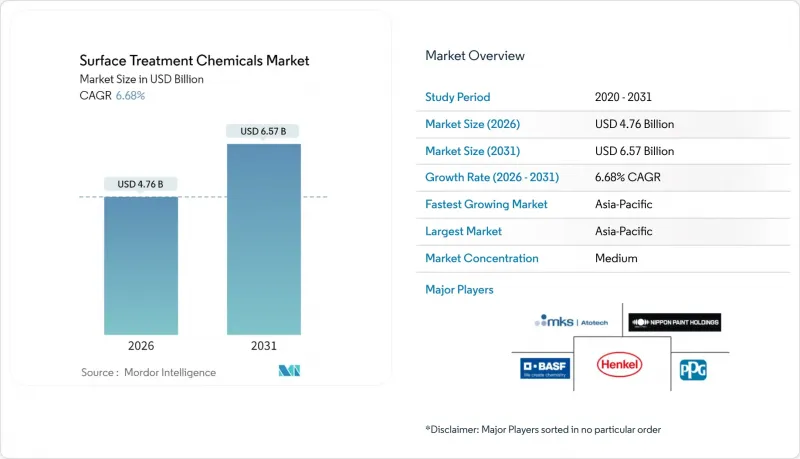

預計到 2026 年,表面處理化學品市場規模將達到 47.6 億美元,高於 2025 年的 44.6 億美元。

預計到 2031 年將達到 65.7 億美元,2026 年至 2031 年的複合年成長率為 6.68%。

汽車電氣化、半導體封裝回收以及需要耐腐蝕系統的離岸風力發電電專案正在推動強勁的成長勢頭。儘管亞洲製造地佔據了新增產能的大部分,但北美生產回收計畫和歐洲永續性法規正在引導高階需求轉向高性能、無鉻配方。隨著傳統金屬表面處理化學品的重要性下降,那些能夠將半導體級純度、多金屬相容性和生物基創新相結合的供應商正在佔據不斷擴大的價值市場。由於對六價鉻的限制日益嚴格,表面處理化學品市場正受益於監管趨同,這迫使終端用戶採用符合嚴格職業健康和環境標準的替代塗料和清潔劑。

全球表面處理化學品市場趨勢與洞察

亞洲汽車製造業快速擴張

亞洲汽車製造商正在擴展多材料車身結構,這些結構依賴能夠防止鋁和鋼之間交叉污染的清潔劑。電動車電池外殼、結構鑄件和溫度控管板需要精密蝕刻和轉化塗層,這些塗層能夠承受混合合金的腐蝕,同時防止電流腐蝕。 Element Solutions公司報告稱,其電子業務部門2024年第一季的銷售額成長了10%,達到3.94億美元,這表明汽車電氣化正在推動對半導體級化學品的需求。然而,區域整合也帶來了集中風險。中國對鎵和鍺的出口限制正在擾亂用於牽引逆變器的功率裝置的電鍍供應。在亞洲擁有多元化佈局和原料來源的供應商可以降低這些風險,同時利用持續的產量成長。

電子元件小型化需要高精度電鍍。

半導體封裝材料銷售額在經歷了2023年的下滑後,預計在2025年達到260億美元,這主要得益於先進基板運轉率的回升。覆晶和晶圓級封裝對電解鎳、浸金和無氧化物清潔劑的厚度公差要求為±1微米。杜邦公司在日本擴大其光阻劑業務,以及住友化學公司設定的到2030年晶片材料銷售額達到3,000億日圓的目標,都凸顯了市場對超高純度製程化學品日益成長的需求。一些能夠提供低缺陷、高選擇性配方的供應商正在湧現,以取代那些無法將微量污染物控制在兆閾值之一以下的傳統金屬表面處理商。過高的資本密集度和嚴格的無塵室通訊協定提高了進入門檻,使得合格的供應商能夠獲得溢價,從而實現兩位數的利潤率。

對六價鉻的監管更加嚴格

歐盟、加州和英國將於2024年同時實施六價鉻禁令,預計將為整個供應鏈帶來3.31億美元至10.7億美元的累積監管成本。替代方案包括三價鉻、物理氣相沉積濺鍍和氮化鈦陶瓷密封劑。航太主要製造商對替代技術實施多年的認證週期,導致電鍍廠需要維修生產線,加劇了近期產能緊張。由於航空安全法規限制零件通過適航檢驗後更換供應商,早期採用氟鋯酸鹽或鉬酸鹽密封劑的廠商已獲得獨家供應地位。中小型合約加工廠面臨資金壁壘,這可能會加速市場整合。

細分市場分析

到2025年,轉化塗層將佔表面處理化學品市場收入的42.39%,其中汽車、航太和通用工業塗料生產線將佔據市場主導地位。受半導體封裝工廠和積層製造中心對超低殘留清洗液的需求推動,清潔劑預計將以6.77%的複合年成長率快速成長。這種差異體現了一種兩極化:通用磷酸鹽基轉化製程需求旺盛但利潤率較低,而精密清洗劑由於其純度和選擇性標準而保持高價。監管機構正在推動向鋯鈦體系的轉變,該體係可減少污泥和能源消耗,這進一步凸顯了擁有強大配方智慧財產權(IP)的供應商的優勢。專業製造商利用捆綁式清洗和轉換流程來確保多年工廠審核合約並降低客戶流失。

用於鋁電池機殼的第二代陽極氧化添加劑可在提高耐磨性的同時保持良好的焊接性能。其他類型的添加劑,例如生物基密封劑和無鉻混合塗層,則滿足醫療設備和風力發電機葉片等特定應用的需求。隨著原始設備製造商 (OEM) 在全球範圍內推行材料規格標準化,能夠提供跨洲一致化學配方的供應商正在贏得主服務協議。因此,表面處理化學品市場的競爭焦點正從每公升價格轉向生命週期成本,研發預算也逐漸轉向旨在延長鍍液壽命、控制發泡和提高污水處理性能的添加劑組合。

表面處理化學品報告按化學品類型(清潔劑、化學轉化膜等)、基材(金屬、塑膠、其他材料)、終端用戶產業(汽車、建築、電子、工業機械、其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元以金額為準。

區域分析

至2025年,亞太地區將佔表面處理化學品市場收入的42.88%,並在2031年之前以7.05%的複合年成長率成長。在中國,隨著國內經濟獎勵策略提振電動車(EV)供應鏈,預計化學品製造商的利潤將在2025年復甦。印度的特種化學品銷售額預計在2025年將達到3,000億美元,這將支撐智慧型手機組裝和汽車出口對高價值塗料的需求。

在北美,1.2兆美元的《基礎設施投資和就業創造法案》正在加強工業基礎,以支撐對重型設備和橋樑塗料的需求。亞利桑那州、德克薩斯州和紐約州的半導體工廠正在推動符合一級無塵室標準的超純清潔化學品的本地消費。加拿大不斷擴大的離岸風力發電供應鏈將進一步提升對ISO 20340認證塗料的需求。雖然北美地區的成長速度不如亞洲,但嚴格的環境法規以及接近性研發叢集的優勢,創造了高價值的獲利機會。

歐洲在海洋能源和航太領域保持技術領先地位。 2025年實施的NORSOK M-501 Rev 7標準要求塗料必須檢驗,能夠承受長期浸泡和火災環境。綠色交易協議促進了生物基化學的發展。德國和斯堪地那維亞國家對木質素基樹脂提供補貼,並加速淘汰溶劑型鉻酸鹽。南美洲、中東和非洲的發展速度各不相同。巴西的鹽層下油田需要高溫腐蝕抑制劑,而波灣合作理事會國家正在投資建造與汽車出口走廊相關的鋁材軋延廠。儘管總產量仍然不高,但當地的生產要求正迫使跨國供應商建立服務中心,以利用先發優勢,加速工業化進程。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲汽車製造業快速擴張

- 電子元件小型化需要高精度電鍍。

- 風力發電機塔架的嚴格防腐蝕標準

- 原位3D列印金屬零件(需列印後表面處理)

- 電動車平台中鋁材用量的快速成長需要多金屬清洗機

- 市場限制

- 對六價鉻的監管更加嚴格

- 向生物基塗料的轉變將降低對傳統化學品的需求。

- 自建金屬精整線的總擁有成本不斷增加

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依化學類型

- 清潔工

- 化學轉換塗層

- 陽極處理化學品

- 其他化學品

- 按基礎材料

- 金屬

- 塑膠

- 其他基材(玻璃、合金、木材)

- 按最終用戶行業分類

- 汽車和運輸設備

- 建造

- 電子設備

- 工業機械

- 其他(石油和天然氣管道、發電、軍事、包裝等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aalberts Surface Technologies GmbH

- ALANOD GmbH and Co. KG

- Asterion LLC

- BASF

- Bulk Chemicals Inc.

- ChemTech Surface Finishing Pvt. Ltd.

- Dow

- Element Solutions Inc

- Henkel AG and Co. KGaA

- MKS|Atotech

- Nihon Parkerizing Co., Ltd.

- Nippon Paint Holdings Co. Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- Quaker Chemical Corporation

- The Sherwin-Williams Company

- YUKEN INDUSTRY CO.,LTD.

第7章 市場機會與未來展望

Surface Treatment Chemicals Market size in 2026 is estimated at USD 4.76 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 6.57 billion, growing at 6.68% CAGR over 2026-2031.

Strong momentum flows from automotive electrification, semiconductor packaging recovery, and offshore wind installations that demand corrosion-resistant systems. Asian manufacturing hubs account for most new capacity, while North American reshoring programs and European sustainability mandates redirect premium demand toward high-performance, chromium-free formulations. Suppliers that combine semiconductor-grade purity, multi-metal compatibility, and bio-based innovation capture rising value pools as legacy metal-finishing chemistries lose relevance. The surface treatment chemicals market benefits from regulatory convergence that penalizes hexavalent chromium, forcing end-users to adopt alternative coatings and cleaners that comply with strict occupational health and environmental limits.

Global Surface Treatment Chemicals Market Trends and Insights

Rapid Expansion of Automotive Production in Asia

Asia's automakers are scaling multi-material vehicle architectures that depend on cleaners able to prevent cross-contamination between aluminum and steel. Electric-vehicle battery housings, structural castings, and heat-management plates require precision etching and conversion coatings that tolerate mixed alloys without galvanic corrosion. Element Solutions recorded 10% electronics-segment sales growth to USD 394 million in Q1 2024, illustrating how automotive electrification lifts semiconductor-grade chemical volumes. Regional consolidation nonetheless concentrates risk: Chinese export controls on gallium and germanium disrupt plating supply for power-devices embedded in traction inverters. Suppliers with diversified Asian footprints and redundant raw-material sources mitigate these vulnerabilities while capitalizing on sustained output gains.

Electronics Miniaturisation Demanding High-Precision Plating

Semiconductor packaging materials revenues are forecast to climb to USD 26 billion in 2025 after a 2023 downturn, restoring capacity utilization across advanced substrate lines. Flip-chip and wafer-level packages impose +-1 µm thickness tolerances on electroless nickel, immersion gold, and oxide-free cleaners. DuPont's photoresist expansion in Japan and Sumitomo Chemical's JPY 300 billion chip-materials sales goal by 2030 underscore the pull for ultra-pure treatment chemicals. Suppliers that deliver low-defect, high-selectivity formulations displace traditional metal finishers whose processes cannot control trace contaminants below parts-per-trillion thresholds. Outsized capital intensity and strict cleanroom protocols raise barriers, enabling premium pricing that supports double-digit contribution margins for qualified vendors.

Regulatory Clamp-Down on Hexavalent Chromium

The European Union, California, and the United Kingdom enacted parallel bans on hexavalent chromium during 2024, triggering cumulative compliance outlays estimated between USD 331 million and USD 1.07 billion across the supply chain. Transition pathways include trivalent chromium, PVD sputtering, and ceramic titanium-nitride sealers. Aerospace primes impose multiyear qualification cycles for alternatives, tightening near-term capacity as plating shops retrofit lines. Early adopters of fluorozirconate or molybdate sealing chemistries secure sole-source positions because flight-safety regulations discourage supplier substitutions once parts pass airworthiness validation. Smaller job shops face capital barriers that may accelerate market consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Anti-Corrosion Standards in Wind-Turbine Towers

- On-Site 3D-Printed Metal Parts Requiring Post-Print Surface Prep

- Shift Toward Bio-Based Coatings Reduces Legacy Chemical Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conversion coatings generated 42.39% of 2025 revenue within the surface treatment chemicals market, anchored by automotive, aerospace, and general-industrial paint lines. Cleaners are projected to post the fastest 6.77% CAGR as semiconductor packaging plants and additive-manufacturing hubs demand ultra-low residue baths. This divergence signals a bifurcation: commodity phosphate-based conversions attract volume but modest margins, whereas precision cleaners command high price points due to purity and selectivity thresholds. Regulators are driving a shift to zirconium and titanium systems that lower sludge and energy usage, further differentiating suppliers that possess strong formulation IP. Specialty players leverage bundled cleaner-conversion packages to lock in multi-year plant audits, limiting churn.

Second-generation anodizing additives for aluminum battery enclosures strengthen wear resistance while maintaining weldability. Other types, including bio-derived sealers and chromium-free hybrid films, address niche specifications in medical instruments and wind-turbine blades. As OEMs standardize global material specifications, suppliers that offer consistent chemistries across continents win master-service agreements. Consequently, the surface treatment chemicals market sees a migration of research budgets toward additive packages that improve bath longevity, foaming control, and wastewater treatability, intensifying competition on lifecycle cost rather than per-liter pricing.

The Surface Treatment Chemicals Report is Segmented by Chemical Type (Cleaner, Chemical Conversion Coating, and More), Base Material (Metal, Plastic and Other Materials), End-User Industry (Automotive, Construction, Electronics, Industrial Machinery, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 42.88% of 2025 revenue within the surface treatment chemicals market and is expanding at a 7.05% CAGR to 2031. China forecasts a profit rebound for its chemical producers in 2025 amid a domestic stimulus that boosts EV supply chains. India's specialty-chemical turnover is scheduled to reach USD 300 billion in 2025, feeding demand for high-value coatings used in smart-phone assembly and automotive exports.

North America is reinforcing its industrial base through the USD 1.2 trillion Infrastructure Investment and Jobs Act, which underpins heavy-equipment and bridge-coating demand. Semiconductor fabs in Arizona, Texas, and New York fuel localized consumption of ultra-pure cleaners that meet Class 1 cleanroom thresholds. Canada's offshore wind supply-chain build-out further widens the need for ISO 20340-certified coatings. Although growth rates trail Asia, premium margin opportunities arise from tight environmental regulations and proximity to research and development clusters.

Europe retains technological leadership in offshore energy and aerospace. The implementation of NORSOK M-501 Rev 7 in 2025 demands coatings validated for long-term immersion and fire exposure. Green-deal policies advance bio-based chemistries; Germany and Scandinavia subsidize lignin-derived resins, accelerating the phase-out of solvent-borne chromates. South America and Middle East Africa are emerging at different paces: Brazil's pre-salt oilfields require high-temperature corrosion inhibitors, while Gulf Cooperation Council states invest in aluminum rolling mills linked to automotive export corridors. Although combined volumes remain modest, local production mandates push multinational suppliers to establish service hubs, unlocking early-mover advantages as industrialization accelerates.

- Aalberts Surface Technologies GmbH

- ALANOD GmbH and Co. KG

- Asterion LLC

- BASF

- Bulk Chemicals Inc.

- ChemTech Surface Finishing Pvt. Ltd.

- Dow

- Element Solutions Inc

- Henkel AG and Co. KGaA

- MKS | Atotech

- Nihon Parkerizing Co., Ltd.

- Nippon Paint Holdings Co. Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- Quaker Chemical Corporation

- The Sherwin-Williams Company

- YUKEN INDUSTRY CO.,LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Automotive Production in Asia

- 4.2.2 Electronics Miniaturisation Demanding High-Precision Plating

- 4.2.3 Stringent Anti-Corrosion Standards in Wind-Turbine Towers

- 4.2.4 On-Site 3D-Printed Metal Parts Requiring Post-Print Surface Prep

- 4.2.5 Surge in Aluminium Use in EV Platforms Necessitating Multi-Metal Cleaners

- 4.3 Market Restraints

- 4.3.1 Regulatory Clamp-Down on Hexavalent Chromium

- 4.3.2 Shift Toward Bio-Based Coatings Reduces Legacy Chemical Demand

- 4.3.3 Rising Total-Cost-of-Ownership of Captive Metal Finishing Lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chemical Type

- 5.1.1 Cleaner

- 5.1.2 Chemical Conversion Coating

- 5.1.3 Anodizing Chemicals

- 5.1.4 Other Types of Chemicals

- 5.2 By Base Material

- 5.2.1 Metal

- 5.2.2 Plastic

- 5.2.3 Other Base Materials (Glass, Alloys, Wood)

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction

- 5.3.3 Electronics

- 5.3.4 Industrial Machinery

- 5.3.5 Others (Oil and Gas Pipeline, Power, Military, Packaging, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aalberts Surface Technologies GmbH

- 6.4.2 ALANOD GmbH and Co. KG

- 6.4.3 Asterion LLC

- 6.4.4 BASF

- 6.4.5 Bulk Chemicals Inc.

- 6.4.6 ChemTech Surface Finishing Pvt. Ltd.

- 6.4.7 Dow

- 6.4.8 Element Solutions Inc

- 6.4.9 Henkel AG and Co. KGaA

- 6.4.10 MKS | Atotech

- 6.4.11 Nihon Parkerizing Co., Ltd.

- 6.4.12 Nippon Paint Holdings Co. Ltd.

- 6.4.13 OC Oerlikon Management AG

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Quaker Chemical Corporation

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 YUKEN INDUSTRY CO.,LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球表面處理化學品市場,2025-2032年

全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球表面處理化學品市場,2025-2032年 表面處理化學品市場預測至2034年-全球產品類型、化學品類型、基礎化學、製程類型、基材、應用和區域分析

表面處理化學品市場預測至2034年-全球產品類型、化學品類型、基礎化學、製程類型、基材、應用和區域分析 表面處理化學品市場規模、佔有率和趨勢分析報告:按材料、化學品、處理方法、最終用途、地區和細分市場預測(2026-2033 年)

表面處理化學品市場規模、佔有率和趨勢分析報告:按材料、化學品、處理方法、最終用途、地區和細分市場預測(2026-2033 年) 混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測

混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測 表面處理市場機會、成長要素、產業趨勢分析及2026-2035年預測。

表面處理市場機會、成長要素、產業趨勢分析及2026-2035年預測。 2026年全球混凝土表面加固劑市場報告全球化學表面處理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年

2026年全球混凝土表面加固劑市場報告全球化學表面處理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年