|

市場調查報告書

商品編碼

2019097

液體包裝紙盒市場機會、成長要素、產業趨勢分析及2026-2035年預測Liquid Packaging Cartons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

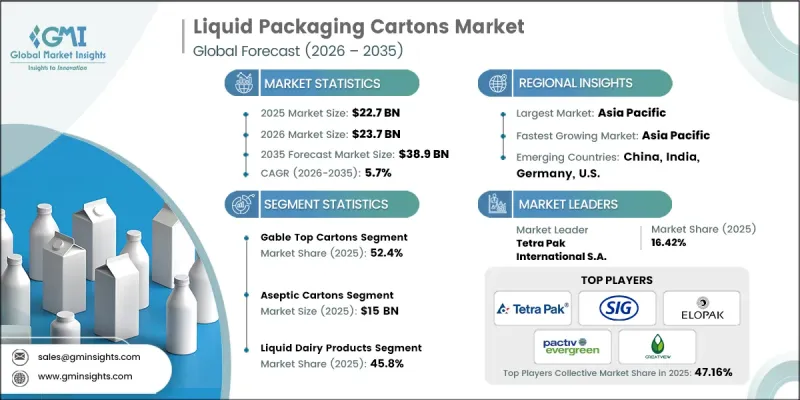

預計到 2025 年,全球液體紙盒市場價值將達到 227 億美元,並預計以 5.7% 的複合年成長率成長,到 2035 年達到 389 億美元。

市場成長主要受消費者購買行為快速變化的驅動,尤其是數位化零售通路日益增強的影響力。消費者對便利、耐用且永續的包裝解決方案的需求不斷成長,加速了飲料和生鮮食品液體紙盒包裝的普及。同時,即飲液體產品全球消費量的成長也顯著促進了市場擴張。生活方式的改變、都市化的加速以及健康意識的增強,促使消費者選擇包裝飲料,從而推動了對高效包裝形式的需求。製造商正日益致力於開發輕量化和環保解決方案,以滿足永續性目標和監管要求。向環保替代包裝的轉變正在推動產業創新,企業力求在確保產品安全性和便利性的同時,減少對環境的影響。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 227億美元 |

| 預測金額 | 389億美元 |

| 複合年成長率 | 5.7% |

預計到2035年,磚形紙盒市場將以4.5%的複合年成長率成長,在液體包裝紙盒市場保持強勁地位。這種形狀的紙盒因其結構強度高、儲存容量大且能延長產品保存期限而廣受歡迎。先進包裝技術的日益普及推動了該細分市場的成長,尤其是在長期維持產品品質方面的有效性。這些紙盒設計有助於維持產品質量,同時確保安全並降低污染風險,使其成為液體包裝應用的可靠選擇。

到2025年,液態乳製品市佔率將達到45.8%。全球對乳類飲料的需求持續成長,鞏固了該領域的領先地位。隨著高價值乳製品的不斷湧現,製造商擴大採用能夠延長產品保存期限的先進包裝。具有先進阻隔性能的高性能紙盒結構正日益受到青睞,因為它們有助於保持產品新鮮度,同時減少對外部儲存條件的依賴。

到2025年,北美液體包裝紙盒市佔率將達到27.9%。在消費者環保意識不斷增強和旨在減少環境影響的監管措施的推動下,該地區正朝著更永續和可回收的包裝解決方案轉型。隨著可生物分解和可堆肥材料的開發,對低塑膠含量包裝的需求也不斷成長。全行業致力於提高食品安全、增強永續性和提高回收效率的努力,進一步推動了市場成長。對創新包裝技術和環保材料的持續投資,正在鞏固該地區在全球市場的地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 包裝飲料消費量增加

- 對永續和環保包裝解決方案的需求日益成長

- 乳製品消費量增加

- 電子商務和宅配服務的擴展

- 即飲飲料市場成長

- 產業潛在風險與挑戰

- 高昂的初始生產成本與回收成本

- 它對碳酸飲料的適用性有限。

- 市場機遇

- 採用先進的智慧功能包裝技術

- 提高新興地區的滲透率

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估價與預測:依紙箱類型分類,2022-2035年

- 山形蓋頂紙箱

- 標準山形蓋頂

- Freshlock山形蓋頂帶可重複密封蓋

- 纖細山形蓋頂

- 磚形紙盒

- 標準磚

- 纖薄磚

- 方形磚

- 異形紙箱

- 紙盒瓶

- 異形紙箱

第6章 市場估算與預測:依技術分類的儲存週期,2022-2035年

- 無菌紙盒

- 符合超高溫瞬時滅菌標準的無菌系統

- 長期儲存(ESL)無菌系統

- 非無菌紙盒

- 巴氏殺菌產品紙盒

- 用於新鮮農產品和冷藏配送的紙箱

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 液態乳製品

- 生牛奶

- 風味牛奶

- 液態優格

- 奶油和酪乳

- 其他

- 非碳酸飲料

- 果汁/果漿

- 冰茶和檸檬水

- 植物來源飲料

- 運動能量飲料

- 流質食品

- 高湯醬汁

- 醬汁和烹飪高湯醬汁

- 液態蛋和乳製品替代品

- 其他液體

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 世界公司

- Elopak AS

- Greatview Aseptic Packaging Co. Ltd.

- Pactiv Evergreen Inc.

- SIG Combibloc Group AG

- Smurfit Kappa Group plc

- Stora Enso Oyj

- Tetra Pak International SA

- 該地區頂尖公司

- Klabin SA

- Nampak Ltd.

- Nippon Paper Industries Co. Ltd.

- Oji Holdings Corporation

- Visy Industries

- 新興企業

- IPI Srl(Coesia)

- Lami Packaging(Kunshan)Co. Ltd.

- Parksons Packaging Ltd.

- TidePak Aseptic Packaging Material Co. Ltd.

- UFlex Limited(ASEPTO)

The Global Liquid Packaging Cartons Market was valued at USD 22.7 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 38.9 billion by 2035.

Market growth is driven by the rapid evolution of consumer purchasing behavior, particularly with the increasing influence of digital retail channels. The growing demand for convenient, durable, and sustainable packaging solutions is accelerating the adoption of liquid cartons for packaged beverages and perishable goods. At the same time, rising global consumption of ready-to-consume liquid products is contributing significantly to market expansion. Changing lifestyle patterns, increasing urbanization, and heightened health awareness are encouraging consumers to choose packaged beverages, which in turn is supporting demand for efficient packaging formats. Manufacturers are increasingly focusing on developing lightweight and environmentally responsible solutions to align with sustainability goals and regulatory expectations. The shift toward eco-conscious packaging alternatives is also shaping innovation within the industry, as companies aim to reduce environmental impact while maintaining product safety and convenience.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.7 Billion |

| Forecast Value | $38.9 Billion |

| CAGR | 5.7% |

The brick cartons segment is expected to grow at a CAGR of 4.5% through 2035, maintaining a strong position within the liquid packaging cartons market. This format is widely preferred due to its structural strength, efficient storage capabilities, and ability to extend product shelf life. Increasing adoption of advanced packaging technologies is supporting the segment's growth, particularly due to its effectiveness in preserving product quality over extended durations. The design of these cartons helps maintain product integrity while ensuring safety and reducing contamination risks, making them a reliable choice for liquid packaging applications.

The liquid dairy products segment accounted for 45.8% share in 2025. Strong global demand for dairy-based beverages continues to support this segment's dominance. The introduction of value-added and enhanced dairy offerings is encouraging manufacturers to adopt advanced packaging solutions that improve product longevity. High-performance carton structures with advanced barrier properties are gaining preference, as they help maintain freshness while reducing dependency on external storage conditions.

North America Liquid Packaging Cartons Market held a 27.9% share in 2025. The region is experiencing a transition toward more sustainable and recyclable packaging solutions, driven by increasing consumer awareness and regulatory initiatives aimed at reducing environmental impact. The demand for packaging with lower plastic content is rising, alongside the development of biodegradable and compostable materials. Industry-wide efforts focused on improving food safety, enhancing sustainability, and increasing recycling efficiency are further supporting market growth. Continuous investments in innovative packaging technologies and eco-friendly materials are strengthening the region's position within the global landscape.

Key companies operating in the Global Liquid Packaging Cartons Market include Elopak AS, Greatview Aseptic Packaging Co. Ltd., IPI Srl (Coesia), Klabin S.A., Lami Packaging (Kunshan) Co. Ltd., Nampak Ltd., Nippon Paper Industries Co. Ltd., Oji Holdings Corporation, Pactiv Evergreen Inc., Parksons Packaging Ltd., SIG Combibloc Group AG, Smurfit Kappa Group plc, Stora Enso Oyj, Tetra Pak International S.A., TidePak Aseptic Packaging Material Co. Ltd., UFlex Limited (ASEPTO), and Visy Industries. Companies in the Global Liquid Packaging Cartons Market are strengthening their market position through innovation, sustainability initiatives, and strategic expansion. A key focus is being placed on developing recyclable and biodegradable packaging materials to align with evolving environmental regulations and consumer preferences. Firms are investing in advanced manufacturing technologies to enhance product durability and efficiency while reducing material usage. Strategic partnerships and collaborations help companies expand their geographic reach and improve distribution capabilities. Additionally, organizations are focusing on product differentiation through improved design and functionality.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Carton type trends

- 2.2.2 Shelf-life technology trends

- 2.2.3 End-use application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumption of packaged beverages

- 3.2.1.2 Rising demand for sustainable and eco-friendly packaging solutions

- 3.2.1.3 Growth in dairy product consumption

- 3.2.1.4 Expansion of e-commerce and home delivery services

- 3.2.1.5 Growth in the ready-to-drink (RTD) beverage market

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial production and recycling costs

- 3.2.2.2 Limited suitability for carbonated beverages

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of advanced smart and functional packaging technologies

- 3.2.3.2 Increasing penetration in emerging regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Carton Type, 2022 - 2035 (USD Billion & Kilo tons)

- 5.1 Key trends

- 5.2 Gable top cartons

- 5.2.1 Standard gable top

- 5.2.2 Fresh-lock gable top with reclosable cap

- 5.2.3 Slim gable top

- 5.3 Brick cartons

- 5.3.1 Standard brick

- 5.3.2 Slim brick

- 5.3.3 Square brick

- 5.4 Shaped cartons

- 5.4.1 Carton bottles

- 5.4.2 Custom shaped cartons

Chapter 6 Market Estimates and Forecast, By Shelf-Life Technology, 2022 - 2035 (USD Billion & Kilo tons)

- 6.1 Key trends

- 6.2 Aseptic cartons

- 6.2.1 Uht-compatible aseptic systems

- 6.2.2 Extended shelf life (ESL) aseptic systems

- 6.3 Non-aseptic cartons

- 6.3.1 Pasteurized product cartons

- 6.3.2 Fresh/chilled distribution cartons

Chapter 7 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 (USD Billion & Kilo tons)

- 7.1 Key trends

- 7.2 Liquid dairy products

- 7.2.1 Fresh milk

- 7.2.2 Flavored milk

- 7.2.3 Liquid yogurt

- 7.2.4 Cream & buttermilk

- 7.2.5 Others

- 7.3 Non-carbonated soft drinks

- 7.3.1 Fruit juices & nectars

- 7.3.2 Iced tea & lemonades

- 7.3.3 Plant-based beverages

- 7.3.4 Sports & energy drinks

- 7.4 Liquid foods

- 7.4.1 Soups & broths

- 7.4.2 Sauces & cooking stocks

- 7.4.3 Liquid eggs & dairy alternatives

- 7.5 Other liquids

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Elopak AS

- 9.1.2 Greatview Aseptic Packaging Co. Ltd.

- 9.1.3 Pactiv Evergreen Inc.

- 9.1.4 SIG Combibloc Group AG

- 9.1.5 Smurfit Kappa Group plc

- 9.1.6 Stora Enso Oyj

- 9.1.7 Tetra Pak International S.A.

- 9.2 Regional Champions

- 9.2.1 Klabin S.A.

- 9.2.2 Nampak Ltd.

- 9.2.3 Nippon Paper Industries Co. Ltd.

- 9.2.4 Oji Holdings Corporation

- 9.2.5 Visy Industries

- 9.3 Emerging Players

- 9.3.1 IPI Srl (Coesia)

- 9.3.2 Lami Packaging (Kunshan) Co. Ltd.

- 9.3.3 Parksons Packaging Ltd.

- 9.3.4 TidePak Aseptic Packaging Material Co. Ltd.

- 9.3.5 UFlex Limited (ASEPTO)

液態紙板市場:按液體類型、包裝類型、纖維原料、紙箱尺寸和銷售管道分類-全球市場預測(2026-2032 年)山形蓋頂液體紙盒市場:按滅菌方法、瓶蓋類型、塗層、應用和分銷管道分類-2026-2032年全球市場預測

液態紙板市場:按液體類型、包裝類型、纖維原料、紙箱尺寸和銷售管道分類-全球市場預測(2026-2032 年)山形蓋頂液體紙盒市場:按滅菌方法、瓶蓋類型、塗層、應用和分銷管道分類-2026-2032年全球市場預測 液體包裝紙盒市場規模、佔有率、趨勢和預測:按紙盒類型、包裝類型、保存期限、最終用戶和地區分類,2026-2034年液體包裝紙盒市場:按類型、材料、紙盒尺寸、技術、分銷管道、應用和最終用戶產業分類-2026-2032年全球市場預測

液體包裝紙盒市場規模、佔有率、趨勢和預測:按紙盒類型、包裝類型、保存期限、最終用戶和地區分類,2026-2034年液體包裝紙盒市場:按類型、材料、紙盒尺寸、技術、分銷管道、應用和最終用戶產業分類-2026-2032年全球市場預測 液體包裝紙盒市場規模、佔有率和成長分析:按紙盒類型、保存期限、最終用途、地區和行業預測,2026-2033年

液體包裝紙盒市場規模、佔有率和成長分析:按紙盒類型、保存期限、最終用途、地區和行業預測,2026-2033年 液體包裝紙盒市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年磚型液體包裝市場規模、佔有率、成長和全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

液體包裝紙盒市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年磚型液體包裝市場規模、佔有率、成長和全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 液體包裝紙盒:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)屋頂型液體紙盒市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024-2032年預測

液體包裝紙盒:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)屋頂型液體紙盒市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2024-2032年預測 液體包裝紙盒市場:按產品類型、材料類型、開啟方式、應用和地區分類

液體包裝紙盒市場:按產品類型、材料類型、開啟方式、應用和地區分類