|

市場調查報告書

商品編碼

2019071

乾蜂蜜市場機會、成長要素、產業趨勢分析及2026-2035年預測Dried Honey Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

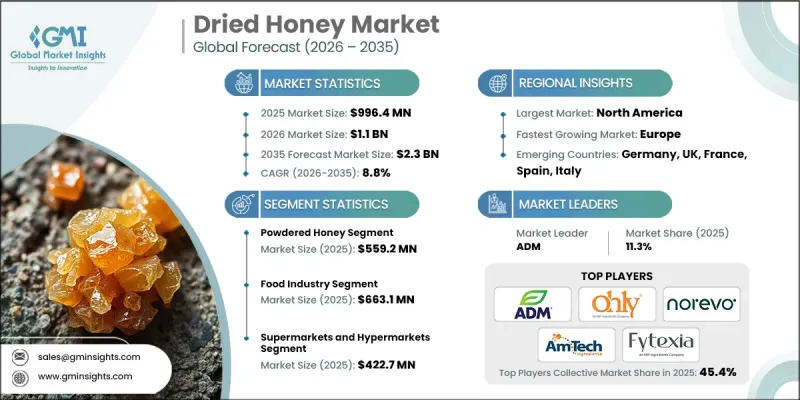

預計到 2025 年,全球乾蜂蜜市場價值將達到 9.964 億美元,年複合成長率為 8.8%,到 2035 年將達到 23 億美元。

乾蜂蜜有粉末狀和顆粒狀兩種形式,保留了液態蜂蜜的天然甜味和功能性益處,同時具有更優異的加工性能、穩定的品質和更長的保存期限。它廣泛用作食品、飲料、營養補充劑和烘焙點心食品中的甜味劑,特別適用於對水分控制要求較高的場合。本產品能與乾燥原料完美融合,因此也適用於營養粉、穀物、糖果甜點及調味料混合物。噴霧乾燥和低溫脫水技術的進步提高了乾蜂蜜的溶解性、流動性和顆粒均勻性,同時保留了其風味和天然成分。這些創新增強了乾蜂蜜在加工食品和包裝產品中的應用,使製造商能夠為工業和烹飪應用提供品質穩定的產品。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 9.964億美元 |

| 預測金額 | 23億美元 |

| 複合年成長率 | 8.8% |

預計到2025年,蜂蜜粉市場規模將達到5.592億美元。蜂蜜粉易於加工,且水分含量可調節,因此成為烘焙混合料、飲料、營養補充劑和調味品混合物中理想的甜味劑。生產商提供不同溶解度和蜂蜜濃度的產品,從而能夠根據不同的產品應用需求進行精準配方。

預計到2025年,食品業市場規模將達到6.631億美元。乾蜂蜜可用作烘焙產品、早餐用麥片穀類、零嘴零食、飲料和乾粉混合物中的天然甜味劑,具有風味穩定且易於加工的優點。在營養保健品領域,乾蜂蜜也被用於膳食補充劑、蛋白粉和健康產品中,因為其天然特性符合潔淨標示的要求。

預計北美乾蜂蜜市場將顯著成長,從2025年的3.547億美元成長到2035年的8.562億美元。這一成長主要受以下因素驅動:消費者對天然成分的偏好增強、加工食品配方的改進以及烘焙、零食和飲料中對粉狀甜味劑需求的成長。隨著生產商更加重視潔淨標示和便利的配方,乾蜂蜜在美國營養棒、穀物和簡便食品市場也越來越受歡迎。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 在全球範圍內,人們越來越偏好在食品中使用天然甜味劑。

- 擴大粉狀原料在食品加工的應用

- 各種應用領域對保存期限長的原料的需求

- 陷阱與挑戰

- 蜂蜜在乾燥過程中的營養敏感性

- 與液態蜂蜜產品相比,其生產成本更高。

- 機會

- 拓展全球潔淨標示天然成分產品的市場。

- 營養保健品和膳食補充品產品領域的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 蜂蜜粉

- 顆粒劑蜂蜜

- 蜂蜜晶體

第6章 市場估算與預測:依最終用戶分類,2022-2035年

- 食品工業

- 營養保健品

- 化妝品和個人護理

- 其他

第7章 市場估價與預測:依通路分類,2022-2035年

- 線上零售

- 超級市場/大賣場

- 健康食品店

- 便利商店

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Ohly

- Mitthi Foods

- AmTech Ingredients

- ADM

- Essentra Natural

- Flavor Consultants, Inc.

- Mevive International

- Fytexia

- Norevo

- AVNI HERBAL &HEALTHCARE

- Vedant Agro Foods

The Global Dried Honey Market was valued at USD 996.4 million in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 2.3 billion by 2035.

Dried honey, available in powdered or granulated forms, retains the natural sweetness and functional benefits of liquid honey while offering superior handling, consistent quality, and longer storage. It is widely used as a sweetening agent in food, beverages, dietary supplements, and baked goods where moisture control is critical. The product integrates seamlessly with dry ingredients, making it suitable for nutrition powders, cereals, confectionery, and seasoning mixes. Technological advancements in spray drying and low-temperature dehydration have improved solubility, flow properties, and particle uniformity while preserving flavor and natural compounds. These innovations enhance usability in processed foods and packaged products, allowing manufacturers to deliver consistent quality across industrial and culinary applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $996.4 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 8.8% |

The powdered honey segment generated USD 559.2 million in 2025. Its ease of handling and controlled moisture content make it the preferred sweetener for bakery mixes, beverages, nutritional powders, and seasoning blends. Manufacturers offer varying solubility and honey concentration levels, enabling precise formulation for diverse product applications.

The food industry accounted for USD 663.1 million in 2025. Dried honey serves as a natural sweetener in bakery products, breakfast cereals, snack foods, beverages, and dry mix products, providing consistent flavor and ease of processing. Nutraceuticals also utilize dried honey in dietary supplements, protein powders, and wellness formulations, where its natural origin aligns with clean-label requirements.

North America Dried Honey Market is expected to see substantial growth, expanding from USD 354.7 million in 2025 to USD 856.2 million by 2035. Rising consumer preference for natural ingredients, reformulation trends in processed foods, and increasing demand for powdered sweeteners in baking, snacks, and beverages are driving market growth. Dried honey is gaining popularity in the U.S. nutrition bar, cereal, and convenience food markets as manufacturers focus on clean-label and easy-to-use formulations.

Key players operating in the Global Dried Honey Market include Ohly, ADM, Mitthi Foods, Mevive International, AVNI HERBAL & HEALTHCARE, Vedant Agro Foods, Essentra Natural, Fytexia, Norevo, and Flavor Consultants, Inc. Companies in the Global Dried Honey Market are adopting multiple strategies to strengthen their market position and expand their footprint. They characteristics and advanced drying technologies such as spray drying and low-temperature dehydration to improve solubility, flow characteristics, and flavor retention. Firms develop customizable honey powders with varying concentration levels to cater to specific food and nutraceutical applications. Strategic partnerships with food manufacturers and nutraceutical brands help integrate products into high-volume production lines. Expanding distribution networks, including e-commerce channels, ensures access to new geographic markets. Additionally, companies emphasize sustainability, clean-label offerings, and natural ingredient positioning to attract health-conscious consumers and secure long-term contracts in the food and dietary supplement sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 End User

- 2.2.3 Distribution Channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing preference for natural sweeteners in foods globally

- 3.2.1.2 Growing use of powdered ingredients in processing foods

- 3.2.1.3 Demand for longer shelf life ingredients in applications

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Sensitivity of honey nutrients during drying processes operations

- 3.2.2.2 Higher production costs compared to liquid honey formats

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of clean label and natural formulations worldwide

- 3.2.3.2 Growth in nutraceutical and supplement products segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Powdered honey

- 5.3 Granulated honey

- 5.4 Honey crystals

Chapter 6 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food industry

- 6.3 Nutraceuticals

- 6.4 Cosmetics and personal care

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Online retail

- 7.3 Supermarkets/hypermarkets

- 7.4 Health food stores

- 7.5 Convenience stores

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ohly

- 9.2 Mitthi Foods

- 9.3 AmTech Ingredients

- 9.4 ADM

- 9.5 Essentra Natural

- 9.6 Flavor Consultants, Inc.

- 9.7 Mevive International

- 9.8 Fytexia

- 9.9 Norevo

- 9.10 AVNI HERBAL & HEALTHCARE

- 9.11 Vedant Agro Foods

全球蜂蜜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球蜂蜜粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球蜂蜜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球蜂蜜粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 蜂蜜市場規模、佔有率和成長分析(按加工方法、通路、產品類型、應用、包裝和地區分類)-2026-2033年產業預測

蜂蜜市場規模、佔有率和成長分析(按加工方法、通路、產品類型、應用、包裝和地區分類)-2026-2033年產業預測 蜂蜜市場-全球產業規模、佔有率、趨勢、機會和預測,按加工方式、按包裝、按銷售管道(百貨公司、藥局、大賣場/超市、線上、其他)、按地區和競爭情況分類,2020-2030 年預測蜜蜂補充劑市場-全球產業規模、佔有率、趨勢、機會與預測,按形式、按價格區間、按包裝、按配銷通路、按地區和競爭進行細分,2020 年至 2030 年全球蜂蜜市場規模(按來源、加工、用途、地區和預測)

蜂蜜市場-全球產業規模、佔有率、趨勢、機會和預測,按加工方式、按包裝、按銷售管道(百貨公司、藥局、大賣場/超市、線上、其他)、按地區和競爭情況分類,2020-2030 年預測蜜蜂補充劑市場-全球產業規模、佔有率、趨勢、機會與預測,按形式、按價格區間、按包裝、按配銷通路、按地區和競爭進行細分,2020 年至 2030 年全球蜂蜜市場規模(按來源、加工、用途、地區和預測) 阿洛酮糖結晶至2030年的市場預測:按產品類型、分銷管道、應用、最終用戶和地區的全球分析

阿洛酮糖結晶至2030年的市場預測:按產品類型、分銷管道、應用、最終用戶和地區的全球分析 蜂蜜市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

蜂蜜市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 蜂蜜市場:市場分析與2033年前的預測 - 各類型,各產品,各用途,不同形態,各終端用戶,各技術,各零件,各流程,各設備,各地區2030 年蜂蜜醬市場預測:按產品類型、加工、包裝、價格細分、應用、分銷管道和地區進行的全球分析

蜂蜜市場:市場分析與2033年前的預測 - 各類型,各產品,各用途,不同形態,各終端用戶,各技術,各零件,各流程,各設備,各地區2030 年蜂蜜醬市場預測:按產品類型、加工、包裝、價格細分、應用、分銷管道和地區進行的全球分析