|

市場調查報告書

商品編碼

1998855

麥芽糊精市場機會、成長要素、產業趨勢分析及2026-2035年預測Maltodextrin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球麥芽糊精市場價值為 41 億美元,預計到 2035 年將達到 61 億美元,年複合成長率為 4.3%。

麥芽糊精市場的成長主要得益於其廣泛的功能多樣性以及在各種產品配方中作為多功能成分的作用。麥芽糊精因其能夠作為填充劑、增稠劑、質地改良劑以及風味和營養成分的載體而被廣泛應用,已成為眾多生產過程中不可或缺的成分。其中性風味、高消化率以及改善產品口感的能力,使其在各種食品飲料配方和營養產品中廣泛使用。消費者對便利型產品的日益成長的需求,也持續推動麥芽糊精市場的穩定擴張。除了在食品加工領域的傳統應用外,由於其穩定性、黏合性和成膜性,麥芽糊精在製藥、個人護理和工業領域的應用也日益廣泛。此外,該成分與其他配方具有良好的相容性,同時保持了成本效益高的生產特性。同時,為了滿足不斷變化的消費者期望,麥芽糊精產業正透過潔淨標示計劃、探索替代碳水化合物來源以及改進加工技術等舉措,逐步實現原料的多樣化採購。這些因素持續影響全球麥芽糊精市場的產品創新、配方開發和競爭力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 41億美元 |

| 預測金額 | 61億美元 |

| 複合年成長率 | 4.3% |

預計到2025年,玉米衍生原料市場規模將達到25億美元,並在2026年至2035年間以4%的複合年成長率成長。在眾多原料來源中,玉米衍生麥芽糊精憑藉其可靠的功能特性和穩定的加工性能,在市場上佔有穩固的地位。由於玉米衍生麥芽糊精能夠在各種配方中始終保持理想的質地特性和中性的感官特性,因此深受生產商的青睞。此外,完善的玉米衍生麥芽糊精生產基礎設施確保了穩定的供應和可靠的品質標準。這些特性使其成為眾多應用領域的首選原料,包括食品、藥品和個人保健產品配方,在這些領域,均勻的黏度、溶解度和體積對於維持產品的一致性至關重要。

預計到2025年,食品級麥芽糊精市場規模將達27億美元,並在2026年至2035年間以3.8%的複合年成長率成長。食品級麥芽糊精因其中性口味、可靠的功能性和符合嚴格的食品安全標準,在麥芽糊精市場中佔據核心地位。產品開發人員利用這種成分來調整各種加工食品配方中的質地、改善口感、提高溶解度和調節甜度。它與各種香精、甜味劑、蛋白質和色素的相容性使製造商能夠在保持產品配方穩定的同時,獲得可預測的感官特性。食品級麥芽糊精被廣泛用作載體、填充劑和質地改良劑,其強勁的應用需求持續推動產品配方的重新調整,旨在提高性能、最佳化生產成本並保持原料的透明度。

預計到2025年,北美麥芽糊精市場規模將達15億美元。該地區的需求穩定,這主要得益於加工食品、特殊營養補充品和醫藥應用領域的高消費量。美國在推動該地區市場成長方面發揮關鍵作用,因為製造商越來越注重原料透明度,並致力於開發符合消費者不斷變化的期望的潔淨標示配方。此外,高度發展的食品製造業以及對易消化碳水化合物原料的持續需求,也推動了全部區域的市場擴張。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依來源分類,2022-2035年

- 玉米衍生

- 小麥衍生

- 馬鈴薯衍生性商品

- 源自木薯

- 其他

第6章 市場估算與預測:依等級分類,2022-2035年

- 食品級

- 醫藥級

- 工業級

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 飲食

- 烘焙點心

- 糖果甜點

- 乳製品

- 飲料

- 速食

- 其他

- 製藥

- 藥物製劑中的添加劑

- 營養補充品

- 化妝品和個人護理

- 護膚品

- 護髮產品

- 工業應用

- 黏合劑

- 粘合劑

- 塗層和封裝

- 其他

- 動物飼料

- 發酵過程

第8章 市場估算與預測:依葡萄糖當量 (DE) 範圍分類,2022-2035 年

- 低DE麥芽糊精

- 中等DE麥芽糊精

- 高DE麥芽糊精

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- AGRANA Group

- Archer Daniels Midland

- Avebe

- Cargill

- Golden Grain Group

- Grain Processing Corporation

- Gulshan Polyols

- Ingredion

- Matsutani America

- Mengzhou Tailijie

- Roquette Freres

- Tate & Lyle

- Zhucheng Dongxiao Biotechnology

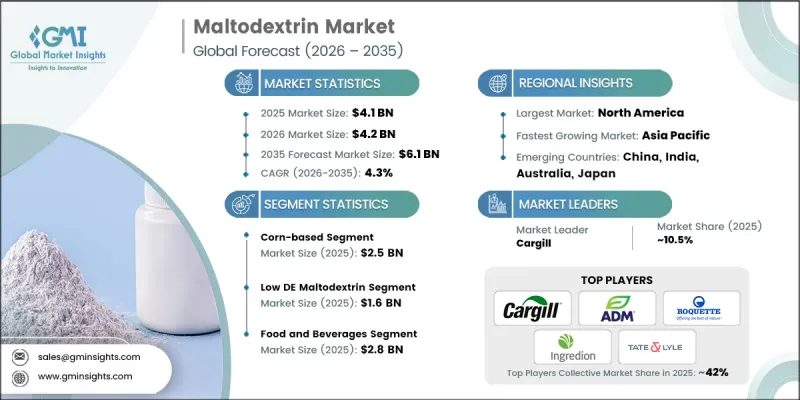

The Global Maltodextrin Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 6.1 billion by 2035.

Growth in the maltodextrin market is supported by its wide functional versatility and its role as a multifunctional ingredient in various product formulations. Maltodextrin is widely utilized for its ability to act as a bulking agent, thickener, texture modifier, and carrier for flavors and nutrients, making it an essential component in numerous production processes. Its neutral flavor profile, high digestibility, and ability to improve product mouthfeel have contributed to its broad adoption across diverse food and beverage formulations as well as nutritional products. Rising consumption of convenience-oriented products continues to support the steady expansion of the maltodextrin market. Beyond its traditional role in food processing, maltodextrin is increasingly used in pharmaceutical, personal care, and industrial applications due to its stabilizing, binding, and film-forming capabilities. The ingredient also offers strong compatibility with other formulation components while maintaining cost-efficient manufacturing characteristics. At the same time, the industry is gradually responding to evolving consumer expectations by exploring alternative carbohydrate sources and improved processing technologies that support cleaner labeling practices and diversified raw material inputs. These factors continue to influence product innovation, formulation development, and competitive dynamics across the global maltodextrin market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 4.3% |

The corn-based segment generated USD 2.5 billion in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. Among different raw material sources, corn-derived maltodextrin maintains a strong market position due to its reliable functional characteristics and stable processing performance. Manufacturers frequently select this source because it consistently delivers the desired textural qualities while maintaining a neutral sensory profile across various formulations. In addition, the well-established production infrastructure supporting corn-based maltodextrin enables consistent supply availability and dependable quality standards. These characteristics make it a preferred ingredient for use across numerous applications, including food, pharmaceutical, and personal care product formulations, where uniform viscosity, solubility, and bulk properties are essential for maintaining product consistency.

The food-grade segment accounted for USD 2.7 billion in 2025 and is projected to grow at a CAGR of 3.8% during 2026-2035. Food-grade maltodextrin plays a central role within the maltodextrin market because it offers a neutral taste profile, reliable functionality, and compliance with strict food safety standards. Product developers rely on this ingredient to adjust texture, improve mouthfeel, enhance solubility, and manage sweetness levels within a wide range of processed food formulations. Its compatibility with various flavors, sweeteners, proteins, and coloring agents allows manufacturers to maintain stable product formulations while achieving predictable sensory characteristics. The widespread use of food-grade maltodextrin as a carrier, bulking agent, and texture modifier continues to support its strong adoption in product reformulation efforts aimed at improving performance, optimizing production costs, and maintaining ingredient transparency.

North America Maltodextrin Market generated USD 1.5 billion in 2025. Demand in the region remains stable due to high consumption levels of processed food products, specialized nutrition formulations, and pharmaceutical applications. The United States plays a key role in regional growth as manufacturers increasingly focus on ingredient transparency and the development of clean-label formulations that align with changing consumer expectations. In addition, the presence of a highly developed food manufacturing sector and continuous demand for rapidly digestible carbohydrate ingredients support ongoing market expansion across the region.

Key companies operating in the Global Maltodextrin Market include Ingredion, Cargill, ADM, Tate & Lyle, and Roquette, along with several additional global and regional manufacturers. Companies operating in the Maltodextrin Market are focusing on strategic initiatives that strengthen their market position and support long-term growth. Leading manufacturers are investing in research and development to enhance ingredient functionality and develop improved processing techniques that meet evolving consumer expectations for transparency and quality. Many firms are also expanding their product portfolios by introducing maltodextrin variants derived from different raw materials to diversify supply options and address changing formulation requirements. Strategic collaborations with food and beverage manufacturers are helping companies expand application capabilities and accelerate product innovation. In addition, industry participants are strengthening their global distribution networks and improving production efficiency to maintain competitive pricing and ensure reliable supply.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Aircraft Platform

- 2.2.4 Component Type

- 2.2.5 Product Type

- 2.2.6 Manufacturing Process

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Corn-based

- 5.3 Wheat-based

- 5.4 Potato-based

- 5.5 Cassava-based

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Food grade

- 6.3 Pharmaceutical grade

- 6.4 Industrial grade

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.2.1 Baked goods

- 7.2.2 Confectionery

- 7.2.3 Dairy products

- 7.2.4 Beverages

- 7.2.5 Convenience foods

- 7.2.6 Others

- 7.3 Pharmaceuticals

- 7.3.1 Excipient in drug formulations

- 7.3.2 Nutritional supplements

- 7.4 Cosmetics and personal care

- 7.4.1 Skincare products

- 7.4.2 Haircare products

- 7.5 Industrial applications

- 7.5.1 Adhesives

- 7.5.2 Binders

- 7.5.3 Coating and encapsulation

- 7.6 Others

- 7.6.1 Animal feed

- 7.6.2 Fermentation processes

Chapter 8 Market Estimates and Forecast, By Dextrose Equivalent (DE) Range, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Low DE Maltodextrin

- 8.3 Mid DE Maltodextrin

- 8.4 High DE Maltodextrin

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 AGRANA Group

- 10.2 Archer Daniels Midland

- 10.3 Avebe

- 10.4 Cargill

- 10.5 Golden Grain Group

- 10.6 Grain Processing Corporation

- 10.7 Gulshan Polyols

- 10.8 Ingredion

- 10.9 Matsutani America

- 10.10 Mengzhou Tailijie

- 10.11 Roquette Freres

- 10.12 Tate & Lyle

- 10.13 Zhucheng Dongxiao Biotechnology