|

市場調查報告書

商品編碼

1998837

胰島素市場機會、成長要素、產業趨勢分析及2026-2035年預測Insulin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

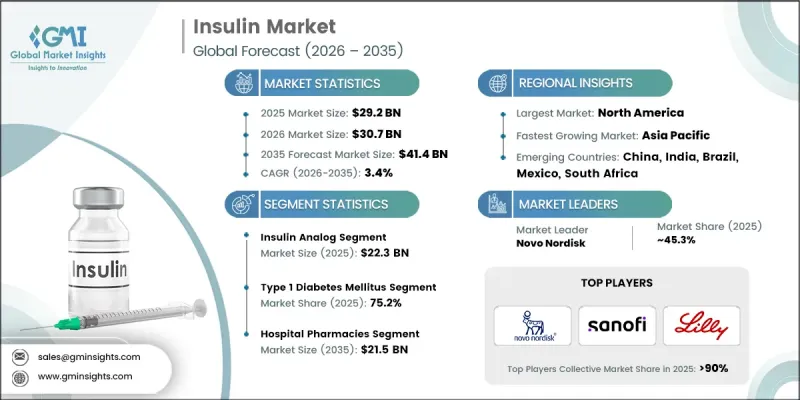

預計到 2025 年,全球胰島素市值將達到 292 億美元,並有望以 3.4% 的複合年成長率成長,到 2035 年達到 414 億美元。

全球胰島素市場的整體成長主要受糖尿病(尤其是第2型糖尿病)盛行率上升的驅動。 2型糖尿病與久坐的生活方式、肥胖率上升以及人口老化密切相關。此外,不良的飲食習慣、高熱量攝取、遺傳傾向以及生活方式相關的壓力等因素也導致了該疾病發生率的增加。胰島素是一種天然激素,在調節血糖值方面發揮重要作用。它是由胰臟中的特殊細胞產生,並在血糖值升高時分泌。這使得葡萄糖能夠被身體細胞吸收,並被用作能量或儲存起來以備後用。如果身體無法產生足夠的胰島素或對胰島素的反應不佳,血糖值就會升高,進而導致糖尿病。胰島素市場包含多種產品類型,包括速效、短效、中效、長效胰島素、預混合料製劑和生物相似藥。全球市場高度集中,少數幾家跨國製藥公司佔據了大部分的生產和技術研發佔有率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 292億美元 |

| 預計金額 | 414億美元 |

| 複合年成長率 | 3.4% |

預計到2025年,胰島素類似物市場規模將達223億美元。與傳統人類胰島素製劑相比,胰島素類比產品憑藉其更佳的臨床療效、更高的安全性以及更便捷的治療方式,保持著強勁的市場地位。這些治療方法因能降低血糖值劇烈波動的風險並提高患者的整體治療順從性而廣受認可。胰島素類似物還具有更大的給藥柔軟性,使患者能夠更方便地管理治療。給藥便捷和患者滿意度的提高促進了其廣泛應用。此外,某些長效胰島素類似物製劑能帶來更穩定的治療效果並減少治療相關併發症,進一步推動了市場需求。

到2025年,長效胰島素市佔率將達到45.3%。長效胰島素製劑旨在緩慢釋放胰島素,從而在較長時間內維持血液中基準水平的穩定。這種緩慢釋放是透過一種特殊的製劑機制實現的,該機制允許藥物在皮下注射後緩慢吸收。有些長效胰島素製劑能夠長期維持療效,進而減少患者所需的注射次數。這種持續作用有助於維持血糖穩定,同時降低血糖值快速波動的風險。因此,長效胰島素療法因其能夠提高治療依從性並提供更可預測的血糖管理而被廣泛採用。

預計到2025年,北美胰島素市佔率將達到40.1%。北美在胰島素產業的主導地位主要得益於糖尿病的高發生率以及全人群對胰島素治療的強勁需求。許多患者依賴胰島素來控制病情,確保了整個醫療保健系統對胰島素的穩定使用。先進的醫療基礎設施、強大的診斷能力以及最新胰島素製劑和給藥技術的廣泛應用,進一步鞏固了北美的市場主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 糖尿病盛行率上升

- 胰島素輸送系統的進展

- 政府措施和政策

- 產業潛在風險與挑戰

- 胰島素高成本

- 替代療法的可近性

- 市場機遇

- 關注兒童糖尿病

- 生物相似胰島素產品的擴張

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 價格分析(基於初步調查)

- 管道分析(基於初步調查)

- 糖尿病現狀

- 全球各地區糖尿病患者人數

- 2050年全球糖尿病患者人數最多的國家(2024年)

- 2024年全球糖尿病盛行率最高的國家

- 2024年全球糖尿病患者人數估計及至2050年的預測

- 預計2050年全球糖尿病患者人數最多的國家

- 糖尿病醫療保健支出排名前十的國家

- 區域細分:全球未確診糖尿病患者人數

- 各地區未確診糖尿病患者的百分比

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 人類胰島素

- 胰島素類似物

第6章 市場估算與預測:依產品分類,2022-2035年

- 速效胰島素

- 長效胰島素

- 配方胰島素

- 生物相似藥

- 其他產品

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 1型糖尿病

- 2型糖尿病

- 妊娠糖尿病

第8章 市場估算與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Adocia

- Biocon

- Boehringer Ingelheim International

- Eli Lilly and Company

- Gan & Lee Pharmaceuticals

- Gland Pharma

- Julphar

- MannKind Corporation

- Novo Nordisk

- Pfizer

- Sanofi

- Shanghai Fosun Pharmaceutical

- Tonghua Dongbao Pharmaceutical

- United Laboratories International

- Wockhardt

The Global Insulin Market was valued at USD 29.2 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 41.4 billion by 2035.

Growth across the insulin market is driven by the rising prevalence of diabetes worldwide, particularly type 2 diabetes, which is increasingly associated with sedentary lifestyles, increasing obesity levels, and an aging population. Additional factors such as poor dietary habits, higher caloric intake, genetic susceptibility, and lifestyle-related stress are also contributing to the growing incidence of the disease. Insulin is a naturally occurring hormone responsible for regulating glucose levels in the bloodstream. It is produced by specialized cells in the pancreas and released when blood sugar levels increase, enabling glucose to move into body cells where it is utilized for energy or stored for later use. When the body either fails to produce adequate insulin or cannot effectively respond to it, blood glucose levels rise, leading to diabetes. The insulin market includes multiple product categories such as rapid-acting, short-acting, intermediate-acting, long-acting, premixed insulin formulations, and biosimilar insulin products. The global market remains highly consolidated, with a limited number of multinational pharmaceutical companies accounting for a significant portion of production and technological development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $29.2 Billion |

| Forecast Value | $41.4 Billion |

| CAGR | 3.4% |

The insulin analog segment reached USD 22.3 billion in 2025. Insulin analog products maintain a strong position in the market because they offer improved clinical outcomes, enhanced safety profiles, and greater treatment convenience compared with conventional human insulin formulations. These therapies are widely recognized for reducing the risk of severe blood sugar fluctuations and improving overall treatment adherence. Insulin analogs also provide greater dosing flexibility, allowing patients to manage therapy more conveniently. Their ease of administration and improved patient satisfaction contribute to their widespread adoption. In addition, certain long-acting analog formulations are associated with more stable treatment outcomes and reduced treatment-related complications, which further supports their demand.

The long-acting insulin segment held a 45.3% share in 2025. Long-acting insulin formulations are designed to release insulin gradually, maintaining a consistent baseline level in the bloodstream over an extended duration. Their slow activity is achieved through formulation mechanisms that allow gradual absorption after subcutaneous injection. Some long-acting insulin products can remain effective for extended periods, which reduces the frequency of injections required for patients. This extended action helps maintain stable glucose control while lowering the risk of sudden fluctuations in blood sugar levels. As a result, long-acting insulin therapies are widely adopted because they improve treatment adherence and provide more predictable blood glucose management.

North America Insulin Market generated 40.1% share in 2025. The region's leadership within the insulin industry is strongly supported by the significant prevalence of diabetes and the high demand for insulin therapy across the population. Many patients rely on insulin to manage their condition, resulting in strong and consistent product utilization across healthcare systems. The presence of advanced medical infrastructure, strong diagnostic capabilities, and broad access to modern insulin formulations and delivery technologies further reinforces North America's leading market position.

Key companies operating in the Global Insulin Market include Novo Nordisk, Sanofi, Eli Lilly and Company, Pfizer, Biocon, Boehringer Ingelheim International, Adocia, Gan & Lee Pharmaceuticals, MannKind Corporation, Shanghai Fosun Pharmaceutical, Tonghua Dongbao Pharmaceutical, United Laboratories International, Julphar, Gland Pharma, and Wockhardt. Companies participating in the Global Insulin Market are implementing a range of strategic initiatives to strengthen their market position and maintain a competitive advantage. Major pharmaceutical firms are investing heavily in research and development to introduce advanced insulin formulations that offer improved efficacy, longer duration of action, and enhanced patient convenience. Strategic partnerships and licensing agreements with biotechnology firms are also helping companies accelerate innovation and expand product pipelines. Many manufacturers are focusing on the development of biosimilar insulin products to improve affordability and increase market penetration across emerging economies. In addition, firms are strengthening global distribution networks and expanding manufacturing capabilities to meet growing demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Product type trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes

- 3.2.1.2 Advancements in insulin delivery systems

- 3.2.1.3 Government initiatives and policies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of insulin

- 3.2.2.2 Availability of alternative therapies

- 3.2.3 Market opportunities

- 3.2.3.1 Focus on pediatric diabetes

- 3.2.3.2 Expansion of biosimilar insulin products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Pricing analysis (Driven by primary research)

- 3.6 Pipeline analysis (Driven by primary research)

- 3.7 Diabetes landscape

- 3.7.1 Number of diabetics worldwide, by region

- 3.7.2 Countries with the highest number of diabetics worldwide in 2024

- 3.7.3 Countries with the highest prevalence of diabetes worldwide in 2024

- 3.7.4 Estimated number of diabetics worldwide in 2024 and a forecast for 2050

- 3.7.5 Countries with the highest projected number of diabetics worldwide in 2050

- 3.7.6 Top 10 countries based on diabetes health expenditure

- 3.7.7 Global undiagnosed diabetes cases, by region

- 3.7.8 Percentage of diabetics undiagnosed, by regions

- 3.8 Impact of AI and generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Human insulin

- 5.3 Insulin analog

Chapter 6 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Rapid-acting insulin

- 6.3 Long-acting insulin

- 6.4 Combination insulin

- 6.5 Biosimilar

- 6.6 Other products

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Type 1 diabetes mellitus

- 7.3 Type 2 diabetes mellitus

- 7.4 Gestational diabetes

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Adocia

- 10.2 Biocon

- 10.3 Boehringer Ingelheim International

- 10.4 Eli Lilly and Company

- 10.5 Gan & Lee Pharmaceuticals

- 10.6 Gland Pharma

- 10.7 Julphar

- 10.8 MannKind Corporation

- 10.9 Novo Nordisk

- 10.10 Pfizer

- 10.11 Sanofi

- 10.12 Shanghai Fosun Pharmaceutical

- 10.13 Tonghua Dongbao Pharmaceutical

- 10.14 United Laboratories International

- 10.15 Wockhardt

緩釋皮下胰島素輸注市場:依產品類型、胰島素類型、年齡層及最終用戶分類-2026年至2032年全球市場預測胰島素市場:2026-2032年全球市場預測(依產品類型、胰島素種類、給藥途徑、最終用戶及通路分類)

緩釋皮下胰島素輸注市場:依產品類型、胰島素類型、年齡層及最終用戶分類-2026年至2032年全球市場預測胰島素市場:2026-2032年全球市場預測(依產品類型、胰島素種類、給藥途徑、最終用戶及通路分類) 重組人胰島素市場:依產品類型、品牌名稱、通路及地區分類

重組人胰島素市場:依產品類型、品牌名稱、通路及地區分類 口服胰島素市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按劑型、胰島素類型、地區和競爭格局分類,2021-2031年)葡萄糖凝膠市場按口味、分銷管道、包裝類型、應用和最終用戶分類-2026-2032年全球預測非侵入性胰島素市場按技術、應用、最終用戶和分銷管道分類-2026-2032年全球預測

口服胰島素市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按劑型、胰島素類型、地區和競爭格局分類,2021-2031年)葡萄糖凝膠市場按口味、分銷管道、包裝類型、應用和最終用戶分類-2026-2032年全球預測非侵入性胰島素市場按技術、應用、最終用戶和分銷管道分類-2026-2032年全球預測 胰島素市場規模、佔有率和成長分析(按產品類型、給藥裝置、類型、應用、分銷管道和地區分類):產業預測(2026-2033 年)

胰島素市場規模、佔有率和成長分析(按產品類型、給藥裝置、類型、應用、分銷管道和地區分類):產業預測(2026-2033 年) 全球重組細胞培養胰島素市場:市場規模、佔有率、趨勢分析(按類型、最終用途和地區分類)、細分市場預測(2025-2033 年)

全球重組細胞培養胰島素市場:市場規模、佔有率、趨勢分析(按類型、最終用途和地區分類)、細分市場預測(2025-2033 年) 胰島素原料藥(API)-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

胰島素原料藥(API)-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 日本胰島素藥物傳輸設備市場報告(按類型(藥物、設備)和地區)2025-2033

日本胰島素藥物傳輸設備市場報告(按類型(藥物、設備)和地區)2025-2033