|

市場調查報告書

商品編碼

1998816

安瓿包裝市場機會、成長要素、產業趨勢分析及2026-2035年預測Ampoules Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

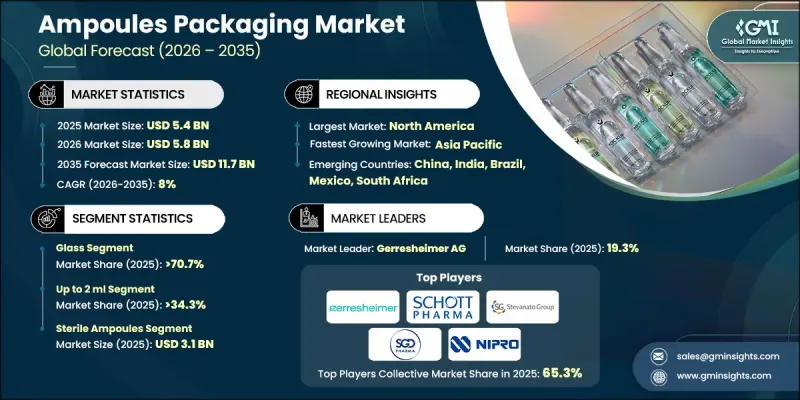

2025年全球安瓿包裝市場價值為54億美元,預計到2035年將以8%的複合年成長率成長至117億美元。

市場擴張主要得益於製藥業的持續成長,尤其是注射劑產量的不斷提高。隨著對無菌給藥系統的需求持續成長,製藥公司正優先考慮可靠的初級包裝,以確保產品的完整性和安全性。安瓿瓶主要由玻璃或精心挑選的替代材料製成,因其能夠保護敏感配方免受環境影響,同時保持無菌性和穩定性而被廣泛應用。已開發市場和新興市場製藥生產設施的持續擴張,推動了對高品質、防污染包裝的需求。監管力度的加強和品質保證標準的日益嚴格,進一步促進了安全、防篡改解決方案的應用。此外,先進治療方法的不斷發展,也提升了能夠在整個儲存和分銷過程中保護複雜配方的包裝系統的重要性。所有這些因素共同推動安瓿瓶包裝市場走上強勁、永續的長期成長軌道。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 54億美元 |

| 預測金額 | 117億美元 |

| 複合年成長率 | 8% |

慢性病發病率的上升加速了對腸外給藥系統的需求,這也是推動產業成長的主要動力。注射藥物通常以單劑量安瓿包裝,以確保劑量精準並提高病人安全性。隨著治療場所擴展到醫院、專科醫療中心和居家醫療機構,對緊湊、安全且易於使用的包裝解決方案的需求日益成長,進一步促進了安瓿在全球範圍內的應用。

到2025年,玻璃將佔據70.7%的市場佔有率,成為領先的材料類別。其優點源自於其化學惰性、優異的阻隔性,以及對USP <660>和歐盟GMP等監管標準的良好符合性。玻璃是製藥應用領域的首選材料,因為它能有效維持藥物製劑的無菌性和穩定性。同時,為了滿足環境目標和監管要求,製造商正增加對永續替代材料(例如可回收玻璃和可生物分解材料)的研發投入。

預計2026年至2035年間,6毫升至10毫升容量規格的注射市場將以9.3%的複合年成長率成長。此細分市場的成長主要受對需要更大容量和更精確劑量的先進注射療法的需求不斷成長的驅動。在臨床環境中,多劑量安瓿有助於提高連續治療通訊協定的操作效率。為了順應這一趨勢,製造商正在投資高精度模具技術,旨在確保密封性並最大限度地降低污染風險。

預計到2025年,北美安瓿包裝市佔率將達到32%。這一成長主要得益於先進的醫療基礎設施、注射和生物製藥研發領域的大量投資以及不斷成長的醫療支出。在該地區營運的公司正優先考慮遵守FDA cGMP標準、加強供應鏈能力,並致力於生物製藥包裝領域的創新,以確保獲得研發資金。此外,在注重成本的醫療環境中,對自動化生產系統和永續玻璃回收專案的投資也有助於降低營運成本。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大注射劑產品組合

- 生物製藥和特殊藥物的成長

- 擴大全球免疫和疫苗接種計劃

- 監管機構越來越重視無菌性和藥品安全性。

- 新興市場非專利注射劑生產規模的擴大

- 產業潛在風險與挑戰

- 損壞風險與應對挑戰

- 向替代包裝形式的過渡正在進行中。

- 市場機遇

- 安瓿設計與製造的技術進步

- 新興醫療基礎設施的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 歷史價格分析(2022-2024)

- 影響價格趨勢的因素

- 各地區價格波動

- 價格預測(2026-2035)

- 定價策略

- 新興經營模式

- 合規要求

- 專利分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依材料分類,2022-2035年

- ,

- 玻璃

- 塑膠

第6章 市場估計與預測:依產能分類,2022-2035年

- ,

- 2毫升或更少

- 3 ml~5 ml

- 6 ml~10 ml

- 超過10毫升

第7章 市場估算與預測:依製造技術分類,2022-2035年

- ,

- 泡棉填充密封(FFS)

- 吹灌封(BFS)

- 傳統灌裝和密封

第8章 市場估算與預測:依滅菌方法分類,2022-2035年

- 主要趨勢

- 無菌安瓿

- 非無菌安瓿

第9章 市場估計與預測:依頸型分類,2022-2035年

- ,

- 開放式漏斗(OPC - 單點切割)

- 封閉式漏斗

- 顏色斷裂環(CBR)

第10章 市場估價與預測:依最終用戶產業分類,2022-2035年

- 製藥

- 個人護理和化妝品

第11章 市場估價與預測:按地區分類,2022-2035年

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第12章:公司簡介

- ABB Ltd.

- Advantech Co., Ltd.

- Antaira Technologies

- B&R Industrial Automation

- Belden Inc.

- Bosch Rexroth AG

- Cisco Systems, Inc.

- Hirschmann Automation and Control

- HMS Networks AB

- Kyland Technology Co., Ltd.

- Moxa Technologies

- OMRON Corporation

- Perle Systems, Inc.

- Phoenix Contact GmbH &Co. KG

- Red Lion Controls, Inc.

- Rockwell Automation, Inc.

- Schneider Electric SE

- Siemens AG

- Weidmuller Interface GmbH &Co. KG

- Westermo Network Technologies

The Global Ampoules Packaging Market was valued at USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 11.7 billion by 2035.

Market expansion is fueled by sustained growth in the pharmaceutical sector, particularly the rising production of injectable formulations. As demand for sterile drug delivery systems continues to climb, pharmaceutical manufacturers are prioritizing reliable primary packaging that ensures product integrity and safety. Ampoules, produced primarily from glass and select alternative materials, are widely utilized due to their ability to safeguard sensitive formulations from environmental exposure while maintaining sterility and stability. Ongoing expansion of pharmaceutical manufacturing facilities across both developed and emerging economies is increasing the need for high-quality, contamination-resistant packaging formats. Heightened regulatory scrutiny and quality assurance standards are further encouraging the adoption of secure, tamper-evident solutions. Additionally, the continued development of advanced therapies is reinforcing the importance of packaging systems capable of preserving complex formulations throughout storage and distribution. These combined factors are positioning the ampoules packaging market for strong and sustained long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 8% |

The rising prevalence of chronic health conditions is accelerating the demand for parenteral drug delivery systems, which serves as a major industry growth catalyst. Injectable treatments are frequently supplied in single-dose ampoules to ensure dosing precision and enhance patient safety. Expanding treatment delivery across hospitals, specialized care centers, and home-based healthcare settings is increasing the need for compact, secure, and user-friendly packaging solutions, further strengthening ampoule adoption worldwide.

The glass segment accounts for 70.7% share in 2025, making it the leading material segment. Its dominance is attributed to chemical inertness, superior barrier properties against moisture and oxygen, and strong compliance with regulatory standards such as USP <660> and EU GMP requirements. Glass effectively preserves sterility and stability in sensitive drug formulations, making it the preferred material for pharmaceutical applications. At the same time, manufacturers are investing in research and development focused on sustainable alternatives, including recyclable glass and biodegradable materials, to align with environmental goals and regulatory expectations.

The 6 ml-10 ml capacity segment is anticipated to grow at a CAGR of 9.3% during 2026-2035. Growth in this segment is driven by increasing demand for advanced injectable therapies that require larger and precisely measured volumes. Multi-dose configurations in clinical settings contribute to improved operational efficiency in ongoing treatment protocols. To support this trend, manufacturers are allocating capital toward high-precision mold technologies designed to produce secure seals and minimize contamination risks.

North America Ampoules Packaging Market held a 32% share in 2025. Regional growth is supported by advanced healthcare infrastructure, significant investment in injectable and biologics development, and rising healthcare expenditure. Companies operating in this region are emphasizing compliance with FDA cGMP standards, strengthening supply chain capabilities, and pursuing innovation in biologics packaging to secure research funding opportunities. Investments in automated manufacturing systems and sustainable glass recycling initiatives are also helping reduce operational costs within an increasingly cost-sensitive healthcare environment.

Prominent companies active in the Global Ampoules Packaging Market include Gerresheimer AG, SCHOTT Pharma, Stevanato Group, SGD Pharma, Nipro Corporation, DWK Life Sciences, Shandong Pharmaceutical Glass Co. Ltd, Adelphi Healthcare Packaging, James Alexander Corporation, Borosil, ESSCO Glass, Alphial S.r.l., Kapoor Glass India Pvt. Ltd., NAFVSM B.V., Namicos Corporation, PG Pharma, Sandfire Scientific Ltd., SFAM, SHIOTANI GLASS CO., LTD., TA Instruments, and AAPL Solutions. Companies in the Global Ampoules Packaging Market are reinforcing their market position through technological advancement, regulatory alignment, and strategic capacity expansion. Leading players are investing in automated production lines and precision molding systems to enhance product consistency and contamination control. Research and development initiatives are focused on high-performance glass compositions and sustainable packaging materials that meet evolving environmental standards. Strategic collaborations with pharmaceutical manufacturers are strengthening long-term supply agreements and improving distribution reach. Firms are also expanding geographically to access high-growth emerging markets while optimizing supply chain resilience.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Capacity trends

- 2.2.3 Manufacturing technology trends

- 2.2.4 Sterility type trends

- 2.2.5 Neck Type trends

- 2.2.6 End-user industry trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Injectable Drug Portfolio

- 3.2.1.2 Growth in Biologics and Specialty Pharmaceuticals

- 3.2.1.3 Rising Global Immunization and Vaccination Programs

- 3.2.1.4 Increasing Regulatory Focus on Sterility and Drug Safety

- 3.2.1.5 Expansion of Generic Injectable Manufacturing in Emerging Markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of Breakage and Handling Challenges

- 3.2.2.2 Growing Shift Toward Alternative Packaging Formats

- 3.2.3 Market opportunities

- 3.2.3.1 Technological Advancements in Ampoule Design and Manufacturing

- 3.2.3.2 Expansion in Emerging Healthcare Infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends,

- 5.2 Glass

- 5.3 Plastic

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035 (USD Million)

- 6.1 Key trends,

- 6.2 Up to 2 ml

- 6.3 3 ml - 5 ml

- 6.4 6 ml - 10 ml

- 6.5 Above 10 ml

Chapter 7 Market Estimates & Forecast, By Manufacturing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends,

- 7.2 Form-fill-seal (ffs)

- 7.3 Blow-fill-seal (bfs)

- 7.4 Conventional filling & sealing

Chapter 8 Market Estimates & Forecast, By Sterility Type, 2022 - 2035 (USD Million)

- 8.1 key trends,

- 8.2 sterile ampoules

- 8.3 non-sterile ampoules

Chapter 9 Market Estimates & Forecast, By Neck Type, 2022 - 2035 (USD Million)

- 9.1 Key trends,

- 9.2 Open funnel (OPC - One Point Cut)

- 9.3 Closed funnel

- 9.4 Color break ring (CBR)

Chapter 10 Market Estimates & Forecast, By End-user Industry, 2022 - 2035 (USD Million)

- 10.1 Pharmaceutical

- 10.2 Personal care and cosmetic

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends, by region

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia-Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 ABB Ltd.

- 12.2 Advantech Co., Ltd.

- 12.3 Antaira Technologies

- 12.4 B&R Industrial Automation

- 12.5 Belden Inc.

- 12.6 Bosch Rexroth AG

- 12.7 Cisco Systems, Inc.

- 12.8 Hirschmann Automation and Control

- 12.9 HMS Networks AB

- 12.10 Kyland Technology Co., Ltd.

- 12.11 Moxa Technologies

- 12.12 OMRON Corporation

- 12.13 Perle Systems, Inc.

- 12.14 Phoenix Contact GmbH & Co. KG

- 12.15 Red Lion Controls, Inc.

- 12.16 Rockwell Automation, Inc.

- 12.17 Schneider Electric SE

- 12.18 Siemens AG

- 12.19 Weidmuller Interface GmbH & Co. KG

- 12.20 Westermo Network Technologies

安瓿包裝市場規模、佔有率和成長分析:按材料、產品類型、產能、終端用戶產業、無菌加工方法、銷售管道和地區分類-2026-2033年產業預測

安瓿包裝市場規模、佔有率和成長分析:按材料、產品類型、產能、終端用戶產業、無菌加工方法、銷售管道和地區分類-2026-2033年產業預測 安瓿包裝市場:按產品類型、材料、包裝技術、無菌性、應用和最終用戶分類-2026-2032年全球預測

安瓿包裝市場:按產品類型、材料、包裝技術、無菌性、應用和最終用戶分類-2026-2032年全球預測 安瓿包裝:市佔率分析、產業趨勢、統計、成長預測(2025-2030)

安瓿包裝:市佔率分析、產業趨勢、統計、成長預測(2025-2030) 全球塑膠安瓿瓶市場中東和非洲的安瓿包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美安瓿包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國安瓿包裝:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)

全球塑膠安瓿瓶市場中東和非洲的安瓿包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美安瓿包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)美國安瓿包裝:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)