|

市場調查報告書

商品編碼

1998808

2026 年至 2035 年飼料益生菌市場的商業機會、成長要素、產業趨勢分析與預測。Animal Feed Probiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

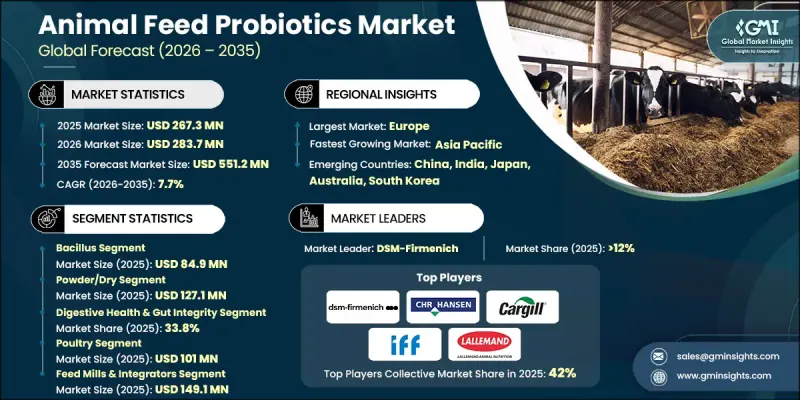

預計到 2025 年,全球動物飼料益生菌市場價值將達到 2.673 億美元,年複合成長率為 7.7%,到 2035 年將達到 5.512 億美元。

飼料益生菌市場的成長與鼓勵無抗生素畜牧養殖系統的監管政策的推進密切相關。隨著對飼料和飲用水中常規使用動物抗生素的監管日益嚴格,生產者擴大採用以營養改善和生物解決方案為重點的替代性健康管理策略。因此,益生菌作為維持牲畜腸道菌叢平衡的重要添加劑,正獲得廣泛認可。鑑於全球飼料生產規模龐大,即使益生菌添加劑的採用率不高,也可能帶來顯著的市場成長。除了監管影響外,業界也意識到補充益生菌帶來的持續性能提升。針對不同畜種的大量飼餵試驗表明,益生菌能夠顯著改善動物健康、生長性能和成本效益。這些結果有助於提高生長速度、降低疾病發生率和改善產品質量,使益生菌成為畜牧預防性健康管理的關鍵要素。此外,對永續性的關注也在推動市場需求,因為益生菌有助於提高營養利用效率並減少對環境的影響。隨著精準飼餵技術的不斷發展和更有效的功效數據的出現,隨著生產商響應不斷成長的全球食品需求和不斷變化的監管標準,動物飼料益生菌市場預計將保持長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2.673億美元 |

| 預測金額 | 5.512億美元 |

| 複合年成長率 | 7.7% |

預計到2025年,芽孢桿菌市場規模將達到8,490萬美元,成為飼料配方中最廣泛應用的益生菌類別之一。芽孢桿菌益生菌因其耐高溫和形成持久孢子的能力而備受推崇,即使在高溫脅迫的飼料加工和儲存條件下也能保持穩定。其生物活性有助於維持消化平衡,並幫助牲畜在生理壓力時期保持穩定的腸道環境。此外,這些益生菌還能產生有益酶,改善營養物質的消化吸收,這也是它們在各種畜牧養殖計畫中廣泛應用的重要因素。

到2025年,專注於消化健康和腸道健康的細分市場將佔據33.8%的市場。維持腸道菌叢平衡仍是將益生菌納入動物營養方案的主要原因之一。健康的消化器官系統能夠幫助牲畜更有效地吸收營養,同時穩定消化道內的微生物平衡。這些益處在早期生長階段和飼料轉換期尤其重要,因為此時動物更容易出現消化器官系統問題,對整體生產力產生負面影響。因此,專注於消化健康的益生菌解決方案仍然是市場上的主要應用領域。

預計2035年,北美動物飼料益生菌市場規模將達到1.047億美元。北美正崛起為關鍵成長區域,這得益於其高度發達的畜牧系統、清晰的法規結構以及業界對無抗生素飼養方式日益成長的興趣。該地區對精準營養策略和永續畜牧業的高度重視,為先進益生菌技術的應用創造了有利條件。益生菌配方和輸送系統的持續創新,進一步推動了全部區域市場的擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 科學證據支持的性能提升

- 管理職責和貿易要求

- 精密農業與穩定技術

- 產業潛在風險與挑戰

- 菌株多樣性和劑量

- 法規的複雜性

- 市場機遇

- 甲烷與營養管理

- 水產養殖與寵物營養

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 芽孢桿菌

- 乳酸桿菌

- 釀酒酵母(源自酵母)

- 雙歧桿菌

- 腸球菌

- 後生元

- 鏈球菌

- 其他

第6章 市場估計與預測:依類型分類,2022-2035年

- 粉末/乾粉

- 微膠囊化

- 液體/水溶性

- 顆粒

- 其他

第7章 市場估計與預測:依功能分類,2022-2035年

- 消化系統健康和腸道健康

- 免疫支持與調節

- 促進生長和飼料效率

- 病原體控制和競爭性消除

- 壓力管理

- 其他

第8章 市場估算與預測:依畜牧業分類,2022-2035年

- 家禽

- 肉雞

- 產蛋母雞

- 種苗

- 其他

- 豬

- 仔豬(斷奶前和斷奶後)

- 發展期

- 肥育豬

- 其他

- 牛(反芻動物)

- 牛

- 牛

- 水產養殖

- 鮭魚

- 鱒魚

- 蝦

- 鯉魚

- 其他

- 寵物食品

- 狗

- 貓

- 馬

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 飼料廠及綜合企業

- 獸藥批發商

- 直接銷售(從生產商到農場)

- 線上/電子商務

- 其他

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- 商業和工業農場

- 小規模家庭花園

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第12章:公司簡介

- DSM-Firmenich

- Chr. Hansen(Novonesis)

- Cargill Animal Nutrition

- IFF

- Lallemand Animal Nutrition

- Alltech

- Kemin Industries

- Evonik Industries

- Novus International

- Lesaffre Group

- Angel Yeast

- Biomin

- Nutreco

- MicroSynbiotiX

The Global Animal Feed Probiotics Market was valued at USD 267.3 million in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 551.2 million by 2035.

Growth in the animal feed probiotics market is linked to evolving regulatory policies that encourage antibiotic-free livestock production systems. Increasing restrictions on the routine use of veterinary antibiotics in feed and water have encouraged producers to adopt alternative health management strategies that focus on improved nutrition and biological solutions. As a result, probiotics are gaining widespread recognition as valuable additives that support a balanced gut microbiome in livestock. The massive scale of global feed production means that even modest adoption rates of probiotic additives can translate into substantial market growth. In addition to regulatory influences, the industry is also recognizing the consistent performance advantages associated with probiotic supplementation. Numerous feeding trials across different livestock categories have demonstrated measurable improvements in animal health, growth performance, and cost efficiency. These outcomes contribute to stronger growth rates, lower disease incidence, and improved product quality, positioning probiotics as a key element in preventive livestock health management. Sustainability considerations are also reinforcing market demand, as probiotics support improved nutrient utilization and reduced environmental impact. With the continued development of precision feeding technologies and the availability of stronger efficacy data, the animal feed probiotics market is expected to maintain long-term growth as producers respond to rising global food demand and evolving regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $267.3 Million |

| Forecast Value | $551.2 Million |

| CAGR | 7.7% |

The bacillus segment generated USD 84.9 million in 2025 and represents one of the most widely adopted probiotic categories used in feed formulations. Bacillus-based probiotics are particularly valued for their ability to withstand high temperatures and form durable spores, allowing them to remain stable during feed processing and storage conditions that involve thermal stress. Their biological activity supports digestive balance and helps maintain gut stability during periods of physiological stress in livestock. Additionally, these probiotics are known to produce beneficial enzymes that improve nutrient digestion, which has contributed to their strong presence across several animal production programs.

The digestive health and gut integrity segment accounted for 33.8% share in 2025. Maintaining a balanced intestinal environment remains one of the primary reasons for incorporating probiotics into animal nutrition programs. Healthy digestive systems allow livestock to absorb nutrients more efficiently while maintaining a stable microbial balance in the gastrointestinal tract. These benefits are particularly valuable during early growth stages and during dietary transitions, when animals are more vulnerable to digestive disturbances that can negatively affect overall performance. As a result, probiotic solutions focused on digestive health continue to represent a major application area within the market.

North America Animal Feed Probiotics Market is projected to reach USD 104.7 million by 2035. North America has emerged as an important growth region due to its highly developed livestock production systems, well-defined regulatory frameworks, and increasing industry emphasis on antibiotic-free feeding practices. The region's strong focus on precision nutrition strategies and sustainable livestock production has created favorable conditions for the adoption of advanced probiotic technologies. Continued innovation in probiotic formulations and delivery systems is further supporting the market's expansion across the region.

Major companies operating in the Global Animal Feed Probiotics Market include Cargill Animal Nutrition, DSM-Firmenich, Chr. Hansen (Novonesis), IFF, Lallemand Animal Nutrition, Alltech, Kemin Industries, Evonik Industries, Novus International, Lesaffre Group, Angel Yeast, Nutreco, Biomin, and MicroSynbiotiX. Companies operating in the Global Animal Feed Probiotics Market are strengthening their market position through innovation, strategic partnerships, and expansion of research capabilities. Many firms are investing heavily in microbiome research to develop advanced probiotic strains that deliver improved performance and stability in animal feed applications. Strategic collaborations with feed manufacturers and livestock producers help companies integrate probiotic solutions into large-scale nutrition programs. Businesses are also focusing on expanding production capacity and improving formulation technologies to enhance product stability during feed processing. Additionally, organizations are increasing their presence in emerging livestock markets while strengthening distribution networks worldwide. Continuous investment in scientific validation, field trials, and regulatory approvals further supports product credibility and helps companies build stronger relationships with producers seeking reliable alternatives to antibiotic-based growth promoters.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Function

- 2.2.5 Livestock

- 2.2.6 Distribution Channel

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Science-backed performance gains

- 3.2.1.2 Stewardship and trade requirements

- 3.2.1.3 Precision farming & stability tech

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Strain variability & dosing

- 3.2.2.2 Regulatory complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Methane and nutrient management

- 3.2.3.2 Aquaculture and pet nutrition.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bacillus

- 5.3 Lactobacilli

- 5.4 Saccharomyces (Yeast-Based)

- 5.5 Bifidobacterium

- 5.6 Enterococcus

- 5.7 Postbiotics

- 5.8 Streptococcus

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder/Dry

- 6.3 Microencapsulated

- 6.4 Liquid/Soluble

- 6.5 Granules

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Function, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Digestive health & gut integrity

- 7.3 Immune support & modulation

- 7.4 Growth promotion & feed efficiency

- 7.5 Pathogen control & competitive exclusion

- 7.6 Stress management

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Poultry

- 8.2.1 Broilers

- 8.2.2 Layers

- 8.2.3 Breeders

- 8.2.4 Others

- 8.3 Swine

- 8.3.1 Piglets (pre-weaning & post-weaning)

- 8.3.2 Growers

- 8.3.3 Finishers

- 8.3.4 Others

- 8.4 Cattle (ruminants)

- 8.4.1 Dairy cattle

- 8.4.2 Beef cattle

- 8.5 Aquaculture

- 8.5.1 Salmon

- 8.5.2 Trout

- 8.5.3 Shrimp

- 8.5.4 Carp

- 8.5.5 Others

- 8.6 Pet food

- 8.6.1 Dogs

- 8.6.2 Cats

- 8.7 Equine

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Feed mills & integrators

- 9.3 Veterinary distributors

- 9.4 Direct sales (manufacturer to farm)

- 9.5 Online/e-commerce

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End-User, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Commercial/industrial farms

- 10.3 Small-scale/backyard operations

- 10.4 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 DSM-Firmenich

- 12.2 Chr. Hansen (Novonesis)

- 12.3 Cargill Animal Nutrition

- 12.4 IFF

- 12.5 Lallemand Animal Nutrition

- 12.6 Alltech

- 12.7 Kemin Industries

- 12.8 Evonik Industries

- 12.9 Novus International

- 12.10 Lesaffre Group

- 12.11 Angel Yeast

- 12.12 Biomin

- 12.13 Nutreco

- 12.14 MicroSynbiotiX

益生菌和益生元飲料市場預測至2034年—按產品類型、成分類型、功能、分銷管道和最終用戶分類的全球分析

益生菌和益生元飲料市場預測至2034年—按產品類型、成分類型、功能、分銷管道和最終用戶分類的全球分析 2026-2034年全球動物飼料益生菌市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球動物飼料益生菌市場規模、佔有率、趨勢和成長分析報告 動物飼料益生菌市場-全球產業規模、佔有率、趨勢、機會和預測:按動物種類、原料、劑型、分銷管道、地區和競爭格局分類,2021-2031年

動物飼料益生菌市場-全球產業規模、佔有率、趨勢、機會和預測:按動物種類、原料、劑型、分銷管道、地區和競爭格局分類,2021-2031年 動物飼料益生菌市場規模、佔有率和成長分析(按動物種類、市場來源、劑型、通路、功能和地區分類)-2026-2033年產業預測

動物飼料益生菌市場規模、佔有率和成長分析(按動物種類、市場來源、劑型、通路、功能和地區分類)-2026-2033年產業預測 動物飼料益生菌市場規模、佔有率和成長分析(按形態、來源、動物種類和地區分類)—產業預測(2026-2033 年)全球精準益生菌市場:預測至2032年-按產品類型、劑型、通路、應用、最終用戶和地區分類的分析

動物飼料益生菌市場規模、佔有率和成長分析(按形態、來源、動物種類和地區分類)—產業預測(2026-2033 年)全球精準益生菌市場:預測至2032年-按產品類型、劑型、通路、應用、最終用戶和地區分類的分析 動物飼料益生菌市場:全球按產地、牲畜、形態、菌株、功能、分銷管道和地區分類 - 預測至 2030 年

動物飼料益生菌市場:全球按產地、牲畜、形態、菌株、功能、分銷管道和地區分類 - 預測至 2030 年 食品、飲料、營養補充品和飼料中的益生菌

食品、飲料、營養補充品和飼料中的益生菌