|

市場調查報告書

商品編碼

1998787

高性能車輪市場商機、成長要素、產業趨勢分析及2026-2035年預測。High Performance Wheels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

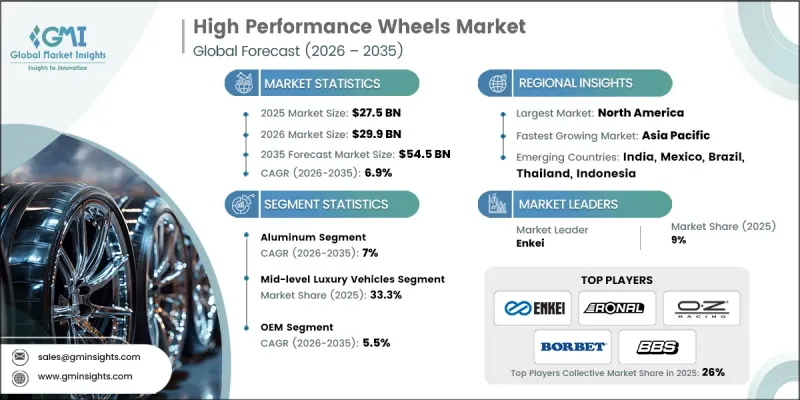

預計到 2025 年,全球高性能車輪市場價值將達到 275 億美元,並有望以 6.9% 的複合年成長率成長,到 2035 年達到 545 億美元。

高性能輪轂產業的成長主要得益於市場對輕量化汽車零件日益成長的需求,這些零件能夠提升效率和駕駛性能。汽車製造商正廣泛採用鍛造鋁和碳纖維等先進材料來減輕車身重量、提高耐用性並提升燃油效率。輕量化輪轂技術在降低排放氣體和提升現代汽車平台的車輛性能方面發揮著至關重要的作用。此外,隨著電動車的普及,對空氣動力學性能更優、能效更高、能夠降低滾動阻力並延長電池續航里程的輪轂設計的需求也在加速成長。豪華車和高性能汽車製造商擴大在其車型中採用更大直徑的合金輪轂和鍛造輪圈,以提升操控性、煞車性能和整體美觀度。人們對賽車運動、性能提升和個人化改裝文化的日益濃厚的興趣也推動了售後市場的強勁需求。這些因素共同推動全球汽車生態系統在輪圈設計、材料工程和製造技術方面的持續創新。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 275億美元 |

| 預測金額 | 545億美元 |

| 複合年成長率 | 6.9% |

複合年成長率 (CAGR) 指的是年均複合成長率,預計到 2025 年,鋁製輪圈市佔率將達到 60%,並在 2026 年至 2035 年間以 7% 的複合年成長率成長。鋁合金因其在強度、輕量化、耐腐蝕性和製造成本方面的優異平衡而成為首選材料。鋁製輪圈在 OEM(原始設備製造商)生產中的應用日益廣泛,尤其是在電動車和豪華車領域,這進一步推動了該細分市場的成長。諸如旋壓成型和鍛造等先進製造技術使製造商能夠生產出結構剛性更強、行駛穩定性更高的輕量化輪轂。這些技術還有助於提高散熱性能和耐久性,這對於高性能汽車應用至關重要。

預計到2025年,中檔豪華車市佔率將達到33.3%,並在2026年至2035年間以7.9%的複合年成長率成長。該細分市場的車輛正擴大採用兼具美觀性和性能的輪轂。汽車製造商正在推出包含輕量化高性能輪轂的選配包,旨在提升車輛的加速、煞車和抓地力。消費者對兼具時尚外觀和卓越性能的車輛的需求持續成長,促使汽車製造商將高階輪轂技術融入其中檔豪華車型。此外,採用先進的輪轂製造程序,使品牌能夠在保持成本效益和結構強度的同時,提供視覺效果驚人的輪轂設計。

預計到2025年,美國高性能輪圈市場規模將達到81億美元。美國豪華車和高性能車市場的強勁表現,為汽車製造商整合先進輪轂技術創造了巨大機會。在美國市場運營的汽車品牌正日益關注鍛造輪圈和空氣動力學最佳化設計的輪轂,以滿足消費者對性能、駕駛舒適性和視覺吸引力的不斷提升的需求。大直徑高階輪轂,尤其是在小眾車型領域,日益受到歡迎,推動了高價值輪轂產品需求的成長。此外,消費者對車輛客製化和性能提升的日益濃厚的興趣也持續刺激著售後市場的發展,從而支撐了整個市場的擴張。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對輕型車輛的需求日益成長

- 高階和豪華汽車銷售成長

- 賽車運動產業的擴張

- 售後市場的客製化趨勢

- 產業潛在風險與挑戰

- 高昂的製造成本

- 原物料價格波動

- 市場機遇

- 拓展OEM夥伴關係

- 不斷成長的電動車售後市場

- 混合鍛造技術的進步

- 新興汽車市場

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 加拿大運輸部車輛安全標準(CMVSS)

- 歐洲

- 歐洲車輛類型認證(WVTA)

- 歐洲經濟共同體法規 124 (R124)

- 亞太地區

- 日本汽車標準協會(JASO)

- AIS(汽車產業標準)- 印度

- 拉丁美洲

- 巴西國家交通運輸委員會(CONTRAN)-第242號決議

- 墨西哥 NOM 標準 (Normas Oficiales Mexicanas)

- 中東和非洲

- 阿拉伯聯合大公國計量與標準化局(ESMA)

- 南非標準局(SABS)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 生產統計

- 生產基地

- 消費中心

- 出口和進口

- 成本細分分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 專利分析(基於初步研究)

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、局限性和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 設備運轉率和擴建計劃

- 品質標準和測試通訊協定

- 國際品質認證標準(ISO、TUV、JWL)

- 性能測試和調查方法

- 安全性和耐久性要求

- 識別和預防仿冒品

- 消費者行為與購買模式分析

- 購買決策因素

- 品牌忠誠度與轉換行為

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依材料分類,2022-2035年

- 鋁

- 鎂

- 鋼

- 碳纖維

第6章 市場估價與預測:依車輛類型分類,2022-2035年

- 入門性能車

- 中檔豪華車

- 頂級豪華轎車

- 超級跑車和頂級跑車

- 高性能SUV和跨界車

- 賽車運動

第7章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第8章 市場估算與預測:依通路分類,2022-2035年

- 離線頻道

- 線上管道

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- BBS Motorsport

- Borbet

- Carbon Revolution

- Enkei

- HRE Performance Wheels

- OZ Racing

- Rays Engineering/Volk Racing

- Ronal

- Vossen

- Work Wheels

- 本地製造商

- Advan Racing/Yokohama

- BC Forged

- Dymag

- Forgeline

- Speedline Corse

- SSR Wheels

- TSW Alloy Wheels

- Weds Sport

- 新興企業

- Cosmis Wheels

- Fifteen52

- Rotiform

- Titan7

The Global High Performance Wheels Market was valued at USD 27.5 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 54.5 billion by 2035.

Growth in the high performance wheels industry is strongly influenced by increasing demand for lightweight automotive components that improve efficiency and driving dynamics. Automotive manufacturers are widely adopting advanced materials such as forged aluminum and carbon fiber to reduce vehicle weight, enhance durability, and support improved fuel efficiency. Lightweight wheel technologies also play a crucial role in reducing emissions and improving vehicle performance across modern automotive platforms. In addition, the rising adoption of electric vehicles is accelerating the demand for aerodynamic and energy-efficient wheel designs that reduce rolling resistance and extend battery range. Premium and performance vehicle manufacturers are increasingly equipping their models with larger-diameter alloy and forged wheels to enhance handling, braking performance, and overall aesthetics. Growing interest in motorsports, performance upgrades, and customization culture is also fueling strong demand in the aftermarket segment. These factors collectively continue to drive innovation in wheel design, materials engineering, and manufacturing technologies across the global automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.5 Billion |

| Forecast Value | $54.5 Billion |

| CAGR | 6.9% |

The aluminum wheels segment held a 60% share in 2025 and is expected to grow at a CAGR of 7% between 2026 and 2035. Aluminum alloys remain the preferred material because they provide an optimal balance between strength, lightweight construction, corrosion resistance, and manufacturing cost. The increasing integration of aluminum wheels in original equipment manufacturing, particularly in electric vehicles and premium passenger vehicles, is further strengthening segment growth. Advanced manufacturing techniques such as flow-forming and forging enable manufacturers to produce lightweight wheels that deliver improved structural rigidity and enhanced driving stability. These technologies also support improved heat dissipation and durability, which are essential for high-performance automotive applications.

The mid-level luxury vehicle segment accounted for 33.3% share in 2025 and is expected to grow at a CAGR of 7.9% from 2026 to 2035. Vehicles within this category are increasingly equipped with performance-oriented wheels that combine aesthetic appeal with improved vehicle dynamics. Automotive manufacturers are introducing optional packages that include lightweight performance wheels designed to enhance acceleration, braking, and road grip. Consumer demand for vehicles that deliver both style and performance continues to grow, encouraging automakers to integrate premium wheel technologies into mid-tier luxury models. The adoption of advanced wheel manufacturing processes also enables brands to offer visually distinctive designs while maintaining cost efficiency and structural strength.

U.S. High Performance Wheels Market reached USD 8.1 billion in 2025. The strong presence of luxury and performance vehicles in the country creates significant opportunities for original equipment manufacturers to integrate advanced wheel technologies. Automotive brands operating in the U.S. market are increasingly focusing on forged and aerodynamically optimized wheel designs to meet rising consumer expectations for performance, ride comfort, and visual appeal. The growing popularity of large-diameter premium wheels, particularly in specialized vehicle segments, is contributing to higher demand for high-value wheel products. In addition, increasing consumer interest in vehicle customization and performance enhancement continues to stimulate the aftermarket segment, supporting overall market expansion.

Key players in the Global High Performance Wheels Market include BBS, Borbet, Carbon Rev, Enkei, HRE, OZ Racing, Rays, Ronal, Vossen, and Work. Companies operating in the Global High Performance Wheels Market focus on innovation in materials engineering and manufacturing processes to strengthen their competitive position. Many manufacturers invest heavily in research and development to create lighter, stronger, and more aerodynamic wheel designs that improve vehicle efficiency and handling. Strategic collaborations with automotive manufacturers allow companies to supply wheels directly to original equipment production lines, strengthening long-term partnerships. Firms also expand their product portfolios through advanced forging technologies and customized design solutions to address the growing demand for premium vehicle personalization. Global expansion strategies, combined with strong distribution networks and aftermarket presence, help companies increase brand visibility and maintain market leadership while meeting evolving automotive performance requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Vehicle

- 2.2.4 Sales channel

- 2.2.5 Distribution channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for lightweight vehicles

- 3.2.1.2 Growth in premium & luxury vehicle sales

- 3.2.1.3 Expansion of motorsports industry

- 3.2.1.4 Aftermarket customization trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Volatility in raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing OEM partnerships

- 3.2.3.2 Growing EV aftermarket segment

- 3.2.3.3 Advancements in hybrid forging techniques

- 3.2.3.4 Emerging automotive markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Whole Vehicle Type Approval (WVTA)

- 3.4.2.2 ECE Regulation 124 (R124)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automotive Standards Organization (JASO)

- 3.4.3.2 AIS (Automotive Industry Standards) - India

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) - Resolution 242

- 3.4.4.2 Mexican NOM Standards (Normas Oficiales Mexicanas)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Cost breakdown analysis

- 3.10 Price analysis (Driven by Primary Research)

- 3.10.1 Historical Price Trend Analysis

- 3.10.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & Generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Quality standards & testing protocols

- 3.15.1 International quality certification standards (ISO, TUV, JWL)

- 3.15.2 Performance testing methodologies

- 3.15.3 Safety & durability requirements

- 3.15.4 Counterfeit product identification & prevention

- 3.16 Consumer behavior & buying patterns analysis

- 3.16.1 Purchase decision drivers

- 3.16.2 Brand loyalty & switching behavior

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Magnesium

- 5.4 Steel

- 5.5 Carbon fiber

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Entry-level performance vehicles

- 6.3 Mid-level luxury vehicles

- 6.4 Top-end luxury vehicles

- 6.5 Supercars & hypercars

- 6.6 Performance SUVs & crossovers

- 6.7 Motorsport & racing

Chapter 7 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Offline channel

- 8.3 Online channel

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 BBS Motorsport

- 10.1.2 Borbet

- 10.1.3 Carbon Revolution

- 10.1.4 Enkei

- 10.1.5 HRE Performance Wheels

- 10.1.6 OZ Racing

- 10.1.7 Rays Engineering / Volk Racing

- 10.1.8 Ronal

- 10.1.9 Vossen

- 10.1.10 Work Wheels

- 10.2 Regional players

- 10.2.1 Advan Racing / Yokohama

- 10.2.2 BC Forged

- 10.2.3 Dymag

- 10.2.4 Forgeline

- 10.2.5 Speedline Corse

- 10.2.6 SSR Wheels

- 10.2.7 TSW Alloy Wheels

- 10.2.8 Weds Sport

- 10.3 Emerging players

- 10.3.1 Cosmis Wheels

- 10.3.2 Fifteen52

- 10.3.3 Rotiform

- 10.3.4 Titan7

智慧輪胎軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測

智慧輪胎軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測 智慧輪胎技術市場預測至2034年—全球輪胎類型、感測器類型、驅動系統、分銷管道、技術、應用和區域分析

智慧輪胎技術市場預測至2034年—全球輪胎類型、感測器類型、驅動系統、分銷管道、技術、應用和區域分析 汽車高階輪胎市場:按類型、設計與結構、材料成分、銷售管道、應用與消費者細分分類-2026-2032年全球市場預測

汽車高階輪胎市場:按類型、設計與結構、材料成分、銷售管道、應用與消費者細分分類-2026-2032年全球市場預測 2026年全球高性能車輪市場報告汽車智慧輪胎市場:按車輛類型、輪胎類型、應用和銷售管道分類-2026-2032年全球市場預測

2026年全球高性能車輪市場報告汽車智慧輪胎市場:按車輛類型、輪胎類型、應用和銷售管道分類-2026-2032年全球市場預測 智慧輪胎市場規模、佔有率和成長分析:按產品類型、技術、感測器類型、車輛類型、連接方式、銷售管道和地區分類-2026-2033年產業預測

智慧輪胎市場規模、佔有率和成長分析:按產品類型、技術、感測器類型、車輛類型、連接方式、銷售管道和地區分類-2026-2033年產業預測 智慧輪胎市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、車輛類型、技術類型、銷售管道類型、地區和競爭格局分類,2021-2031年超高性能輪胎市場-全球產業規模、佔有率、趨勢、機會和預測:按輪胎類型、需求類別、車輛類型、地區和競爭格局分類,2021-2031年高性能乘用車輪胎市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031)汽車高階輪胎市場機會、成長要素、產業趨勢分析及2026年至2035年預測

智慧輪胎市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、車輛類型、技術類型、銷售管道類型、地區和競爭格局分類,2021-2031年超高性能輪胎市場-全球產業規模、佔有率、趨勢、機會和預測:按輪胎類型、需求類別、車輛類型、地區和競爭格局分類,2021-2031年高性能乘用車輪胎市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031)汽車高階輪胎市場機會、成長要素、產業趨勢分析及2026年至2035年預測