|

市場調查報告書

商品編碼

1998780

獸用支架市場機會、成長要素、產業趨勢分析及2026-2035年預測Veterinary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

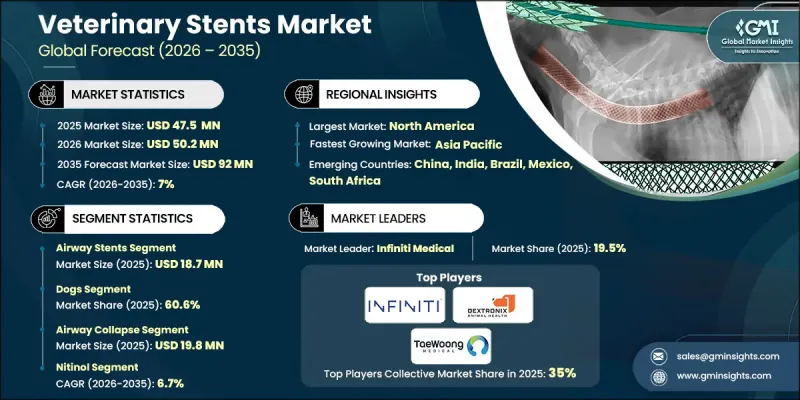

預計到 2025 年,全球獸用支架市場價值將達到 4,750 萬美元,並預計以 7% 的複合年成長率成長,到 2035 年達到 9,200 萬美元。

獸用支架市場的成長主要得益於人們對改善動物健康和提高獸醫治療標準的日益關注。隨著全球寵物數量的持續成長,獸醫和寵物飼主越來越重視能夠改善伴侶動物生活品質的有效醫療干預措施。獸用支架正日益被認可為治療動物重要內道結構性狹窄或阻塞的重要選擇。同時,技術的快速發展顯著提高了這些器械的性能和可靠性。除了微創獸醫手術的發展外,支架設計的改進和先進生物材料的引入也提高了植入手術的成功率。此外,影像和留置技術的進步使獸醫能夠提供更精準、更有效率的治療。這些進步有助於改善臨床療效,加速動物康復,並降低併發症率。因此,獸用支架正逐漸被獸醫專業人士廣泛接受,並贏得了尋求先進治療方法的寵物飼主的信任。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4750萬美元 |

| 預測金額 | 9200萬美元 |

| 複合年成長率 | 7% |

獸用支架是一種專門設計的植入,用於治療因疾病、創傷或發育異常而導致特定內道阻塞或狹窄的動物。這些圓柱形裝置通常由耐用的金屬合金或聚合物材料製成,並植入管狀解剖結構中,以維持正常的通道通暢並恢復正常的生理功能。獸用支架透過為受影響區域提供結構支撐,根據其植入位置的不同,有助於改善氣流、血液循環或體液流動。

預計到2025年,氣道支架市場規模將達到1,870萬美元。該市場的成長主要與伴侶動物氣道相關疾病發生率的上升有關,這些疾病需要長期在呼吸系統內提供結構支撐。此類疾病會導致嚴重的呼吸窘迫,需要即時進行醫療干預以恢復足夠的通氣量。獸醫和寵物飼主對微創治療方法的日益青睞也促進了氣道支架使用的增加。此外,支架材料工程的進步,包括自膨脹金屬合金和先進的生物可分解材料,正在提高器械性能並拓展其在獸醫臨床中的應用。

預計到2025年,犬類市場將佔據60.6%的市場。這一市場擴張歸因於犬類疾病盛行率的上升,而這些疾病需要支架輔助治療。影響呼吸系統、泌尿器官系統和血管系統的各種結構性併發症可能需要植入支架以恢復正常的生理功能。全球寵物犬數量的龐大以及獸醫支出的不斷成長進一步推動了該領域的成長。獸醫擴大將支架手術作為治療方法犬類重要內部通道結構性狹窄或阻塞的有效方法。

預計到2025年,北美獸用支架市佔率將達到41.5%。該地區的主導地位主要歸功於其高度發展的獸醫基礎設施以及寵物先進治療方案的廣泛普及。在北美,眾多專科動物醫院、轉診中心和先進的臨床設施均配備了進行包括支架植入在內的複雜微創手術的設備。此外,消費者在寵物醫療保健方面的強勁支出以及寵物保險計劃的普及,也有助於降低先進獸醫手術的費用負擔。這些因素共同推動了創新獸醫解決方案的普及,並支撐著全部區域獸用支架市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 寵物數量增加

- 呼吸道和泌尿器官系統疾病的盛行率

- 人們越來越關注寵物健康,但醫療成本也不斷上漲。

- 產業潛在風險與挑戰

- 獸醫支架和手術高成本

- 支架相關併發症的風險

- 市場機遇

- 擴大專業動物醫院及轉診中心

- 獸醫介入設備的技術進步

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 技術與創新趨勢(基於初步調查)

- 目前技術

- 新興技術

- 價格分析(基於初步調查)

- 人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 氣道支架

- 血管支架

- 尿道支架

- 其他支架

第6章 市場估計與預測:依動物種類分類,2022-2035年

- 狗

- 貓

- 其他動物

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 氣道阻塞

- 血管阻塞

- 泌尿道阻塞

- 其他用途

第8章 市場估算與預測:依材料分類,2022-2035年

- 鎳鈦諾

- 可生物分解聚合物

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 獸醫醫院和診所

- 其他最終用戶

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AbtVet(Stening group)

- Create Medic

- Dextronix

- EpiicVet

- Infiniti Medical

- MI Tech

- TaeWoong Medical

- UltraVet Medical Devices

The Global Veterinary Stents Market was valued at USD 47.5 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 92 million by 2035.

Growth in the veterinary stents market is strongly influenced by the increasing focus on improving animal health and advancing treatment standards within veterinary medicine. As pet ownership continues to rise globally, veterinarians and pet owners are placing greater emphasis on effective medical interventions that enhance the quality of life for companion animals. Veterinary stents are increasingly recognized as an important treatment option for animals experiencing structural narrowing or blockages in vital body passages. At the same time, rapid technological advancements have significantly improved the performance and reliability of these devices. The development of minimally invasive veterinary procedures, along with improved stent designs and advanced biomaterials, has enhanced the success rate of implantation procedures. In addition, improvements in imaging and placement technologies are enabling veterinarians to deliver more precise and efficient treatments. These advancements are contributing to better clinical outcomes, faster recovery for animals, and reduced complication rates. As a result, veterinary stents are gaining wider acceptance among veterinary professionals while also receiving greater trust from pet owners seeking advanced treatment options.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.5 Million |

| Forecast Value | $92 Million |

| CAGR | 7% |

Veterinary stents function as specialized implants designed to treat animals experiencing blockages or narrowing within certain internal pathways caused by disease, injury, or developmental abnormalities. These cylindrical devices are typically manufactured using durable metal alloys or polymer-based materials and are inserted into tubular anatomical structures to maintain proper passage and restore normal physiological function. By providing structural support within affected areas, veterinary stents help improve airflow, circulation, or fluid movement, depending on the location of placement.

The airway stents segment generated USD 18.7 million in 2025. Segment growth is primarily associated with the rising incidence of airway-related disorders among companion animals that require long-term structural support within the respiratory tract. Such conditions can lead to severe breathing complications and require immediate medical intervention to restore proper airflow. The growing preference among veterinarians and pet owners for minimally invasive treatment approaches has contributed to the increased use of airway stents. Additionally, advancements in stent material engineering, including self-expanding metal alloys and modern biodegradable materials, have improved device performance and expanded their clinical use within veterinary practices.

The dogs segment held 60.6% share in 2025. Market expansion within this segment is driven by the rising occurrence of medical conditions in canine populations that require stent-based treatment. Various structural complications affecting the respiratory, urinary, and vascular systems can require intervention through stent placement to restore normal physiological function. The high global population of companion dogs and increasing spending on veterinary healthcare further support the growth of this segment. Veterinarians are increasingly utilizing stent procedures as an effective treatment solution for dogs experiencing structural narrowing or obstructions within critical internal pathways.

North America Veterinary Stents Market accounted for 41.5% share in 2025. The region's leadership position is largely supported by its highly developed veterinary healthcare infrastructure and widespread availability of advanced treatment options for companion animals. Numerous specialized veterinary hospitals, referral centers, and advanced clinical facilities across North America are equipped to perform complex minimally invasive procedures, including stent implantation. In addition, strong consumer spending on pet healthcare and the availability of pet insurance programs contribute to greater affordability for advanced veterinary procedures. These factors collectively encourage the adoption of innovative veterinary treatment solutions and support the continued growth of the veterinary stents market across the region.

Key companies operating in the Global Veterinary Stents Market include Infiniti Medical, Dextronix, TaeWoong Medical, UltraVet Medical Devices, Create Medic, M.I. Tech, AbtVet (Stening Group), and EpiicVet. Companies competing in the Veterinary Stents Market are implementing several strategic initiatives to strengthen their market presence and expand global reach. Leading manufacturers are focusing heavily on research and development to introduce advanced stent designs with improved durability, flexibility, and biocompatibility. Many companies are also investing in the development of innovative materials and minimally invasive delivery systems to enhance treatment effectiveness and simplify clinical procedures for veterinarians. Strategic collaborations with veterinary hospitals, specialty clinics, and research institutions are helping companies improve product adoption and clinical validation. Additionally, market participants are expanding their distribution networks and strengthening regional partnerships to increase accessibility to veterinary stent technologies across emerging markets while maintaining strong competitiveness in established veterinary healthcare sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal trends

- 2.2.4 Application trends

- 2.2.5 Material trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership

- 3.2.1.2 Prevalence of respiratory and urological disorders

- 3.2.1.3 Growing awareness of pet health and healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary stents and procedures

- 3.2.2.2 Risk of stent-related complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of veterinary specialty hospitals and referral centers

- 3.2.3.2 Technological advancements in veterinary interventional devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Impact of AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Airway stents

- 5.3 Vascular stents

- 5.4 Urethral stents

- 5.5 Other stents

Chapter 6 Market Estimates and Forecast, By Animal, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Other animals

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Airway collapse

- 7.3 Vascular obstructions

- 7.4 Urinary tract obstructions

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Nitinol

- 8.3 Biodegradable polymer

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbtVet (Stening group)

- 11.2 Create Medic

- 11.3 Dextronix

- 11.4 EpiicVet

- 11.5 Infiniti Medical

- 11.6 M.I. Tech

- 11.7 TaeWoong Medical

- 11.8 UltraVet Medical Devices

全球自膨式覆膜支架市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球自膨式覆膜支架市場規模、佔有率、趨勢和成長分析報告(2026-2034) 血管支架市場:全球市場按產品類型、材質、輸送系統、應用和最終用戶分類的預測——2026-2032年支架市場:2026-2032年全球市場預測(依產品類型、材料、輸送方式、應用及最終用戶分類)

血管支架市場:全球市場按產品類型、材質、輸送系統、應用和最終用戶分類的預測——2026-2032年支架市場:2026-2032年全球市場預測(依產品類型、材料、輸送方式、應用及最終用戶分類) 自膨式覆膜支架市場規模、佔有率和趨勢分析報告:按解剖部位、適應症、材料和細分市場分類(2026-2033 年)覆膜支架市場規模、佔有率和趨勢分析報告:按器材類型、解剖部位、地區和細分市場預測(2026-2033 年)

自膨式覆膜支架市場規模、佔有率和趨勢分析報告:按解剖部位、適應症、材料和細分市場分類(2026-2033 年)覆膜支架市場規模、佔有率和趨勢分析報告:按器材類型、解剖部位、地區和細分市場預測(2026-2033 年) 血管支架市場報告:按產品類型、材料、輸送方式、最終用戶和地區分類(2026-2034 年)

血管支架市場報告:按產品類型、材料、輸送方式、最終用戶和地區分類(2026-2034 年) 胃腸道支架市場報告:趨勢、預測和競爭分析(至2035年)裸金屬支架市場:按類型、材質、長度、應用和最終用戶分類-2026-2032年全球市場預測頸動脈支架市場:依產品類型、材料、輸送方式、最終用戶和通路分類-2026-2032年全球市場預測

胃腸道支架市場報告:趨勢、預測和競爭分析(至2035年)裸金屬支架市場:按類型、材質、長度、應用和最終用戶分類-2026-2032年全球市場預測頸動脈支架市場:依產品類型、材料、輸送方式、最終用戶和通路分類-2026-2032年全球市場預測 支架市場機會、成長要素、產業趨勢分析及2026-2035年預測。

支架市場機會、成長要素、產業趨勢分析及2026-2035年預測。